Outcome

Data over the last month has generally surprised to the upside, with both inflation and the GDP reporting stronger than expected outcomes. The labour market indicators remain buoyant, and the WPI highlighted that private sector wage momentum is now picking up amid labour shortages in some sectors and generally strong demand across the board. With public sector wage freezes also being unwound along with the usual increases in award/award-linked wages, a further acceleration in wages growth is likely to materialise moving through 2022. This in turn will feed through to core inflation (although the acceleration is likely to be modest, given the lags between strengthening labour demand, wages and final output prices). At the same time, headline inflation is likely to moderate, as momentum in global fuel prices (and other commodities/materials) ease and the supply/logistics chain disruptions abate.

Building on the stronger print for GDP, the high frequency data suggests that household spending in the lockdown states has rebounded rapidly. Business investment expectations remain robust, which suggest that domestic private sector demand should be able to drive growth momentum into 2022, even as the contribution to growth from the public sector wanes. It is also worth noting that while public spending will contribute less to momentum in 2022, it will remain at historically high levels due to the ongoing infrastructure investment programs, continued rollout of the vaccine program and other COVID-related expenditure, and the increase in spending on aged car, child care, mental health services and other initiatives announced in the FY22 budget.

The re-opening of the border to international students and migrant workers will boost both demand and supply in the economy. Within the labour market the re-entry of these workers will relieve some of the most acute labour shortages, particularly in the hospitality, agriculture/food processing and IT sectors. But the return of migrants is likely to be patchy, given the strength of demand for labour globally and the need to re-establish dormant networks within the community. As such, this channel is not likely to materially weigh on the positive momentum in wages.

A key pillar of the economic recovery has been the successful rollout of the vaccine across Australia. But the emergence of the Omicron variant has highlighted that the pandemic is far from over (indeed, it will remain a significant risk until a high proportion of the global population has been vaccinated). The variant poses a significant downside risk to the outlook, particularly to the travel/tourism sectors. We do not yet know the transmissibility or severity of the disease, or whether the current vaccines will remain highly efficacious. In a worst case scenario the authorities could be forced to reintroduce significant social distancing restrictions to control the spread while modified vaccines are developed and administered. In this case it would be appropriate for monetary settings to remain accommodating for longer than currently expected, to support the economy.

As predicted, real GDP growth was negative in 2021Q3, although the decline in activity was not as bad as might have been expected given the lockdowns and ongoing lack of international travel. We can expect a robust recovery going forward, although there is heightened uncertainty given the Omicron variant.

We can also expect inflation to remain elevated in the short term, but possibly fall back below the target range as (i) the base effects from Covid wear off, (ii) the effects of falling oil prices work their way through to final goods prices, and (iii) supply chains return more to their normal operations. As a more positive signal for returning inflation sustainably to target range is a heightened sense of labour-market shortages that will inevitably lead to more wage growth at some point of time.

The RBA abandoned the yield curve control target just before the previous Board meeting, but they are still communicating forward guidance that they expect to keep the policy rate at the effective lower bound until late 2023 at the earliest. I believe this is the right policy for the RBA given the need for expansionary policy to bring inflation sustainably into the target range. Indeed, it is possible that they will need to extend zero-interest-rate policy beyond 2023, as reflected in my distributions for the policy rate 3 years from now.

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Omicron Could Threaten Australia’s Strong Economic Bounce: Cash Rate To Stay Low

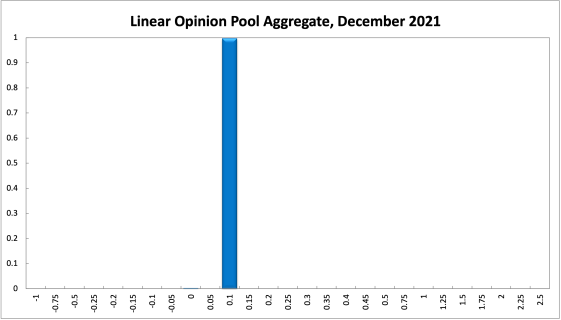

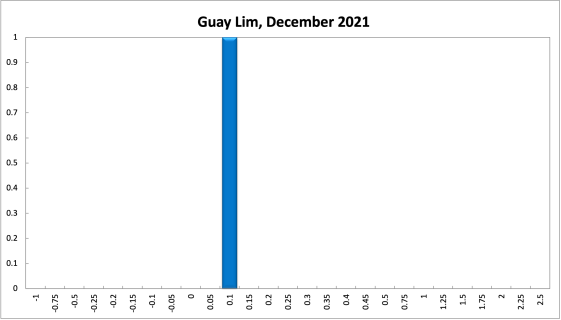

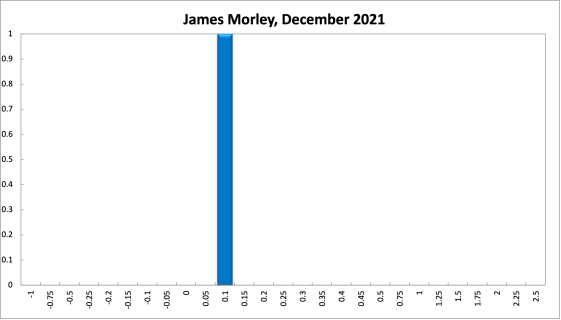

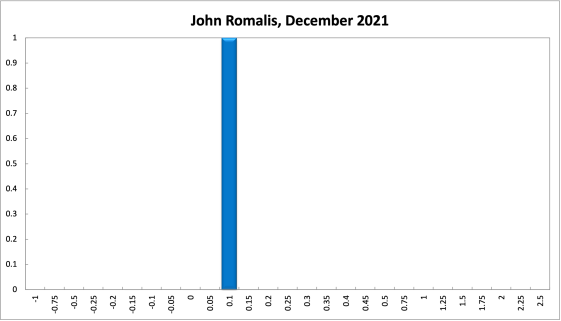

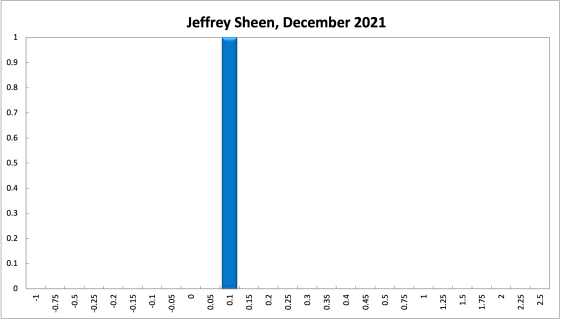

Australian GDP contracted by 1.9% in the third quarter, less than predicted by markets. Fourth quarter GDP growth, given Australia’s high vaccination rate and easing of restrictions, should be strongly positive, unless the Omicron variant ends up posing a serious threat to the population. No new inflation data has been released; the most recent measurement of the growth rate of the CPI equals 3% (year-on-year) in the third quarter of 2021, right at the top of the RBA’s official target band of 2-3%. The preferred inflation statistic, the trimmed mean measure of core inflation, equals 2.1%, at the bottom of the target range. The RBA Shadow Board’s verdict is, once again, unchanged from the previous month: it is certain (100% confident) that keeping the cash rate at the historically low rate of 0.1% is the appropriate policy for the November round.

As widely predicted, the most recent official ABS unemployment rate increased, from 4.6% in September to 5.2% in October, whilst the youth unemployment rate spiked by more than two percentage points, to 13.1%. Total employment fell by nearly 50,000 and the participation rate increased slightly to 64.7%. The underemployment rate also increased slightly to 9.5%; monthly hours worked fell by approximately 1 million hours, that is, by 0.1%. On the upside, job advertisements increased by more than 10,000. Moreover, there are growing signs that labour shortages in some sectors are fuelling wage demands.

The Aussie dollar, following a rally in October, dropped steadily in the past weeks to below 71 US¢. Yields on Australian 10-year government bonds retreated, from approx. 2% to 1.65%. The yield curves, all of which are showing ‘normal’ convexity, have consequently flattened slightly, as seen in the compressed interest rate spreads: for short-term maturities (2-year versus 1-year) the spread is now a mere 13.8 points, closer to the RBA’s stated intention of keeping the 3-year rate on par with the 1-year rate; in mid-term versus short-term maturities (5-year versus 2-year) the spread is 96.3 bps and in higher-term maturities (10-year versus 2-year) the spread narrowed substantially, to 125.1 bps. Spurred by concerns about the Omicron variant, Australian share prices continued their retreat from their August all-time high: the S&P/ASX 200 stock index is now trading barely above 7,200.

The outlook for the global economy has not changed much, except for the emergence of the omicron variant of the corona virus. Just how much of an epidemiological, and thus also economic threat, this new variant poses will become clearer in the coming weeks, in particular, whether or not existing vaccinations are effective. Clogged supply chains and goods price inflation remain a genuine concern, at least in the short-term, as do geopolitical tensions, notably the military build-up near the Ukrainian border. The US economy, based on recent data, appears to be gaining momentum, while there are mixed economic signals coming out of China.

Australian consumer confidence remained steady for the third consecutive month, with the Melbourne Institute and Westpac Bank Consumer Sentiment Index printing at 105. Retail sales, already growing in October, surged in November, growing by 4.9% month-on-month, as NSW, VIC and the ACT eased their Covid-19 restrictions further. NAB’s index of business confidence continued its climb, the most recent reading up 10 points, from September. The services PMI and manufacturing PMI both improved somewhat, from 50.4 to 54.8 and from 45.7 to 47.6, respectively. The recent pickup in economic activity is reflected in a jump of the capacity utilization rate of more than 3 percentage points, to 81.47. The Westpac-Melbourne Institute Leading Economic Index improved by 0.16% month-on-month, ending a five-month decline, whereas the six-month annualised growth rate in the Leading Index was unchanged at 0.5%. Unless Omicron throws a large amount of sand in the wheels of the Australian economy, we should see confidence indicators improve and consequently economic activity pick up further.

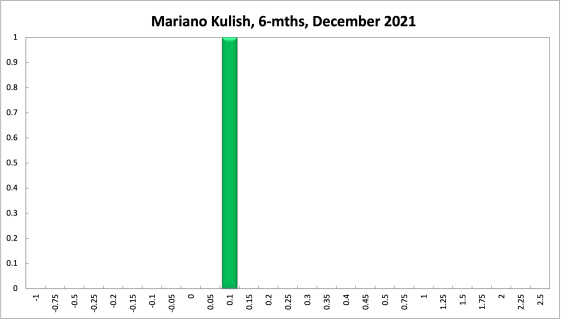

The official cash rate target has been at the historic level of 0.1% for 13 months. For yet another month, the Shadow Board maintains its unqualified conviction to keep the overnight interest rate at 0.1%: it is has no doubt that the overnight interest rate should remain steady, attaching 0% probability that either an increase is appropriate or a further rate cut to below 0.1%.

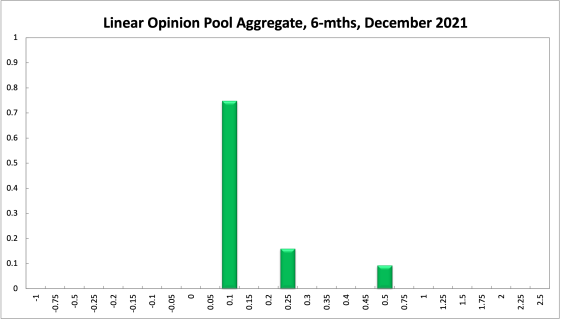

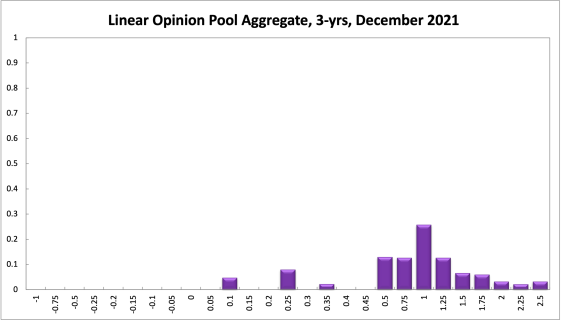

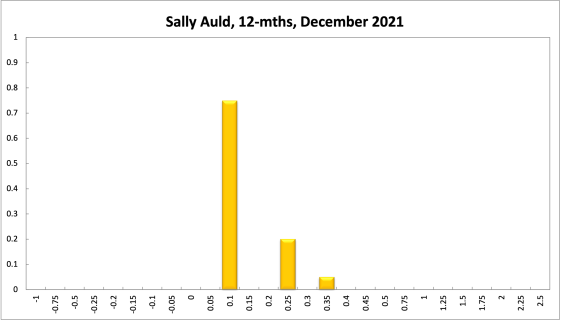

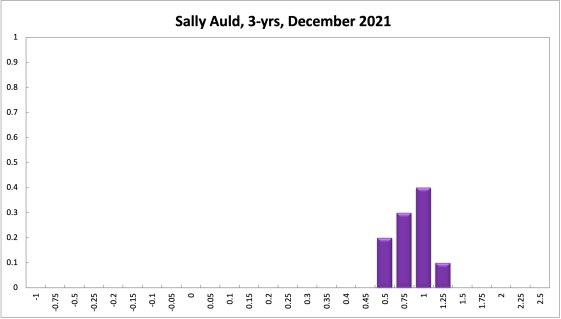

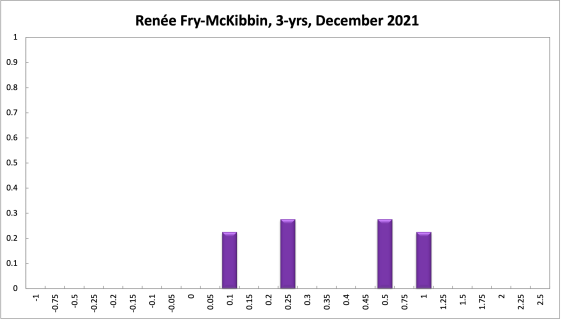

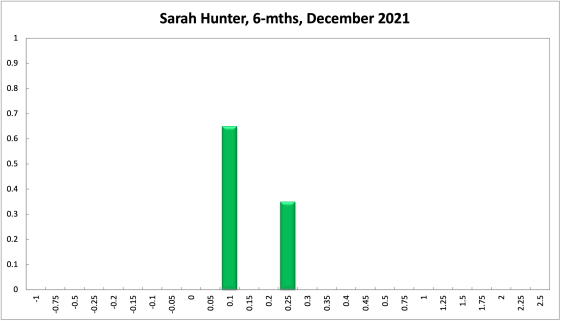

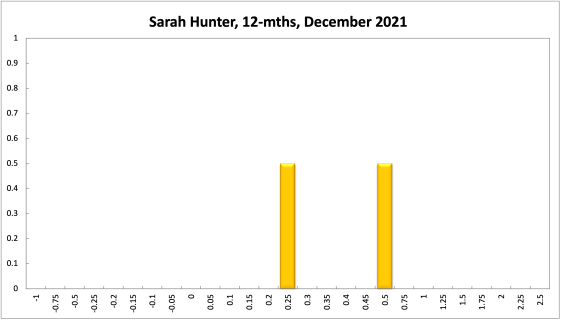

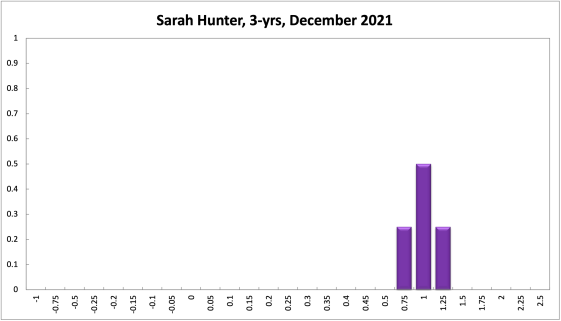

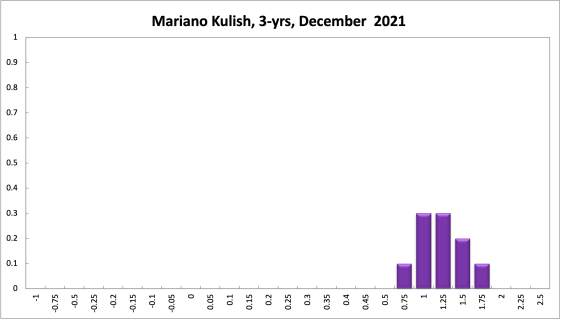

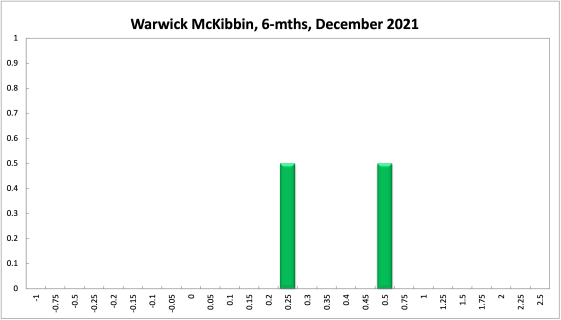

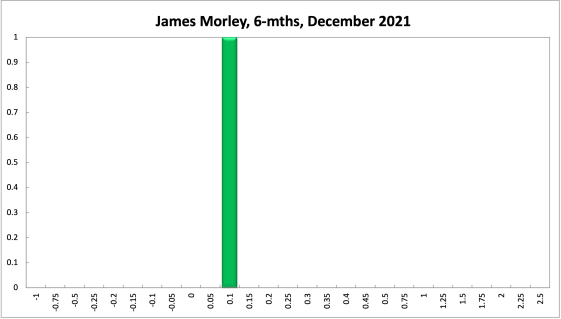

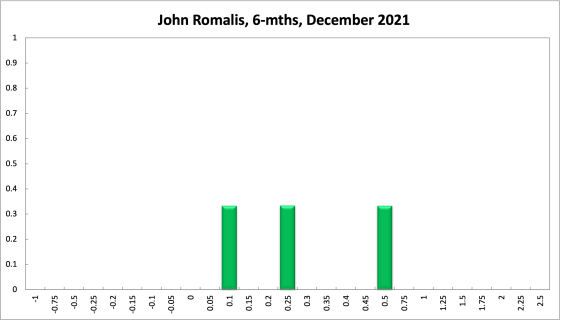

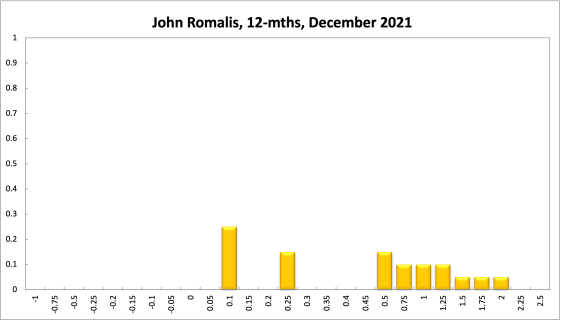

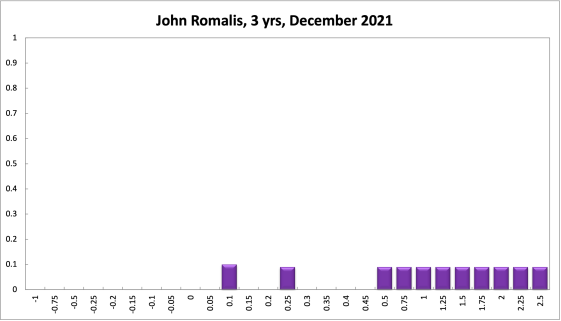

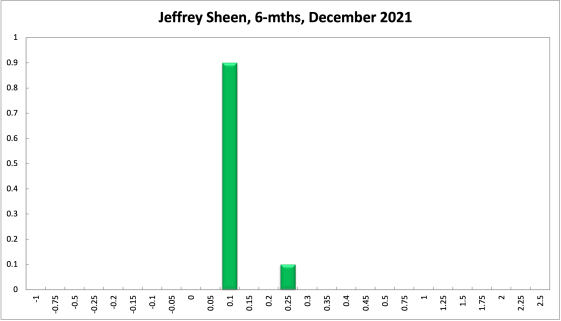

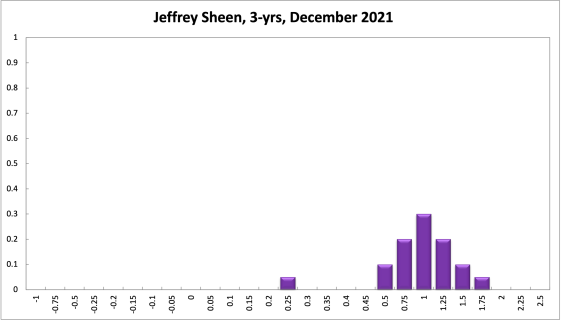

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at 0.1% has softened, from 83% in November to 75% in the current round; the probability attached to the appropriateness of an interest rate decrease remains unchanged at 0%, while the probability attached to a required increase rose to 25%. One year out, the Shadow Board members’ confidence that the cash rate should be held steady also fell, from 61% in November to 50% in this round. The confidence in a required cash rate decrease, to below 0.1%, is 0% (unchanged) and in a required cash rate increase 50% (39% in November). Three years out, the probabilities shifted in the same direction: the Shadow Board attaches a 5% probability that the overnight rate should equal 0.1% (down two percentage points), a 0% probability that a rate lower than 0.1% is appropriate, and a 95% probability that a rate higher than 0.1% is optimal (up two percentage points). The range of the probability distribution remained unchanged over the 6-month horizon, where it extends from 0.1% to 0.5%, but widened over the 12-month horizon, where it extends from 0.1% to 2%. For the 3-year recommendation, the distribution again remains unchanged, extending from 0.1% to 2.5%.