Aggregate

Another 50 bps Rise Called For

Domestically, many economic indicators remain quite strong: the labour market is tight, the capacity utilisation rate is high, business confidence is mostly sanguine. But there are clear headwinds on the horizon, as recent interest rate rises start restraining spending and global risks reduce external demand. With the most recent print of the inflation rate (6.1% in Q2 of 2022 for headline CPI and 4.9% for core inflation) well above the RBA’s target band of 2-3%, the broad consensus calls for further monetary tightening. The RBA Shadow Board strongly advocates in favour of further interest rate increases. It is 88% confident that the overnight rate should be raised to above the current setting of 2.35%, with a mode recommendation of a 50 bps increase, whilst only attaching an 11% probability that keeping the overnight rate on hold this round is the appropriate policy.

Australia’s seasonally adjusted unemployment rate ticked up, from 3.4% in July 2022, to 3.5% in August. Total employment increased by 33,500, and the labour participation rate, increased also, to 66.6%. Total monthly hours worked in all jobs rose by 14 million, or 0.8%. The underemployment rate fell to 5.9%, and job vacancies and job advertisements remain strong. Overall, the Australian labour market continues to perform. There has been no new data on wage price growth.

Throughout September, the Australian dollar continued to weaken, trading below 65 US¢, a new two-year low. This is the result of the US Federal Reserve increasing the interbank rate more aggressively than the RBA and other central banks. Yields on Australian 10-year government bonds continued to rise, pausing just below 4% at the end of September. Yield curves retain their normal convexity. The spread between 10-year versus 2-year bonds narrowed a little, to 44 bps. Australian stock prices rebounded briefly at the beginning of the month, only to fall sharply, testing the low made in June. The S&P/ASX 200 stock index looks to have found some support around the 6,500 mark.

Consumer confidence arrested its nine-month decline: the Melbourne Institute and Westpac Bank Consumer Sentiment Index recovered slightly, from 81.2 to 84.4. Private sector credit remained steady, whereas August retail sales softened. Business confidence remains positive; NAB’s index of business confidence improved from 8 to 10, as did the services PMI (from 51.7 to 53.3, August); the S&P Global Australia Composite PMI improved slightly (from 50.2 to 50.8, September). The capacity utilisation rate remains just shy of its all-time high of 86.68%. On the downside, the six-month annualised growth rate of the Westpac-Melbourne Institute Leading Economic Index, which is interpreted as the likely pace of economic activity relative to the trend in six to nine months, fell to -0.36% in August. This is the first time since the big lockdown in 2021 that the number is negative.

Risks to the global economy remain elevated and are unlikely to go away any time soon. Inflation is uncomfortably high everywhere, leading most central banks, led by the Federal Reserve, to tighten monetary policy sharply. Widespread downturns are likely, with a recession in Europe seen as a near certainty, especially as demand for natural gas going into winter increases. The Ukraine war is likely to cause further disruptions, as are other geopolitical tensions, gumming up supply chains and raising risk premia. International capital, which Australian financial markets rely on, will become more expensive as a consequence.

Five months ago, the Reserve Bank of Australia embarked on a tightening cycle after the official cash rate target stood at the historically low level of 0.1% for one-and-a-half years. For the current (October) round, the Shadow Board is advocating that the overnight interest rate be raised further, above the current level of 2.35%, attaching an 88% probability that this is the appropriate policy stance. It attaches an 11% probability that keeping the overnight rate on hold is the appropriate policy and a mere 2% probability that a decrease is appropriate.

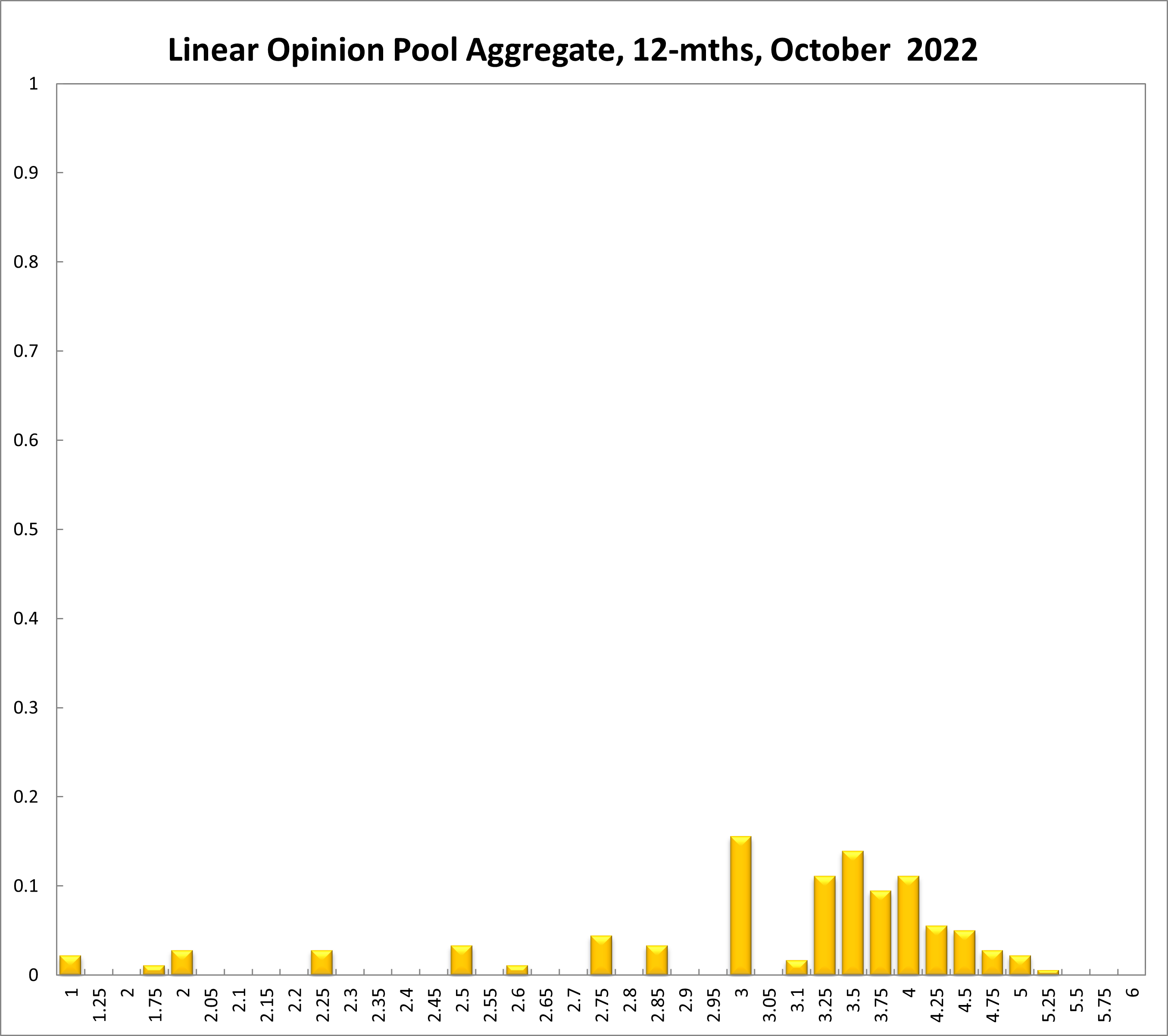

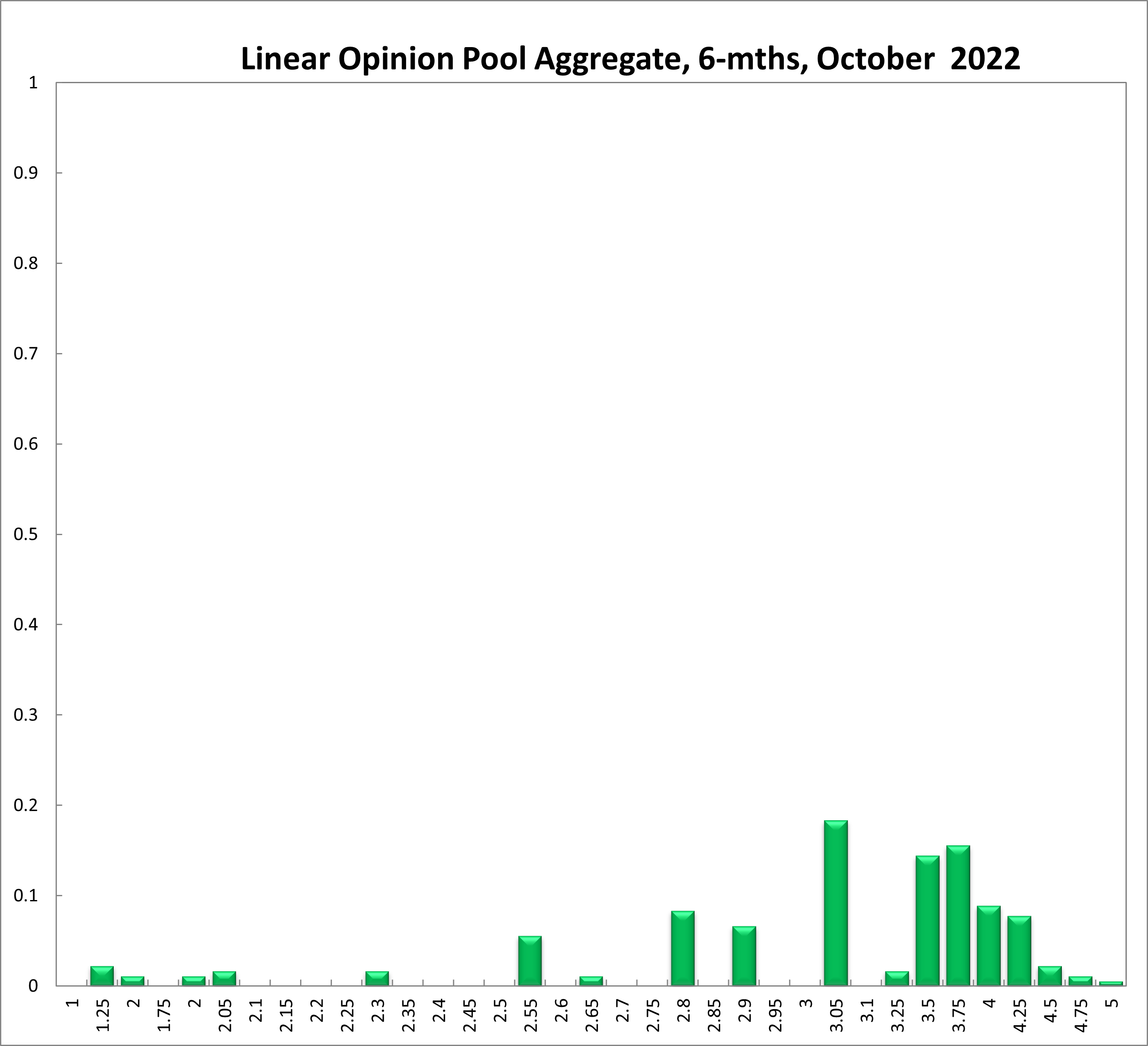

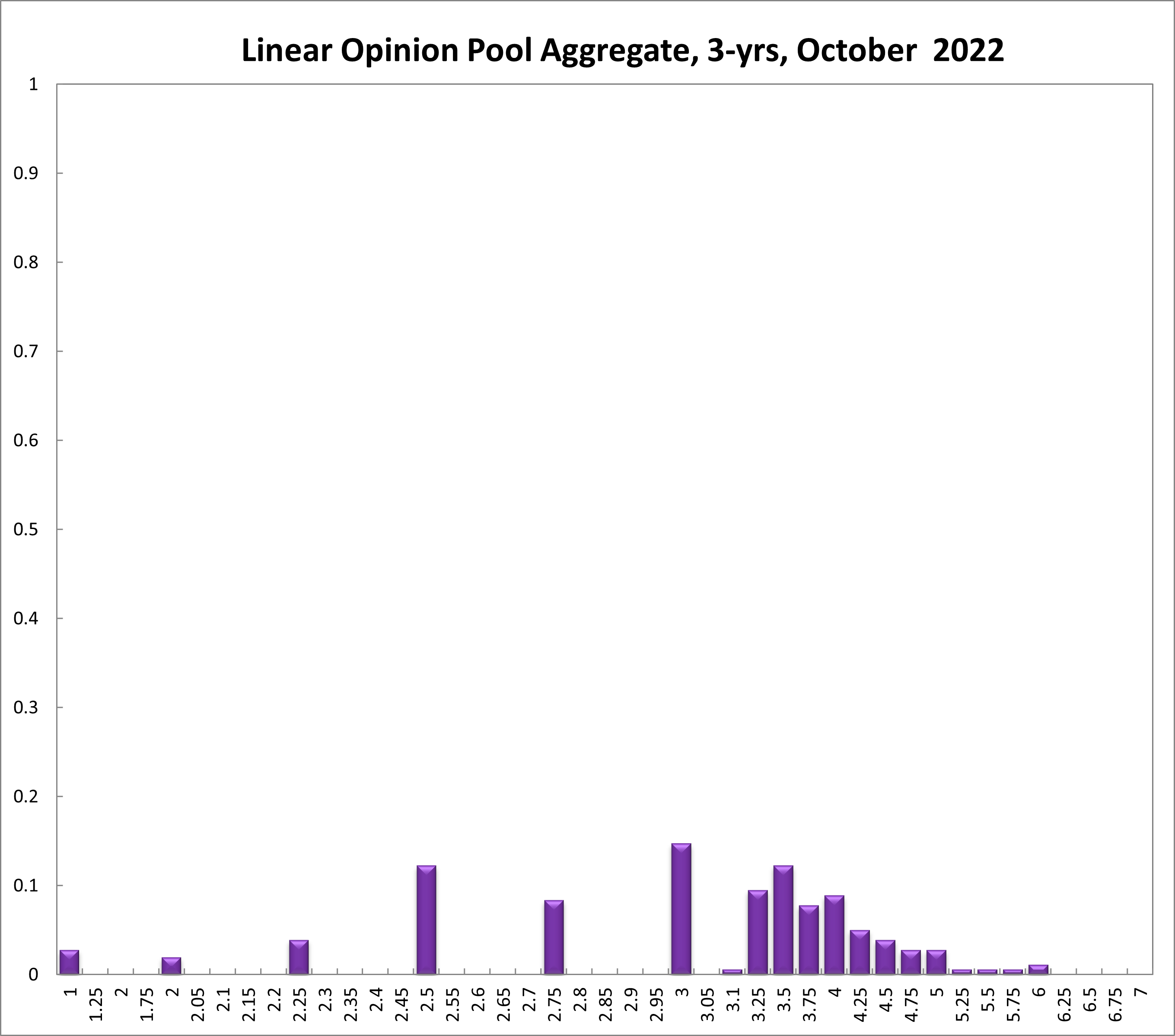

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at the current setting of 2.35% equals 0%; the probability attached to the appropriateness of an interest rate decrease equals 8%, while the probability attached to a required increase equals 92%. One year out, the recommendations are similar. The Shadow Board members’ confidence that the appropriate cash rate is 2.35% equals 0%. The confidence in a required cash rate decrease, to below 2.35%, is 9% and in a required cash rate increase, to above 2.35%, equals 91%. Three years out, the Shadow Board attaches a 0% probability that the overnight rate should equal 2.35%, a 9% probability that a lower overnight rate is optimal and a 91% probability that a rate higher than 2.35% is optimal.

The range of the probability distributions for the current and 6-month recommendations has widened considerably: for the current setting, it extends from 2.25% to 4.25% (compared to a range of 1.85% and 3.00% in the previous round) and for the 6-month horizon it extends from 1.25% to 5.00% (compared to a range of 1.5% to 4.25% in the previous round). The range for the 12-month horizon extends from 1.0% to 5.25%. For the 3-year horizon the range, now extending from 1.0% to 6.0%, actually narrowed slightly.

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin