Outcome

Monetary policy should remain very accommodative for the foreseeable future. Notwithstanding the strength of the recovery in the labour market thus far, there are now signs that the initial rebound is coming to an end and the economy is still some way from full employment (employment growth in NSW has stagnated in recent months, for example). Given the likely need for the unemployment rate to fall to 4.5% (or lower) before a sustained, broad-based acceleration in wages growth is seen, the RBA should continue to provide support in order to stimulate activity levels.

Measures of underlying inflation remain below the RBA’s target band of 2 - 3 per cent. Although monetary policy settings in Australia are expansionary, the recent increase in commodity prices together with expansionary monetary policy in the United States have contributed to a significant appreciation of the Australian dollar in recent months. A stronger Australian dollar will reduce inflation further through a reduction in non-tradable inflation. With inflation persistently below target and slack in the labour market there is a risk that long-run inflation expectations become anchored at a permanently lower level. Monetary policy must therefore increase the degree of policy accommodation by extending the duration of its zero interest rate policy.

The current forward guidance by the RBA is clear in terms of expecting to maintain the cash rate at the effective lower bound for at least three years and emphasising a link to inflation being higher than currently and sustainably within the 2-3% target range. Given some recent signs of improving global economic conditions and continued fiscal support for economies such as the United States, it is possible that “liftoff” for the main policy rate (the overnight cash rate) could commence in early 2024. Thus, it may be helpful to modify the guidance language to be even more “calendar-based” in the sense of specifying the overnight cash rate is expected to remain at the effective lower bound until at least the end of 2023. It would also be helpful in managing expectations to allow that inflation may temporarily exceed the target range before liftoff away from the effective lower bound would occur.

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Shadow Board without doubt that overnight rate must remain steady

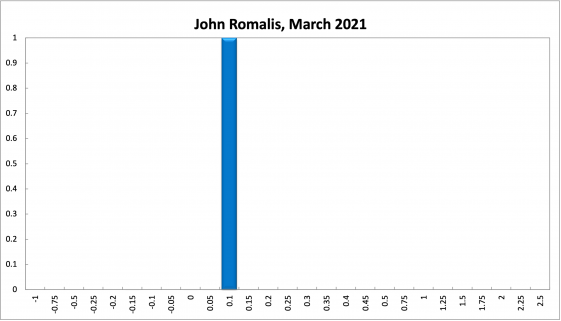

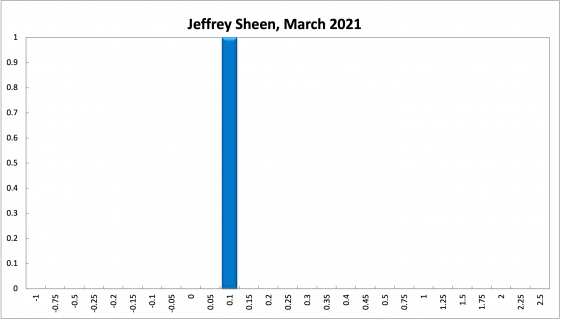

Australia’s economy appears to continue on its slow, steady path of recovery. The most recent data on inflation are from the December quarter, putting the ABS CPI estimate at 0.9%, year-on-year, well below the RBA’s official target band of 2-3%. The RBA Shadow Board’s conviction that the cash rate should remain at the historically low rate of 0.1% is, for the first time, unqualified: it has no doubt that this is the appropriate interest rate setting.

The labour market continues to improve, at least for the time being. The official ABS unemployment rate fell from 6.6% in December to 6.4% in January. In the same period, employment rose by 29,100, lower than expected. Full-time employment increased by 59,000, while part-time employment shrank by 29,800. Youth unemployment was steady at 13.9%, job advertisements ticked up and the labour force participation rate edged down to 66.1%. The unwinding of Jobkeeper and Jobseeker assistance may well affect these numbers going forward.

The Aussie dollar extended its steady climb, nearly reaching the 80 US¢ mark. Yields on Australian 10-year government bonds rallied considerably in February, from around 1.15% in late January to 1.88% four weeks later. While the yield curve in short-term maturities (2-year versus 1-year) remains flat, which is a deliberate policy by the Reserve Bank of Australia, in mid-term versus short-term maturities (5-year versus 2-year) and in higher-term maturities (10-year versus 2-year) the yield curves are convexifying further. The spread between the 10-year rate and the 2-year rate is now 175 basis points. The stock market likewise posted some modest gains, with the S&P/ASX 200 stock index briefly breaching 6,900. All this points to the markets revising their forecasts for the Australian economy upwards.

The second and third waves of Covid-19 continue to dominate the outlook for global growth. The rollout of various vaccines is clearly a welcome development but it has not been as quick as hoped. Moreover, the emergence of new variants of the virus, perhaps more resistant to some of the vaccines, is cause for concern. The International Monetary Fund recently forecast the global economy to grow 5.5% in 2021 and 4.2% in 2022, a slight upward revision to the previous forecasts. These forecasts are premised on effective and coordinated policy actions to handle the pandemic and acknowledge the uneven variation of growth across countries.

Trade tensions and geopolitical fissures between Australia and some of its trading partners, principally China, are unlikely to go away soon; they will continue to affect Australia’s current account and GNI.

Consumer confidence barely budged since last month: the Melbourne Institute and Westpac Bank Consumer Sentiment Index currently stands at 109, up a mere two points relative to the previous month. Retail sales (month-on-month) were mildly positive in January remain.

NAB’s index of business confidence improved from 5 in December to 10 in January, while the manufacturing and services PMI stayed put. Capacity utilisation continued to increase, reaching 80.96% in January, which is not far off the level just prior to the Covid-19 pandemic hitting Australia.

The housing market is showing further signs of strength. According to CoreLogic, the 5 capital city aggregate home value index rose by nearly 3.5%, quarter-on-quarter. New home sales fell to 4,143 units in January, after an aberrant jump in December, which presumably reflects the more generous terms of the HomeBuilder program until 31 December 2020. The AI Group/HIA Australian Performance of Construction Index was unchanged. In previous statements, some shadow board members have explained that the appropriate policy lever to reign in house prices is through macroprudential policies, not the overnight interest rate.

Since November the official cash rate target has been at the unprecedented level of 0.1%. For the first time since its inception, the Shadow Board is now effectively unconditional in its conviction that the overnight rate should be held steady. Last month, the Shadow Board still attached an 11% probability that the overnight interest rate should be than 0.1% and a 0% probability that a further rate cut to below 0.1% is appropriate.

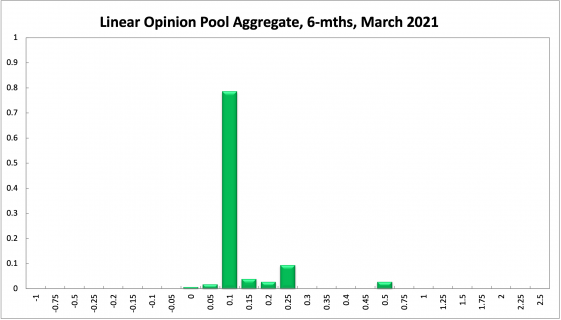

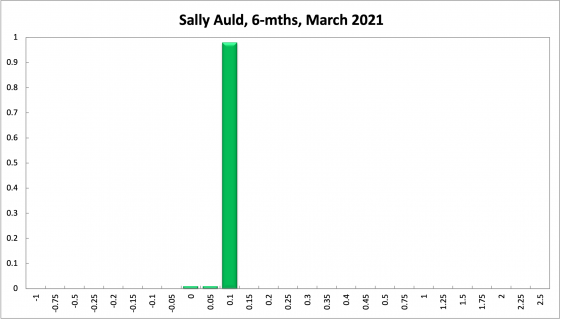

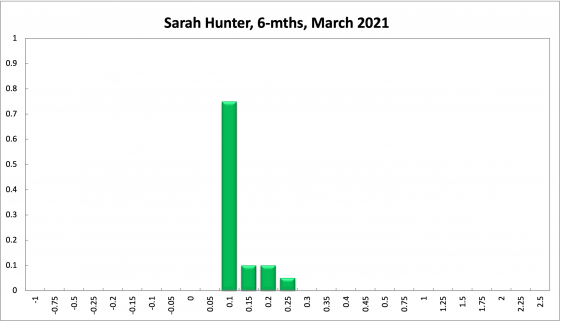

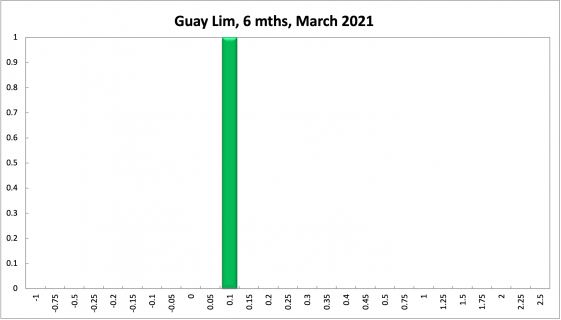

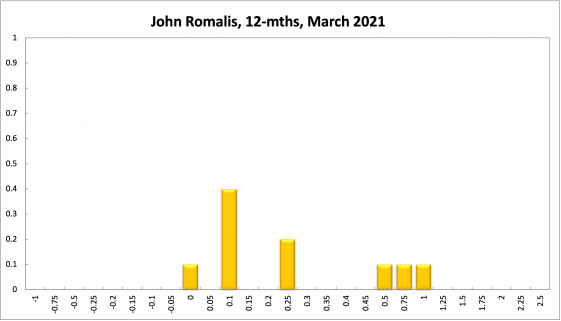

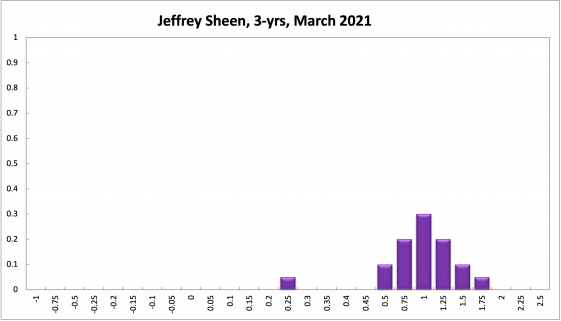

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at 0.1% equals 79% (65% in February), the probability attached to the appropriateness for an interest rate decrease is unchanged at 2%, while the probability attached to a required increase is 19% (33% in February). One year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 75% (51% in February). The confidence in a required cash rate decrease, to below 0.1%, is 14% (1% in February) and in a required cash rate increase 23% (48% in February). Three years out, the Shadow Board attaches a 21% probability that the overnight rate should equal 0.1% (24% in February), a unchanged 1% probability that a rate lower than 0.1% is appropriate, and a 79% probability that a rate higher than 0.1% is optimal (75% in February). The range of the probability distributions over the 6 month and 12 month horizons spans from 0% to 1.0%, the range of the probability distribution for the 3-year recommendation is wider, extending from 0% to 2.5%.