Outcome

The recovery in the labour market continues to be strong, and the forward looking indicators for employment remain very healthy, suggesting that the current policy stimulus measures (fiscal and monetary) have been very effective at driving the recovery. Given this, an expansion of the monetary supports is not warranted at this time.

There are still hurdles for the economy to jump though. The end of JobKeeper will naturally lead to some people being made redundant. The key question will be whether these people are able to transition into the sectors/regions where there are job vacancies. The fact that job vacancies have risen in recent months but the number of people unemployed remains elevated compared to pre-COVID (notwithstanding a sharp fall in February) suggests that for some workers at least this transition isn’t seamless. Given this, it will likely be some time before full employment is reached.

Furthermore, although it is recovering domestic demand is still relatively subdued. Household spending on services has not fully recovered, and business investment intentions (particularly with respect to building construction) are still depressed.

It would be premature to remove monetary supports from the economy right now, and non-traditional policies (such as QE and the 3 year government bond yield target) should be unwound first. As such, I would not change the cash rate over the next 12 months. Beyond this, the better than anticipated recent data potentially warrants bringing forward the first rate rise if the upside outcomes are maintained. But there is still considerable uncertainty about how the recovery will play out from here, what the Federal government will do to the fiscal policy stance and when some certainty about domestic and international restrictions can be removed.

The improvement in various economic conditions suggests that the RBA will be able to begin liftoff from the effective lower bound in early 2024. The exact timing and speed of liftoff will depend on whether they have achieved a sustainable return of inflation to their 2-3% target range and where inflation is in the target range. If the RBA has not achieved the return of inflation to the target range by early 2024, they should extend keeping the cash rate at the effective lower bound until inflation does return to the target range. If inflation exceeds the target range well before 2024, they should start liftoff earlier. My forecast is that inflation and measures of inflation expectations are most likely to be within the lower half of the target range by the beginning of 2024, which would call for a gradual liftoff back to neutral that allows inflation to run at the higher end of the target range. This gradual liftoff would let the price level return back up to a general path for it based on 2-3% inflation per year from when the cash rate hit the effective lower bound in response to the COVID-19 crisis.

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Overnight rate to stay at all-time low despite economy improving, Shadow Board finds

By international comparison, Australia seems to be managing the Covid-19 crisis well, which is reflected in steadily improving economic indicators such as the recent fall in the official unemployment rate from 6.4% to 5.8%. The most recent data on inflation are still from the December quarter, putting the ABS CPI estimate at 0.9%, year-on-year, well below the RBA’s official target band of 2-3%. The RBA Shadow Board’s conviction that the cash rate should remain at the historically low rate of 0.1% remains exceptionally strong: it has virtually no doubt that this is the appropriate interest rate setting.

The headline labour market statistics continue to improve. The official ABS unemployment rate fell significantly from 6.4% in January to 5.8% in February. In the same period, total employment increased by 88,700, almost all attributable to a change in full-time employment. Youth unemployment fell a full percentage point, to 12.9%. Job advertisements ticked up while the labour force participation rate remained steady at 66.1%. JobKeeper assistance terminated at the end of March; without this assistance and the economy remaining weak in some sectors, especially the entertainment, hospitality and tourism industries, unemployment is likely to rise again during the next few months.

The Aussie dollar has retreated from its recent highs, falling back to 76 US¢. Yields on Australian 10-year government bonds rallied considerably in February and held firm in March, settling in the 1.7-1.8% range. The shapes of the yield curves remain unchanged: the yield curve in short-term maturities (2-year versus 1-year) is flat, a deliberate policy by the Reserve Bank of Australia; in mid-term versus short-term maturities (5-year versus 2-year) and in higher-term maturities (10-year versus 2-year) the yield curves display normal convexity. The spread between the 10-year rate and the 2-year rate is now 167 basis points, marginally smaller than at the end of February. The stock market, after its extended climb, has largely traded sideways. The S&P/ASX 200 stock index is oscillating between 6650 and 6850.

The unfolding of Covid-19 remains central to the outlook for global growth. The pace of vaccine rollout is much slower than anticipated and hoped for in most countries, not least in Australia. New virus strains, some more virulent than the original strains, are forcing countries in repeated lockdowns. There have been no significant revisions to projections of world GDP growth, with the International Monetary Fund recently holding on to its forecast of 5.5% for 2021 and 4.2% for 2022. The political tensions between China and the US, as well as other Western nations, continue to probe Australia’s reliance on China as a major destination for her exports.

Consumer confidence edged up slightly: the Melbourne Institute and Westpac Bank Consumer Sentiment Index rose 3 points, to 112. Retail sales (month-on-month) contracted by 0.8% in February. NAB’s index of business confidence improved from 12 in January to 16 in February; the manufacturing and services PMI increased from 58.8 to 59.9 and from 54.3 to 55.8, respectively. Promisingly, capacity utilisation increased by almost a full percentage point, to 81.81% in February, which is what it was prior to the Covid-19 pandemic.

The strength of the housing market is unabated, with house prices having jumped 2.1% in February, the biggest month-on-month gain in almost 18 years, according to CoreLogic. In the same month, building permits increased by 21.6%. The AI Group/HIA Australian Performance of Construction Index was largely unchanged. The continuous rise in house prices is raising concerns of a dislocating housing bubble, which the RBA has also recently acknowledged. Governor Phil Lowe has reiterated that the RBA will not explicitly target house prices, arguing, as several Shadow Board members have in the past, that the appropriate policy lever to reign in house prices is through macroprudential policies, not the overnight interest rate.

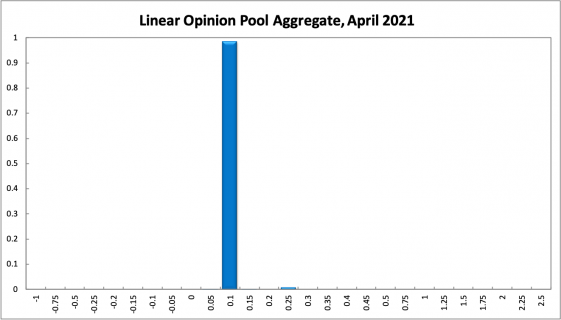

Since November the official cash rate target has been at the unprecedented level of 0.1%. The Shadow Board’s exceptionally strong conviction to keep the overnight interest at 0.1% is carrying over into the current interest rate round. The Shadow Board attaches a 99% probability that the overnight interest rate should remain steady, a mere 1% probability that an increase is appropriate and a 0% probability that a further rate cut to below 0.1% is appropriate.

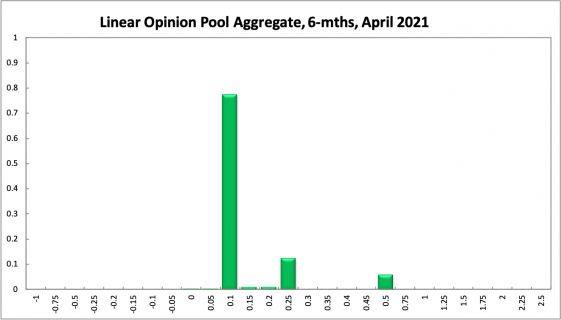

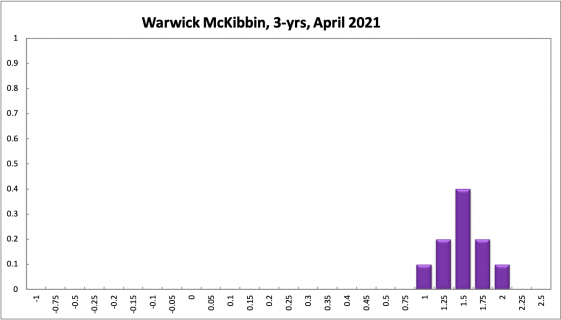

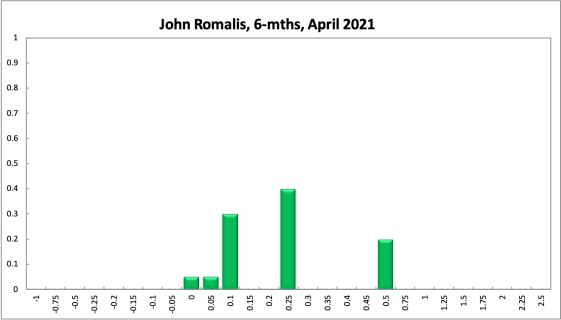

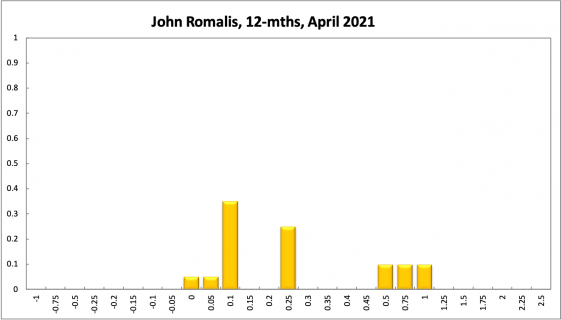

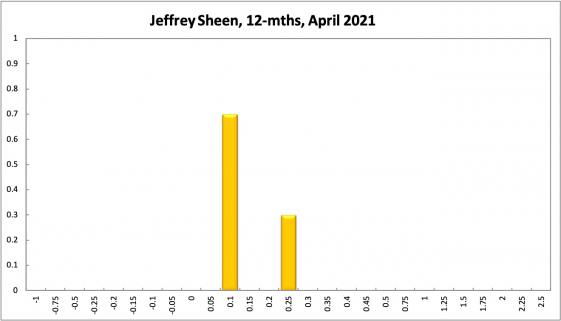

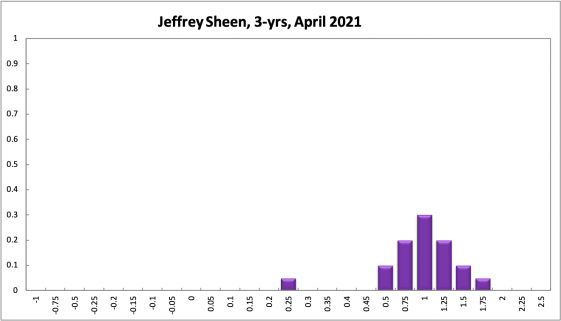

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at 0.1% equals 78% (79% in March), the probability attached to the appropriateness for an interest rate decrease fell from 2% to 1%, while the probability attached to a required increase is 21% (19% in March). One year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 72% (75% in March). The confidence in a required cash rate decrease, to below 0.1%, is 1% (unchanged from March) and in a required cash rate increase 27% (23% in March). Three years out, the Shadow Board attaches a 13% (21% in March) probability that the overnight rate should equal 0.1%, an unchanged 1% probability that a rate lower than 0.1% is appropriate, and a 87% (79% in March) probability that a rate higher than 0.1% is optimal. The range of the probability distributions over the 6 month and 12 month horizons spans from 0% to 1.0%, the range of the probability distribution for the 3-year recommendation is wider, extending from 0% to 2.5%.