Aggregate

Omicron Could Threaten Australia’s Strong Economic Bounce: Cash Rate To Stay Low

Australian GDP contracted by 1.9% in the third quarter, less than predicted by markets. Fourth quarter GDP growth, given Australia’s high vaccination rate and easing of restrictions, should be strongly positive, unless the Omicron variant ends up posing a serious threat to the population. No new inflation data has been released; the most recent measurement of the growth rate of the CPI equals 3% (year-on-year) in the third quarter of 2021, right at the top of the RBA’s official target band of 2-3%. The preferred inflation statistic, the trimmed mean measure of core inflation, equals 2.1%, at the bottom of the target range. The RBA Shadow Board’s verdict is, once again, unchanged from the previous month: it is certain (100% confident) that keeping the cash rate at the historically low rate of 0.1% is the appropriate policy for the November round.

As widely predicted, the most recent official ABS unemployment rate increased, from 4.6% in September to 5.2% in October, whilst the youth unemployment rate spiked by more than two percentage points, to 13.1%. Total employment fell by nearly 50,000 and the participation rate increased slightly to 64.7%. The underemployment rate also increased slightly to 9.5%; monthly hours worked fell by approximately 1 million hours, that is, by 0.1%. On the upside, job advertisements increased by more than 10,000. Moreover, there are growing signs that labour shortages in some sectors are fuelling wage demands.

The Aussie dollar, following a rally in October, dropped steadily in the past weeks to below 71 US¢. Yields on Australian 10-year government bonds retreated, from approx. 2% to 1.65%. The yield curves, all of which are showing ‘normal’ convexity, have consequently flattened slightly, as seen in the compressed interest rate spreads: for short-term maturities (2-year versus 1-year) the spread is now a mere 13.8 points, closer to the RBA’s stated intention of keeping the 3-year rate on par with the 1-year rate; in mid-term versus short-term maturities (5-year versus 2-year) the spread is 96.3 bps and in higher-term maturities (10-year versus 2-year) the spread narrowed substantially, to 125.1 bps. Spurred by concerns about the Omicron variant, Australian share prices continued their retreat from their August all-time high: the S&P/ASX 200 stock index is now trading barely above 7,200.

The outlook for the global economy has not changed much, except for the emergence of the omicron variant of the corona virus. Just how much of an epidemiological, and thus also economic threat, this new variant poses will become clearer in the coming weeks, in particular, whether or not existing vaccinations are effective. Clogged supply chains and goods price inflation remain a genuine concern, at least in the short-term, as do geopolitical tensions, notably the military build-up near the Ukrainian border. The US economy, based on recent data, appears to be gaining momentum, while there are mixed economic signals coming out of China.

Australian consumer confidence remained steady for the third consecutive month, with the Melbourne Institute and Westpac Bank Consumer Sentiment Index printing at 105. Retail sales, already growing in October, surged in November, growing by 4.9% month-on-month, as NSW, VIC and the ACT eased their Covid-19 restrictions further. NAB’s index of business confidence continued its climb, the most recent reading up 10 points, from September. The services PMI and manufacturing PMI both improved somewhat, from 50.4 to 54.8 and from 45.7 to 47.6, respectively. The recent pickup in economic activity is reflected in a jump of the capacity utilization rate of more than 3 percentage points, to 81.47. The Westpac-Melbourne Institute Leading Economic Index improved by 0.16% month-on-month, ending a five-month decline, whereas the six-month annualised growth rate in the Leading Index was unchanged at 0.5%. Unless Omicron throws a large amount of sand in the wheels of the Australian economy, we should see confidence indicators improve and consequently economic activity pick up further.

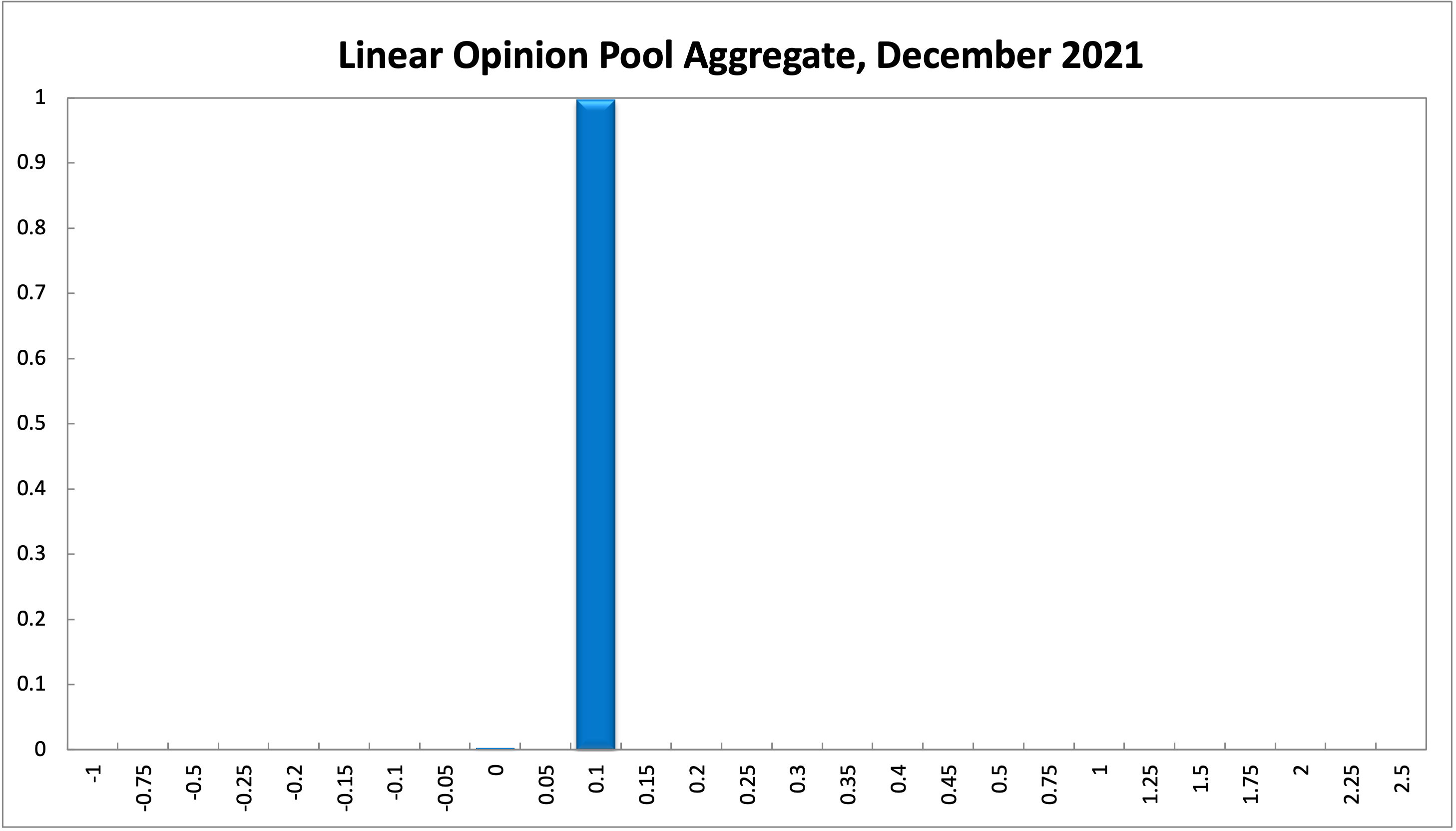

The official cash rate target has been at the historic level of 0.1% for 13 months. For yet another month, the Shadow Board maintains its unqualified conviction to keep the overnight interest rate at 0.1%: it is has no doubt that the overnight interest rate should remain steady, attaching 0% probability that either an increase is appropriate or a further rate cut to below 0.1%.

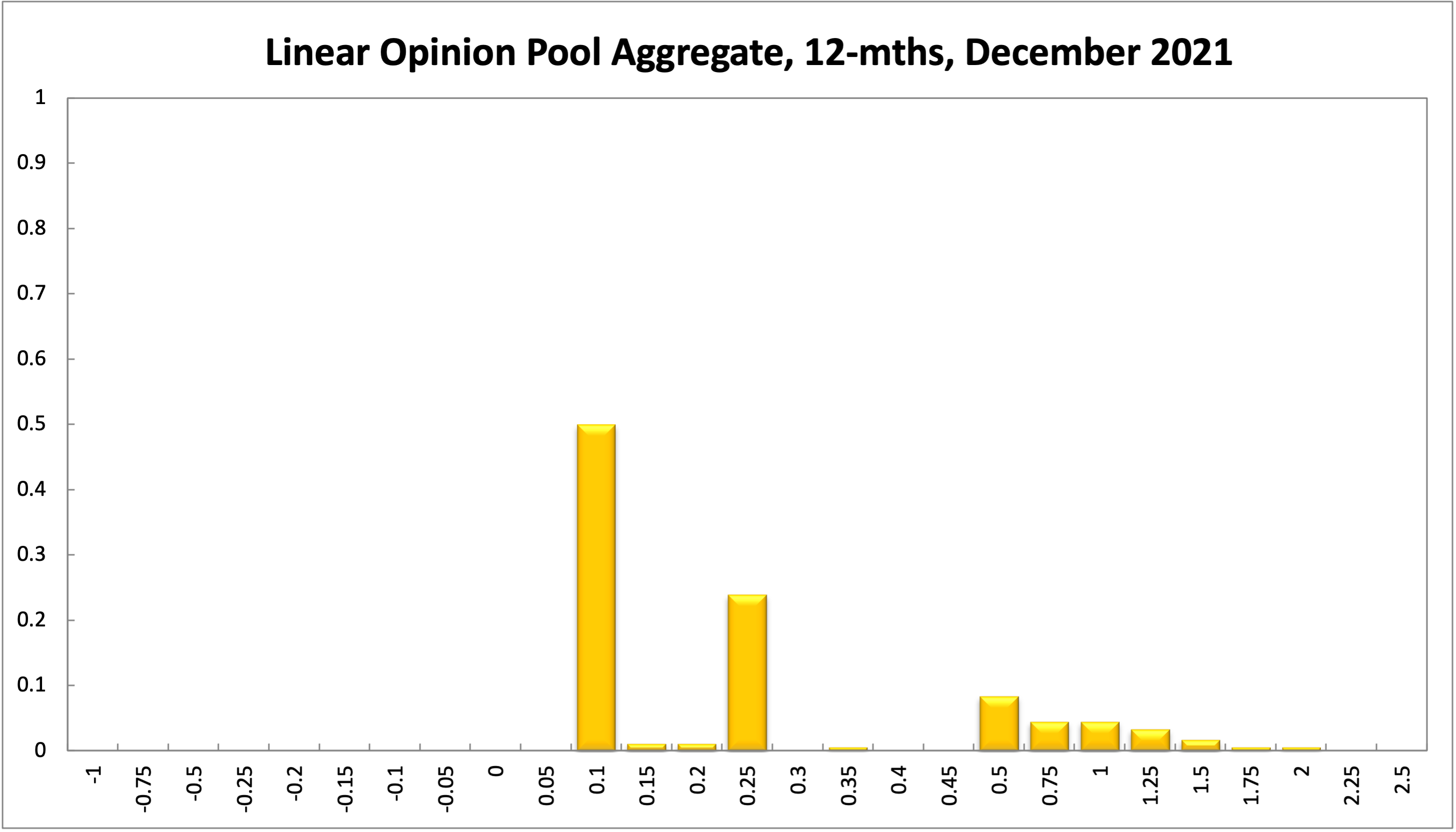

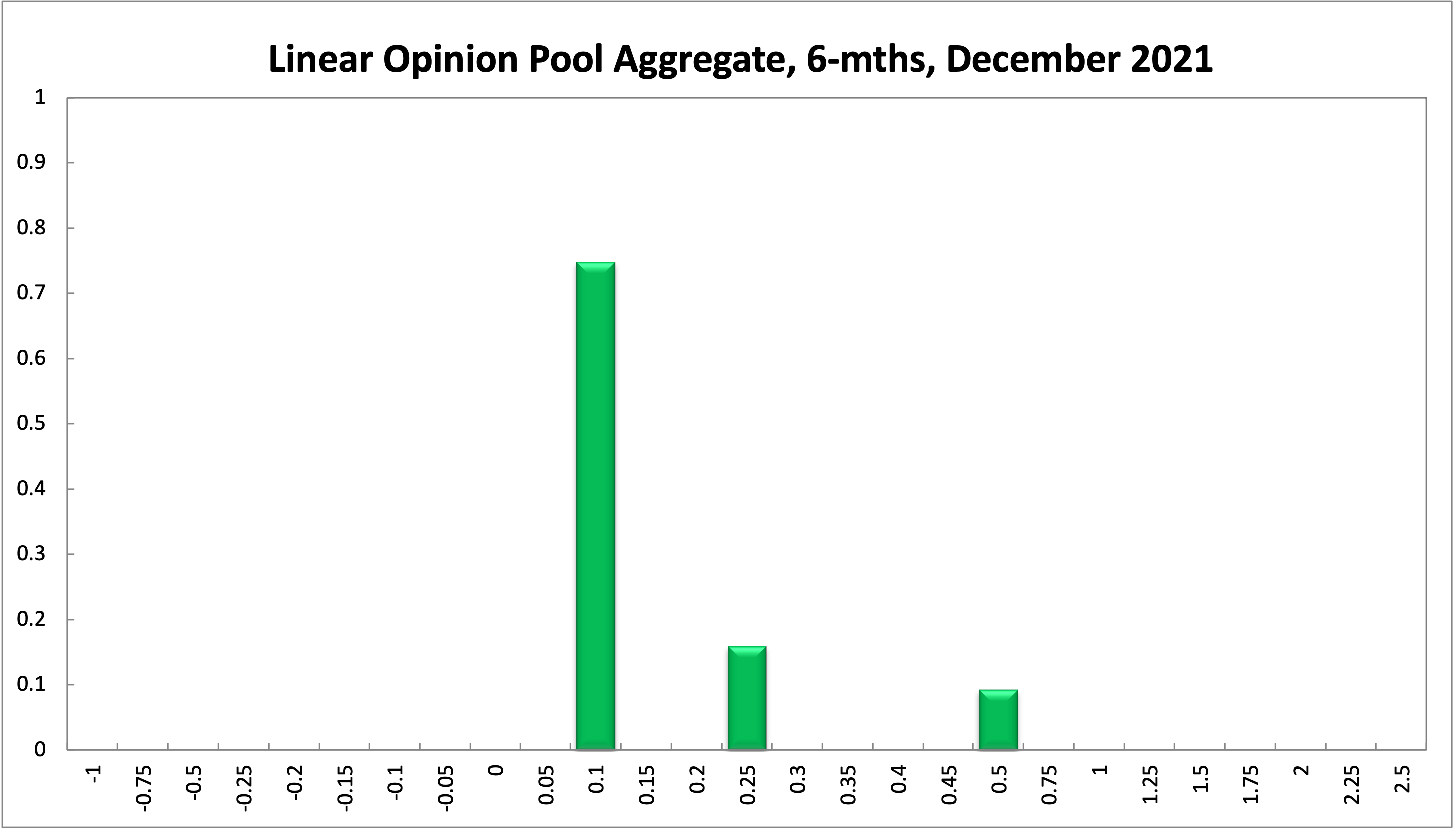

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at 0.1% has softened, from 83% in November to 75% in the current round; the probability attached to the appropriateness of an interest rate decrease remains unchanged at 0%, while the probability attached to a required increase rose to 25%. One year out, the Shadow Board members’ confidence that the cash rate should be held steady also fell, from 61% in November to 50% in this round. The confidence in a required cash rate decrease, to below 0.1%, is 0% (unchanged) and in a required cash rate increase 50% (39% in November). Three years out, the probabilities shifted in the same direction: the Shadow Board attaches a 5% probability that the overnight rate should equal 0.1% (down two percentage points), a 0% probability that a rate lower than 0.1% is appropriate, and a 95% probability that a rate higher than 0.1% is optimal (up two percentage points). The range of the probability distribution remained unchanged over the 6-month horizon, where it extends from 0.1% to 0.5%, but widened over the 12-month horizon, where it extends from 0.1% to 2%. For the 3-year recommendation, the distribution again remains unchanged, extending from 0.1% to 2.5%.

Updated: 27 December 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin