Sarah Hunter

The incoming data continues to show the underlying strength in the economy. While it will take a little longer for WPI wages growth to pick-up, due to the sticky nature of collective agreements and the award wage process, there are clear signs of momentum in the private sector (particularly in construction, professional services and parts of manufacturing). These trends are likely to be reinforced by the inflationary environment globally, with many local businesses now looking to pass on rising costs to final consumers.

Set against the backdrop of an upcoming election, the Federal budget included tax cuts and increased transfers for households; the strength of the economic recovery and the tailwind from elevated commodity prices means that despite these measures (and increases in funding for infrastructure, healthcare and cyber security) the deficit is not projected to worsen in FY23. While these payments will help offset the rising cost of living, given that the economy is operating close to full employment (and generating some domestic inflationary pressures as a result) there is a risk that they further fuel inflation.

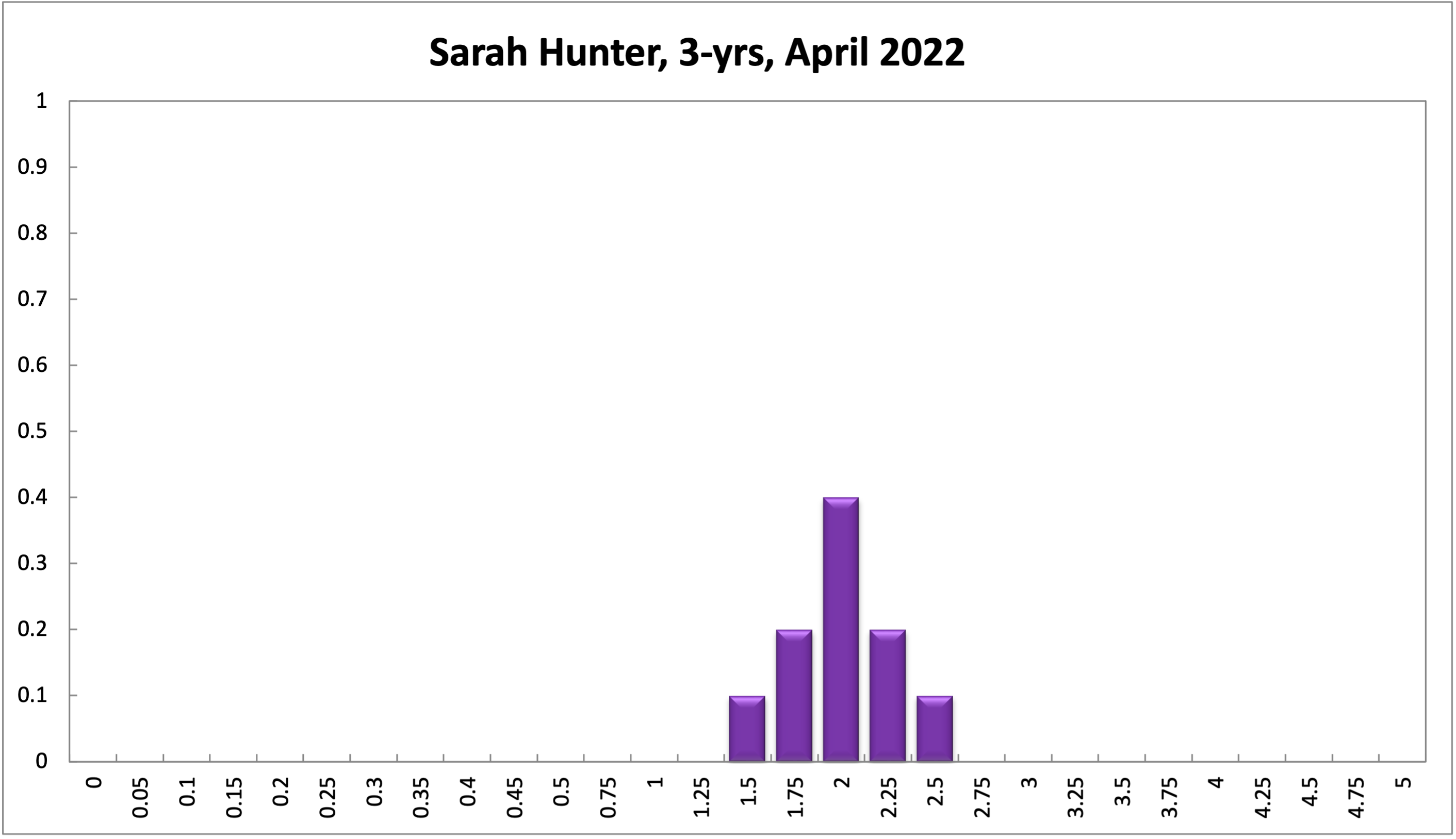

Given current conditions, it is appropriate for the RBA to begin raising the cash rate in the very near term, and to proceed with a steady pace of monetary tightening into 2023. While growth momentum will naturally ease in H2 2022 and again in 2023 as fiscal policy tightens, the RBA will need to return the cash rate to a broadly neutral stance over the medium term to ensure that inflation remains in check.

Updated: 18 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin