James Morley

As predicted, real GDP growth was negative in 2021Q3, although the decline in activity was not as bad as might have been expected given the lockdowns and ongoing lack of international travel. We can expect a robust recovery going forward, although there is heightened uncertainty given the Omicron variant.

We can also expect inflation to remain elevated in the short term, but possibly fall back below the target range as (i) the base effects from Covid wear off, (ii) the effects of falling oil prices work their way through to final goods prices, and (iii) supply chains return more to their normal operations. As a more positive signal for returning inflation sustainably to target range is a heightened sense of labour-market shortages that will inevitably lead to more wage growth at some point of time.

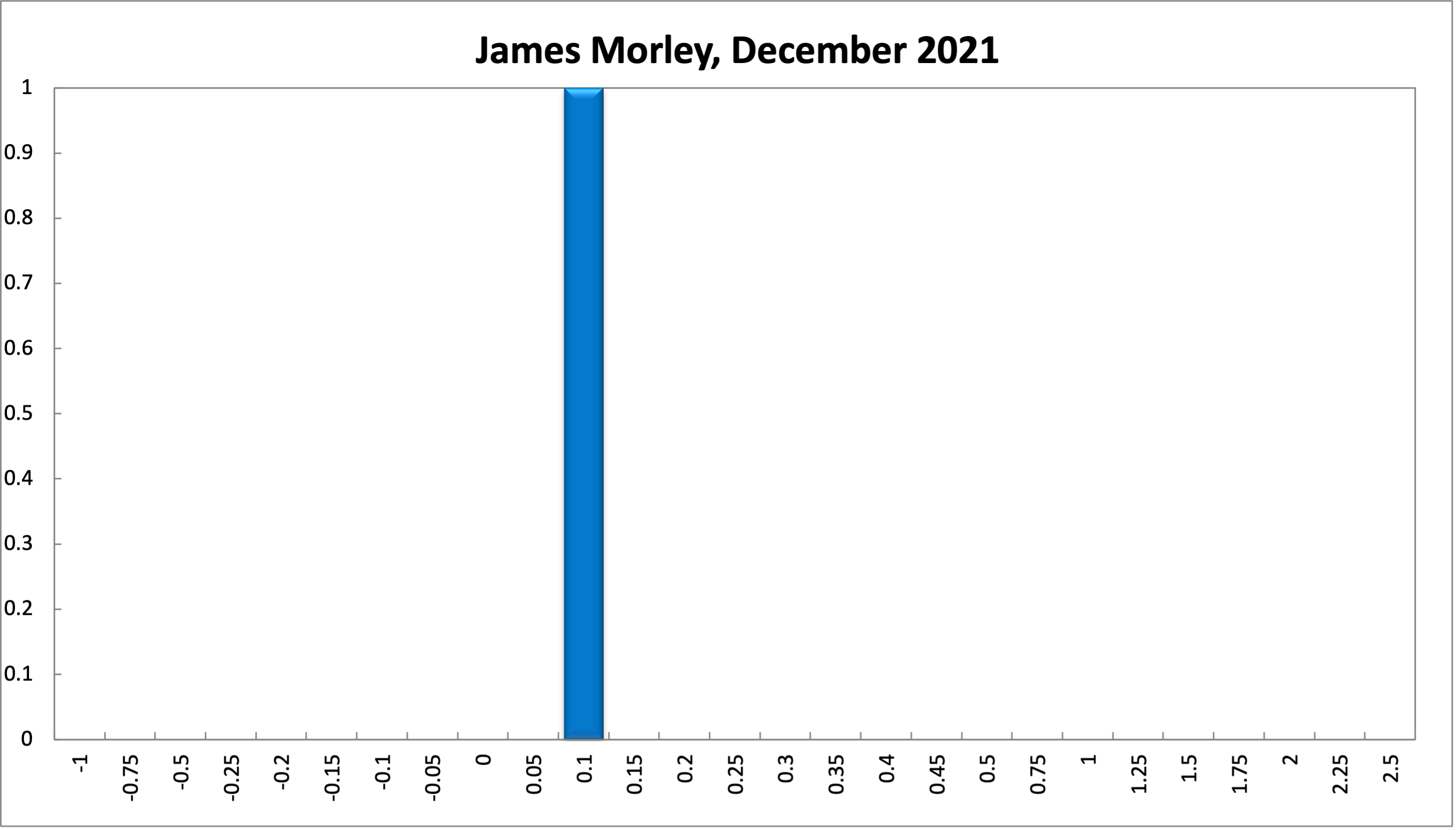

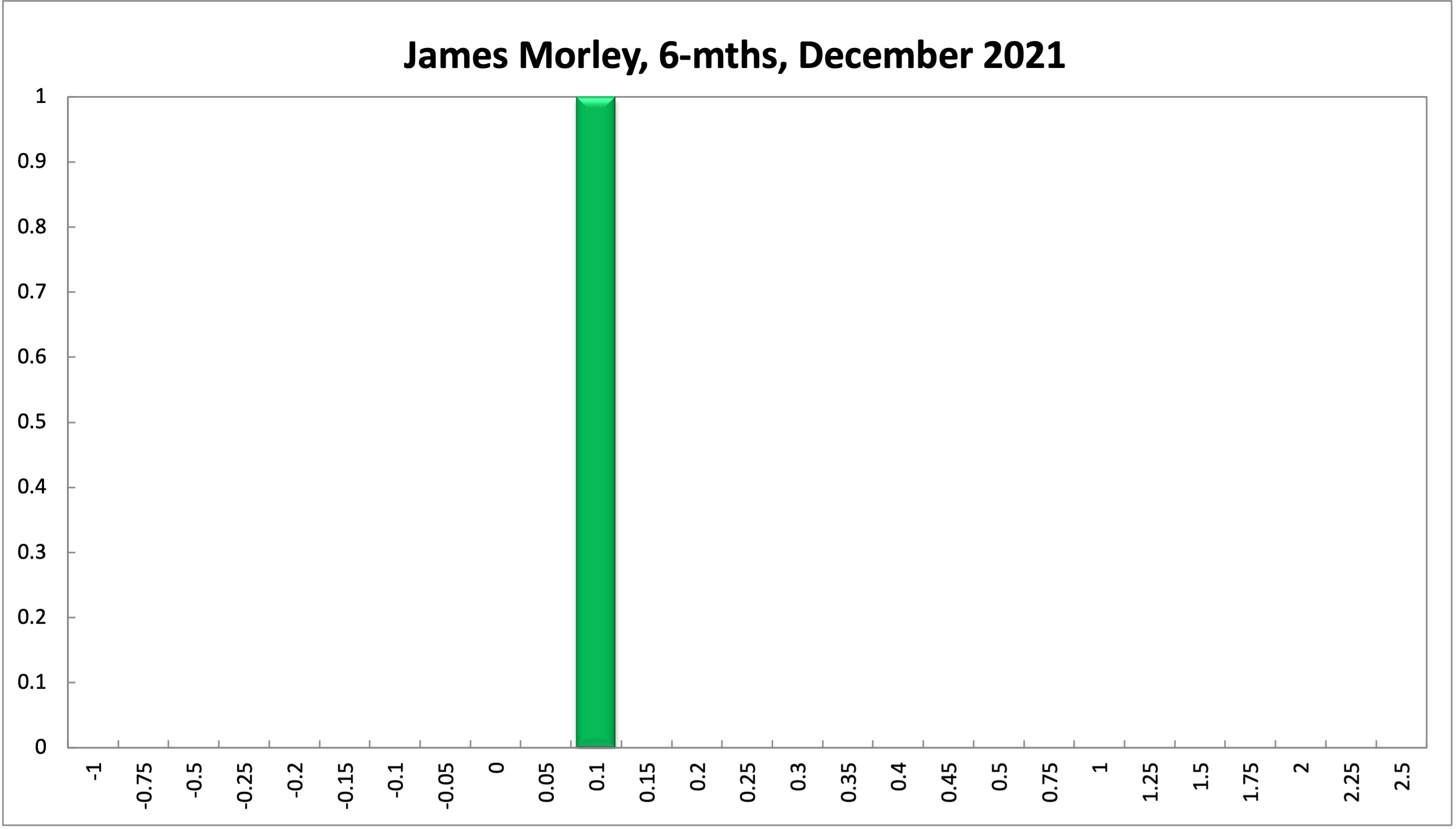

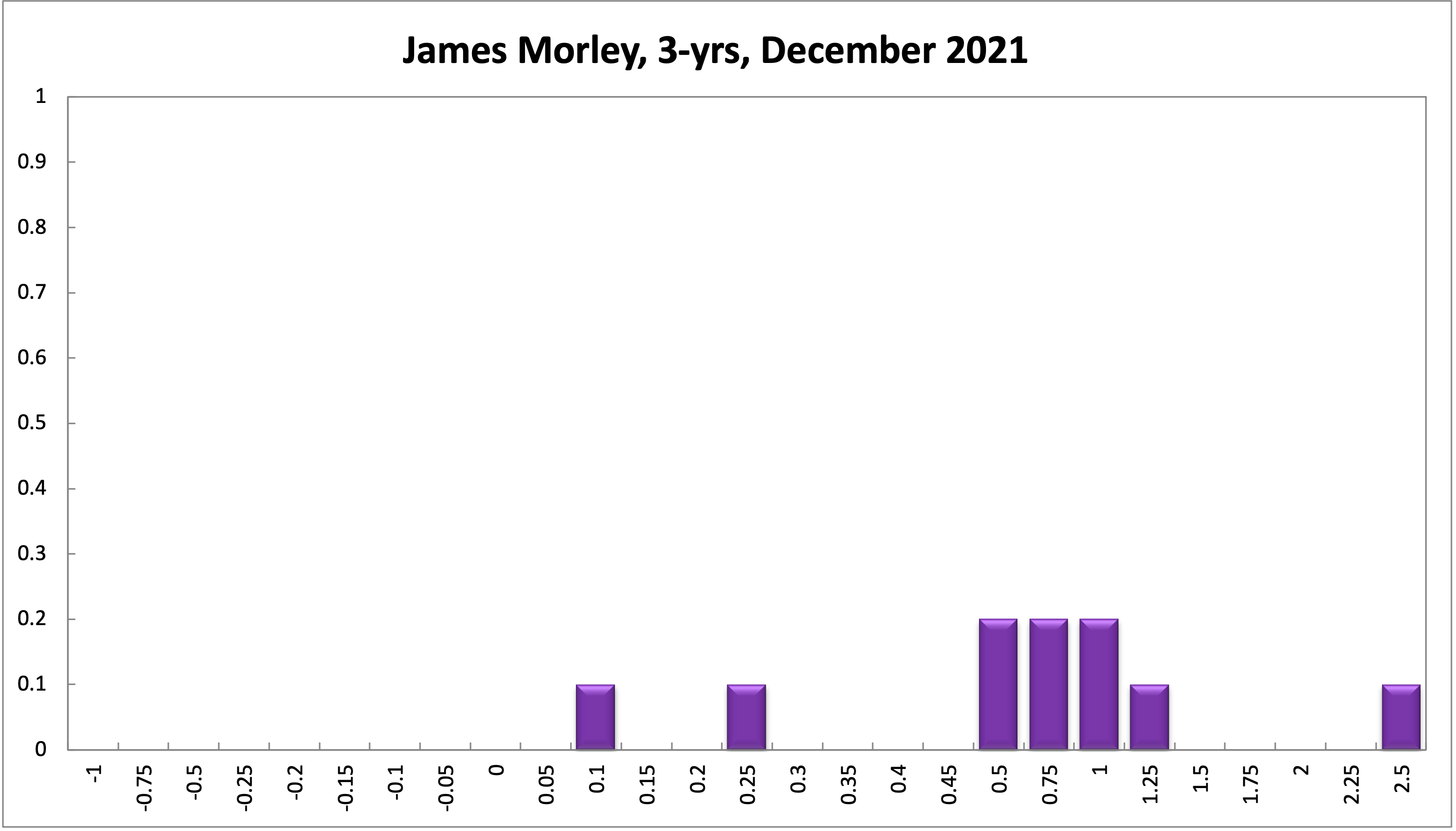

The RBA abandoned the yield curve control target just before the previous Board meeting, but they are still communicating forward guidance that they expect to keep the policy rate at the effective lower bound until late 2023 at the earliest. I believe this is the right policy for the RBA given the need for expansionary policy to bring inflation sustainably into the target range. Indeed, it is possible that they will need to extend zero-interest-rate policy beyond 2023, as reflected in my distributions for the policy rate 3 years from now.

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin