Besa Deda

The inflation report for the September quarter revealed upside inflation risks are materialising. Indeed, inflation could take longer to come down as a result. Headline inflation showed growth of 1.2% in the quarter, much faster than the 0.9% growth rate that the current forecasts from the RBA imply. In a recent speech, Bullock emphasised that the RBA would not tolerate a later return to the target band, which means the higher-than-expected inflation result has implications for the next policy decision on 7 November.

Bullock, the recently appointed Governor of the RBA, also took to the stand today before the Senate Legislative Committee. Bullock said services prices were still higher than the RBA was “comfortable with”.

The inflation report followed a recent update on the jobs market, which revealed a tick down in the national unemployment rate to close to a 50-year low of 3.6% in September. Whilst job vacancies are off their post-covid peaks, they are still elevated and some businesses are still struggling with shortages. It’s hard to find strong evidence that the unemployment rate is set to move above the rate consistent with full employment over the coming six months at least.

The low unemployment rate reflects the resilience of the economy. Households are tightening their belts and consumer spending growth is slowing, leading the weaker activity in the economy. However, strong population growth is injecting a layer of resilience.

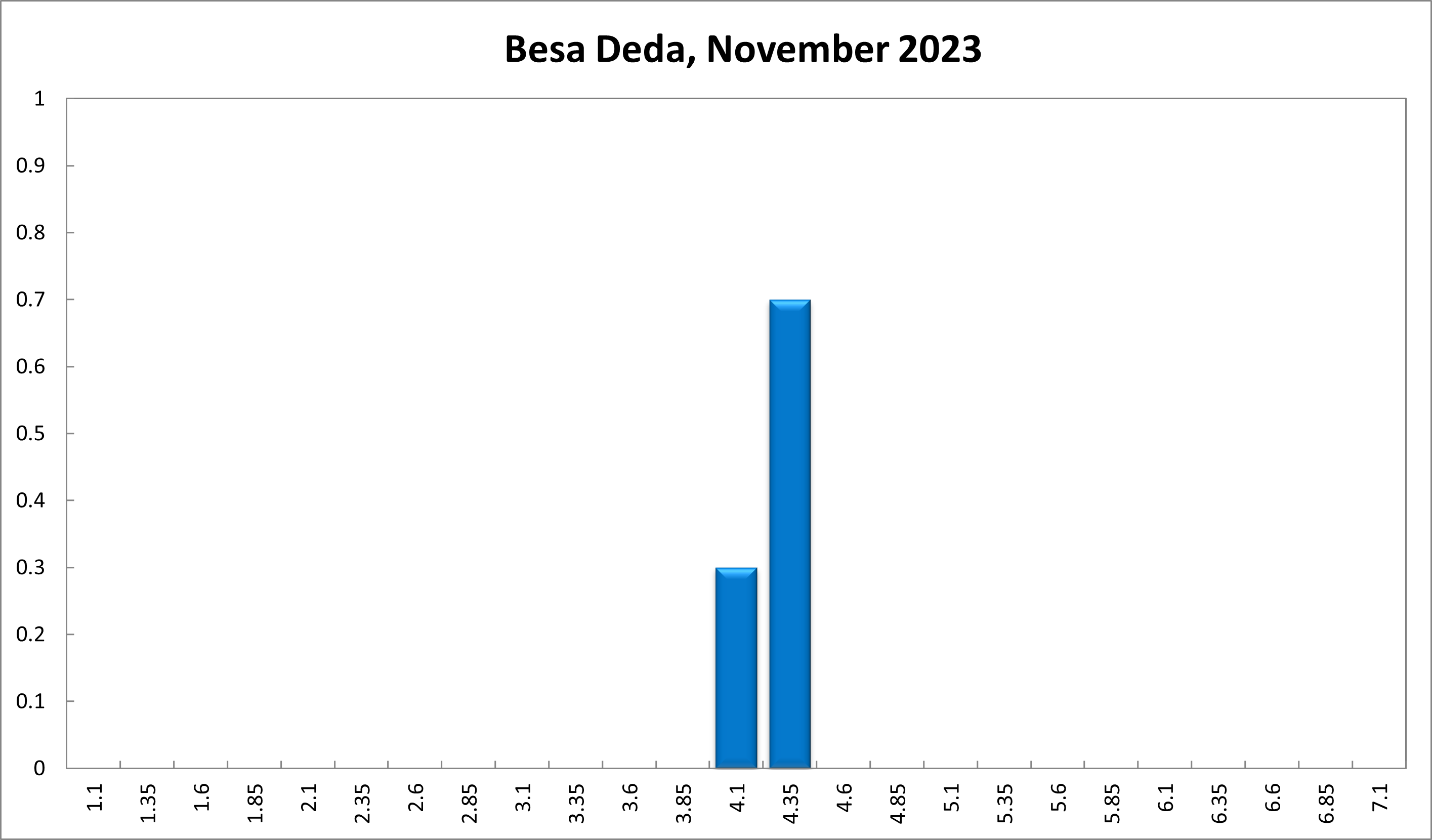

These mix of factors and data leaves the November board meeting as a live decision. In fact, we are left in no doubt that the Board will need to discuss a rate hike at the meeting. The discussion will boil down to whether they leave the cash rate unchanged or tap the brakes by 25 basis points to fine tune policy settings and ensure that inflation returns to the band in a timely manner.

The RBA will need to weigh up the slowdown in consumer spending growth against ongoing resilience from businesses and determine how much of the surprise outcome in inflation was due to temporary factors versus permanent drivers. In our opinion, there were more permanent drivers at play. For example, around 75% of prices economy-wide are growing at an annual rate that is faster than the midpoint of the RBA’s inflation target band. This share has come down from the peak, but remains high and progress lower appears to have stalled.

Since the rate-hike cycle began in May of last year, one variable has ranked consistently high on the RBA’s watch list. That variable is inflation expectations, especially over the medium term. The RBA wants to ensure that inflation expectations do not become de-anchored. Higher than expected prints on inflation can contribute to a flare up in inflation expectations. There is some evidence in recent weeks that medium-term inflation expectations have begun to tick up, suggesting the RBA may need to lean in to arrest the trend.

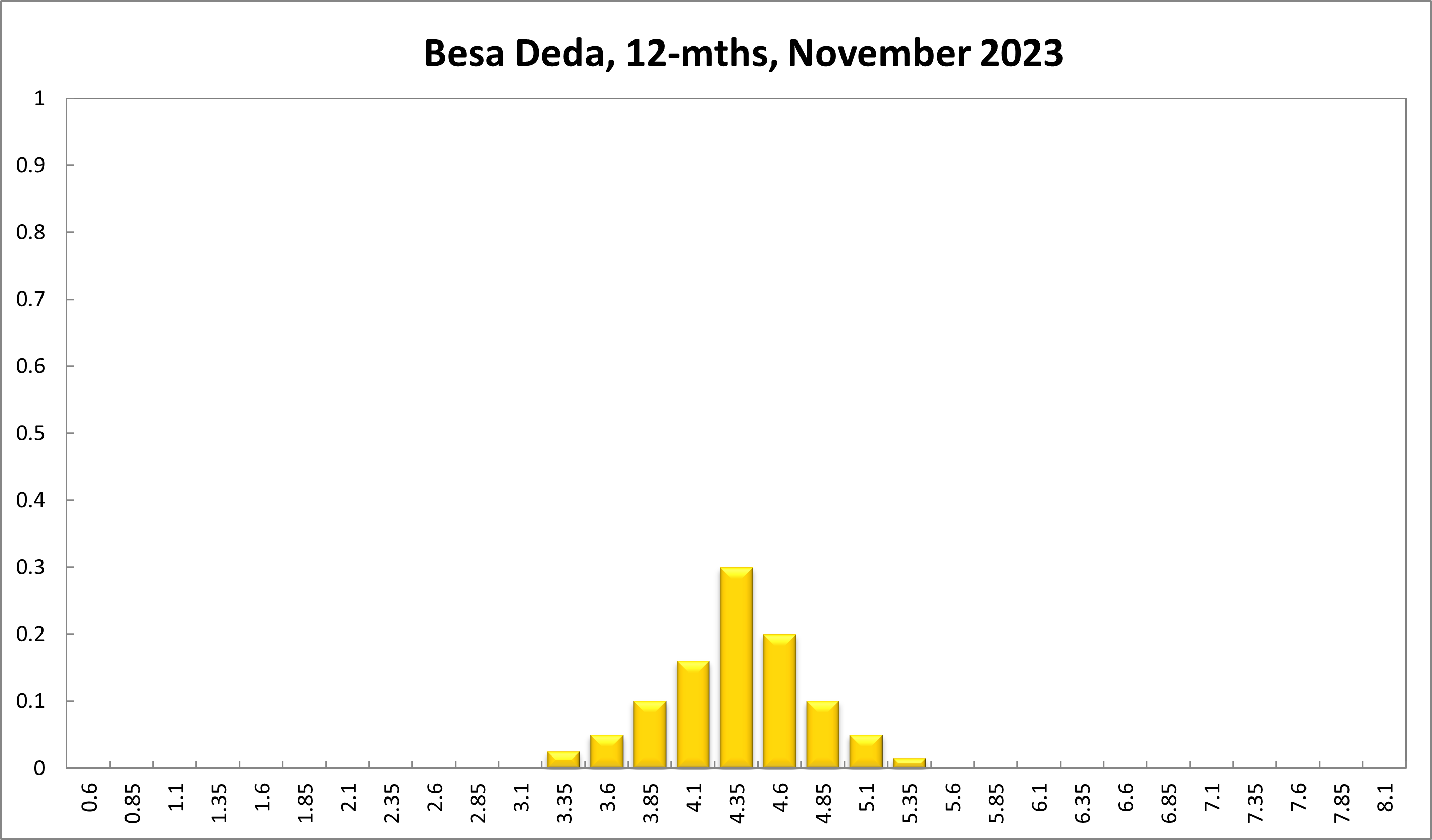

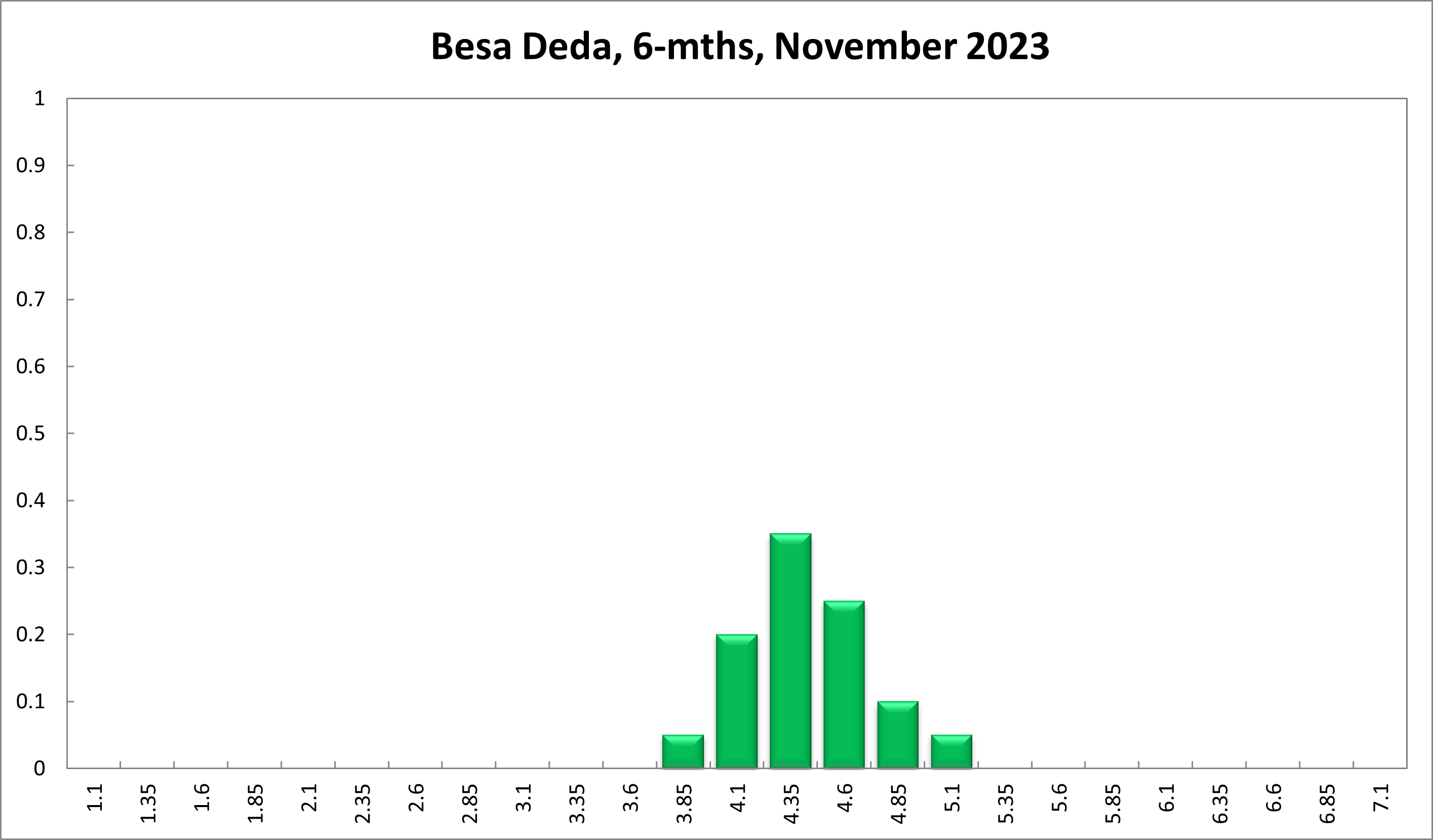

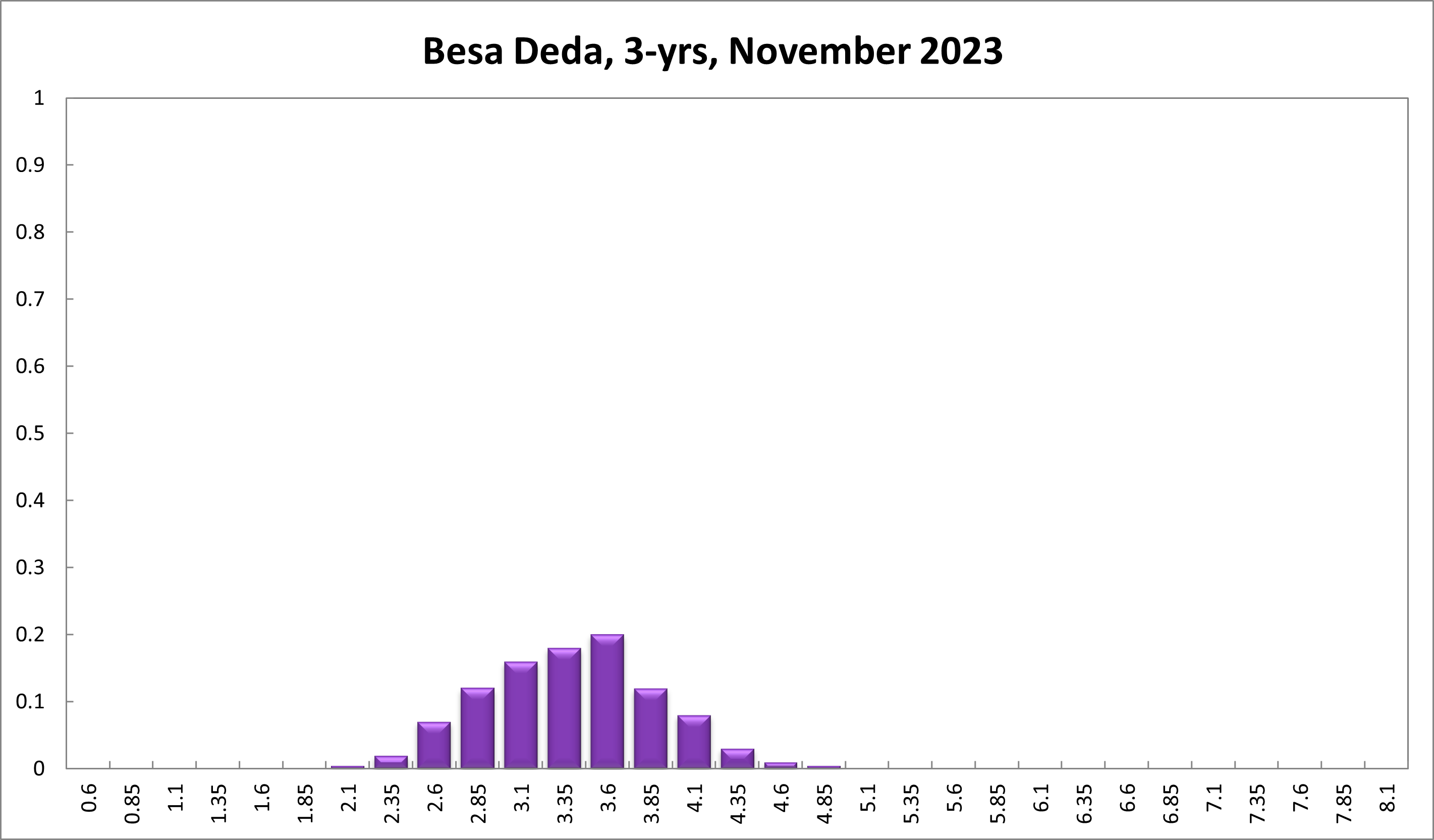

Reflecting the changing balance of risks, we believe the odds have shortened considerably for a rate hike on Melbourne Cup Day. Is this one hike and done? Quite possibly, but the high uncertainty attached to forecasts in the current environment means further tightening in the next six months cannot be fully ruled out. The incoming data remains key.

Updated: 27 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin