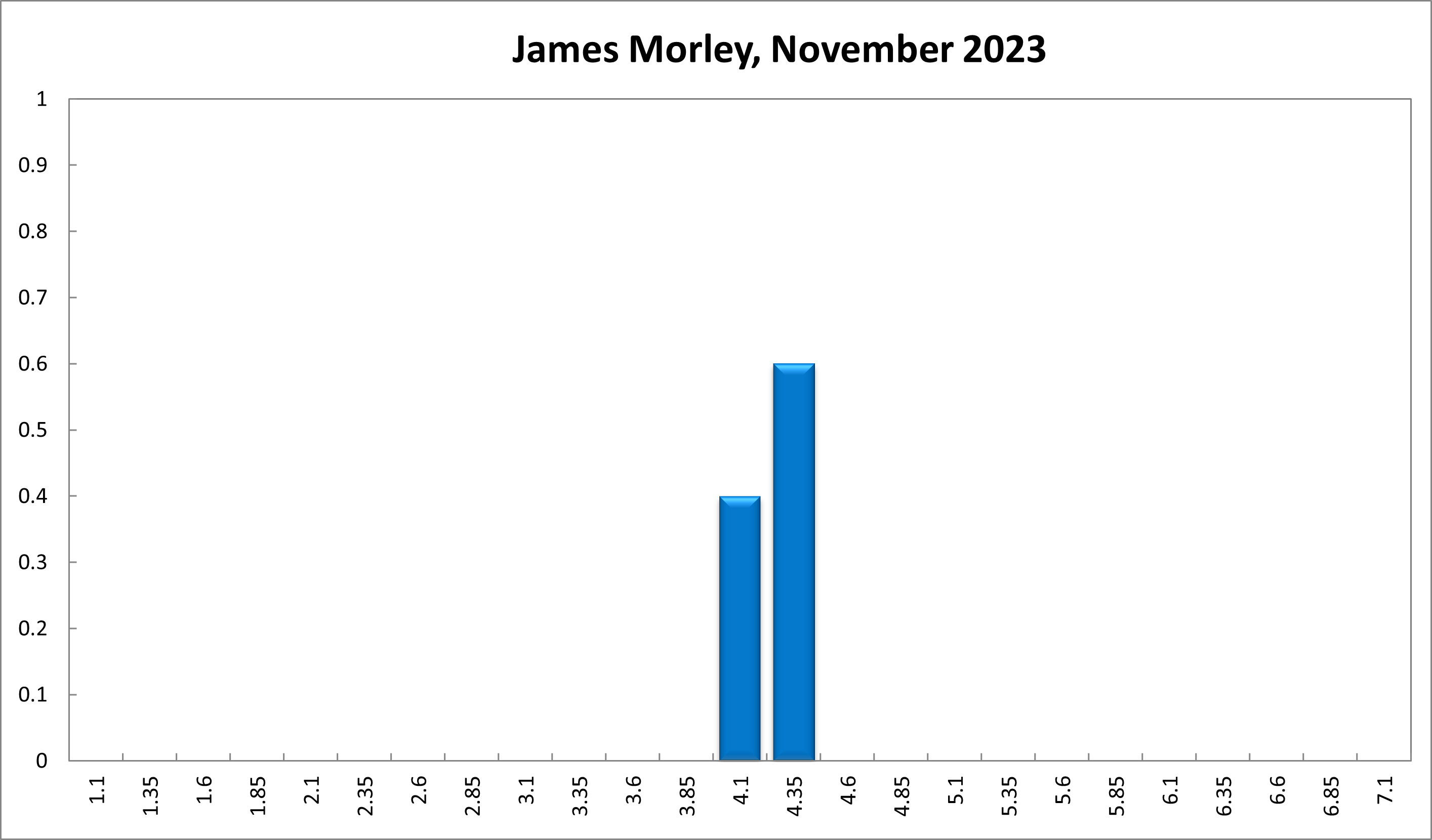

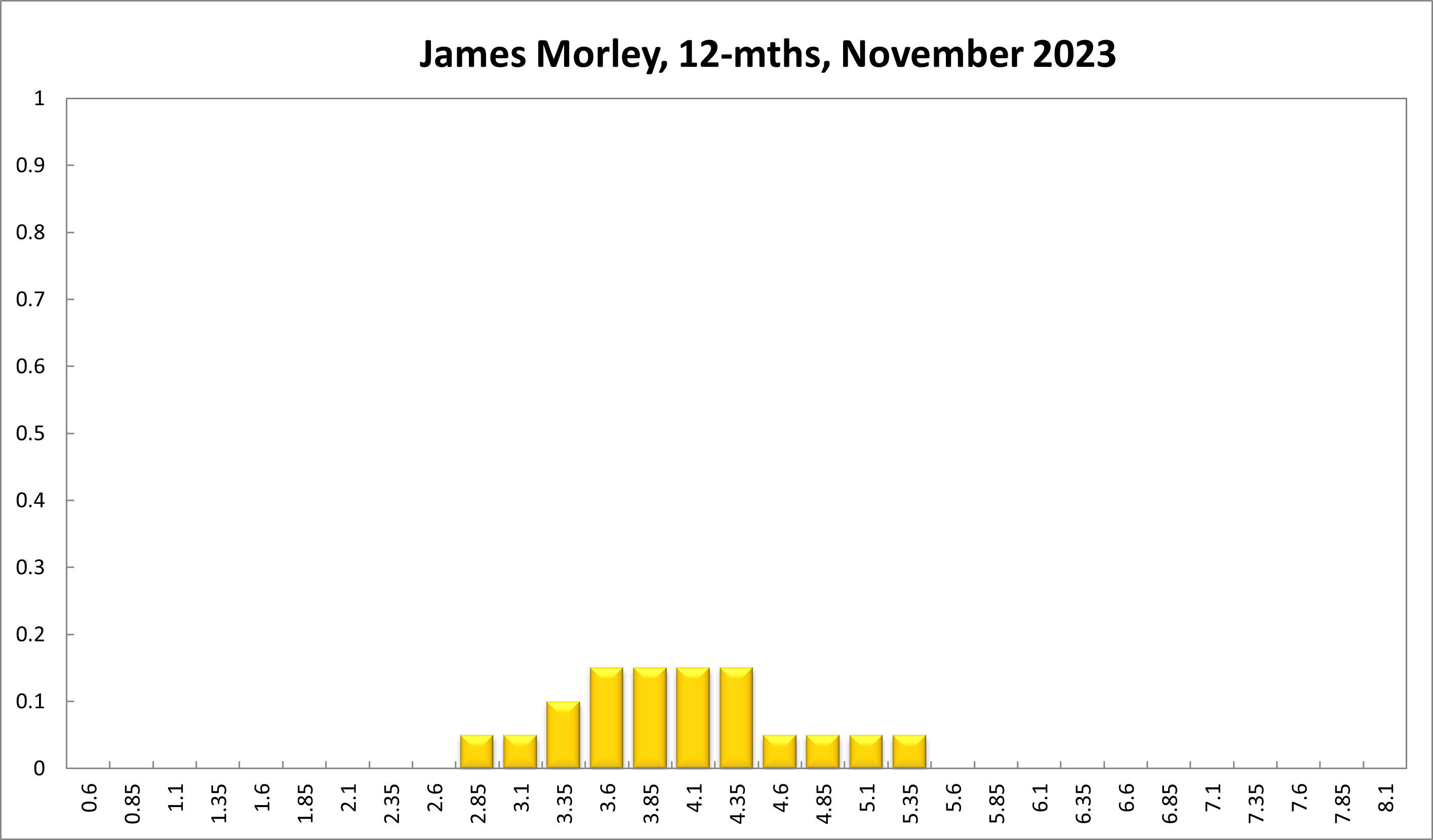

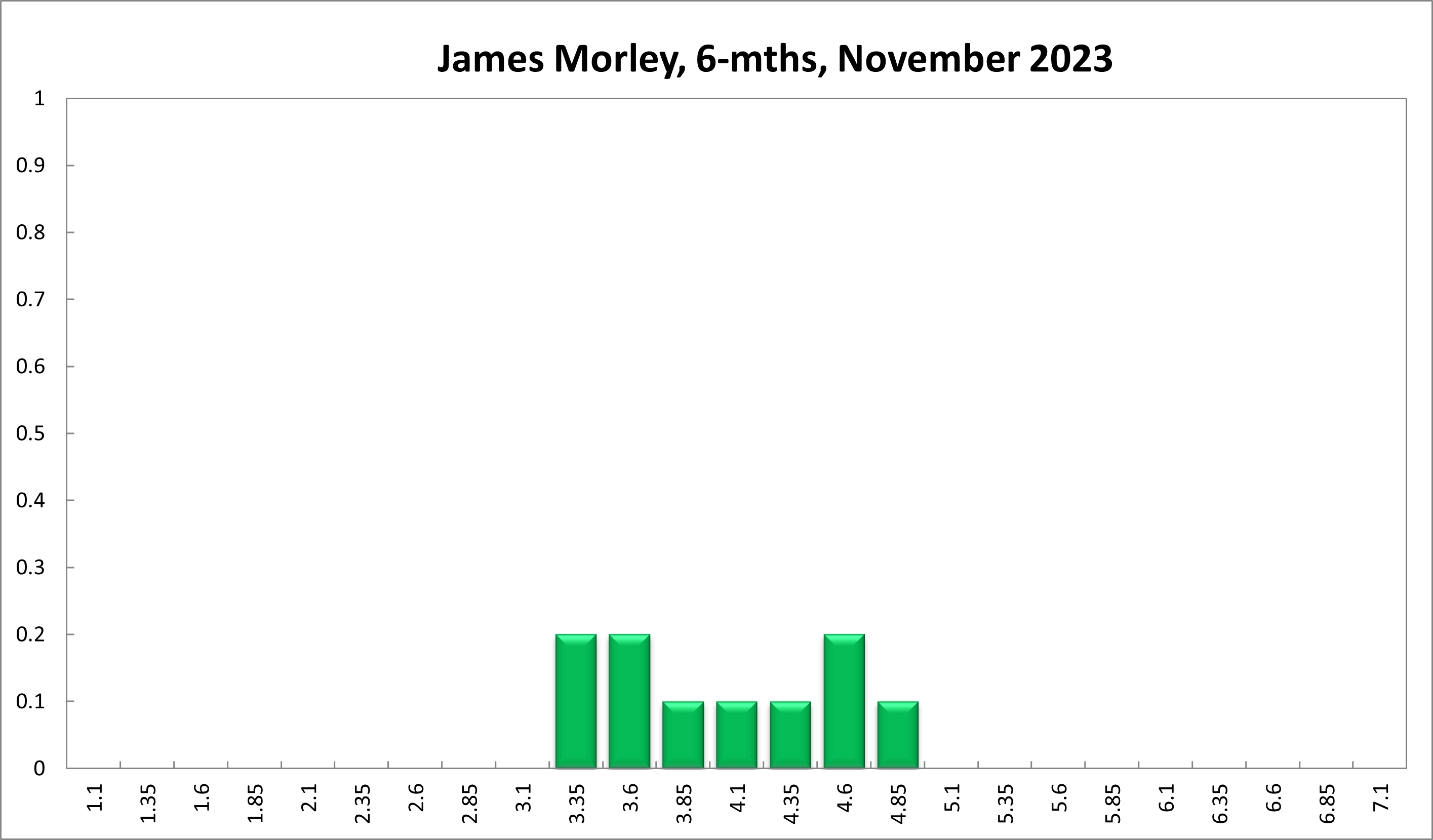

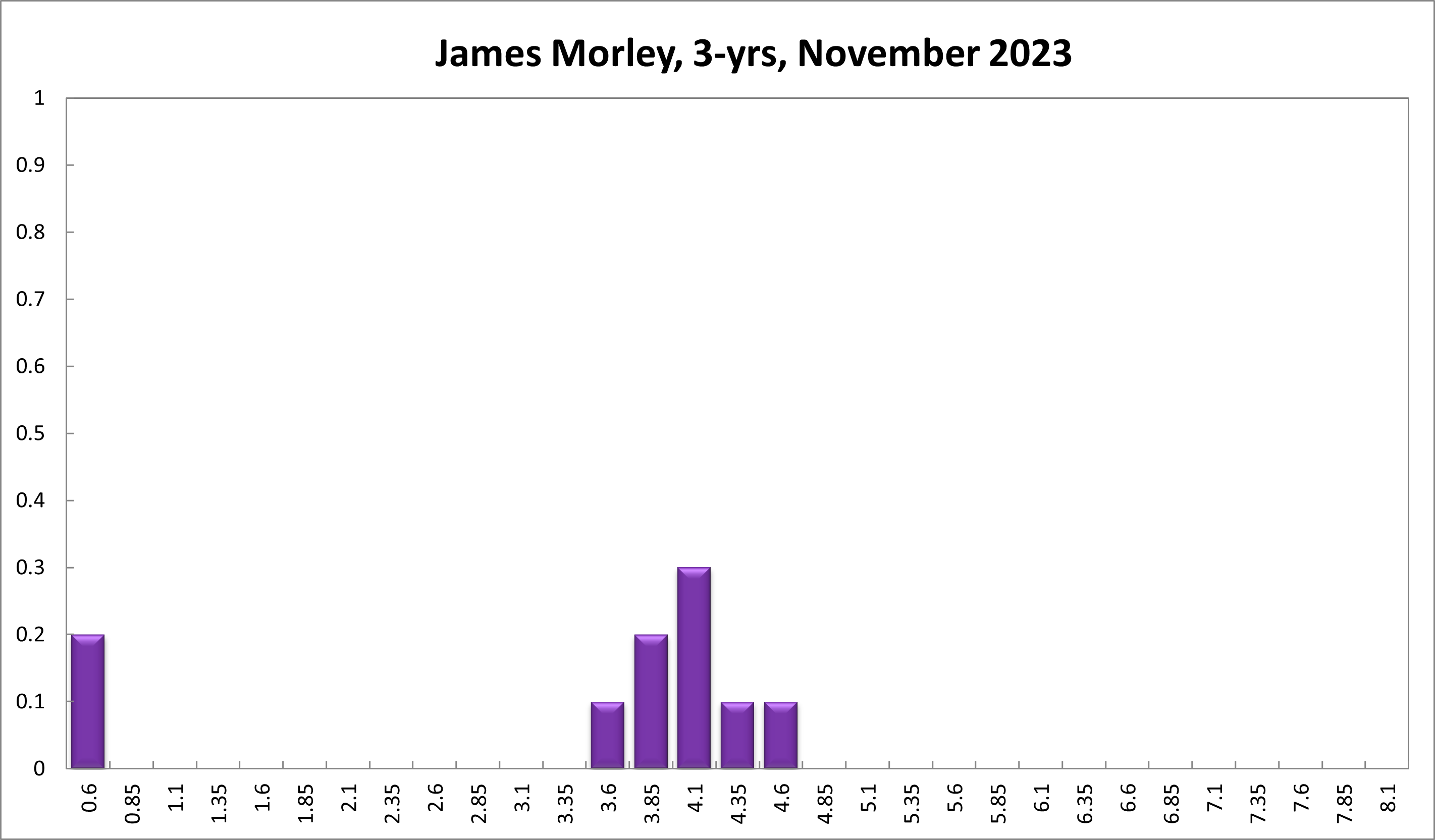

James Morley

The latest inflation report confirms that we are past the peak and inflation looks like it will gradually return to the RBA’s 2-3% target range. However, there are enough components of inflation that surprised on the upside in the report and the RBA will want to ensure longer-term inflation expectations remain anchored at low levels despite another spike in volatile energy prices that is hopefully less persistent than with the War in Ukraine. Also, more robust global economic conditions and domestic financial conditions both suggest the risk of recession is receding. Thus, the RBA has room to raise rates at the next meeting in response to inflationary pressures while still likely achieving a soft landing.

My recommendation puts a bit more weight on raising than holding steady, but the rise in geopolitical uncertainty means that risks of a global recession have not completely evaporated. Also, domestic demand is likely to continue to weaken given the past increases in interest rates. It is just that an upside surprise in the level of inflation should be met with a response to ensure real interest rates have their effects in cooling inflation and to help bring the level back to the target range. It will be important to monitor global inflation and demand conditions as well going forward as these appear to have an influence on Australia’s inflation. The RBA should not ignore components of inflation that are beyond their immediate control, but should offset them in whatever way necessary to ensure total headline inflation returns to the target range.

Updated: 26 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin