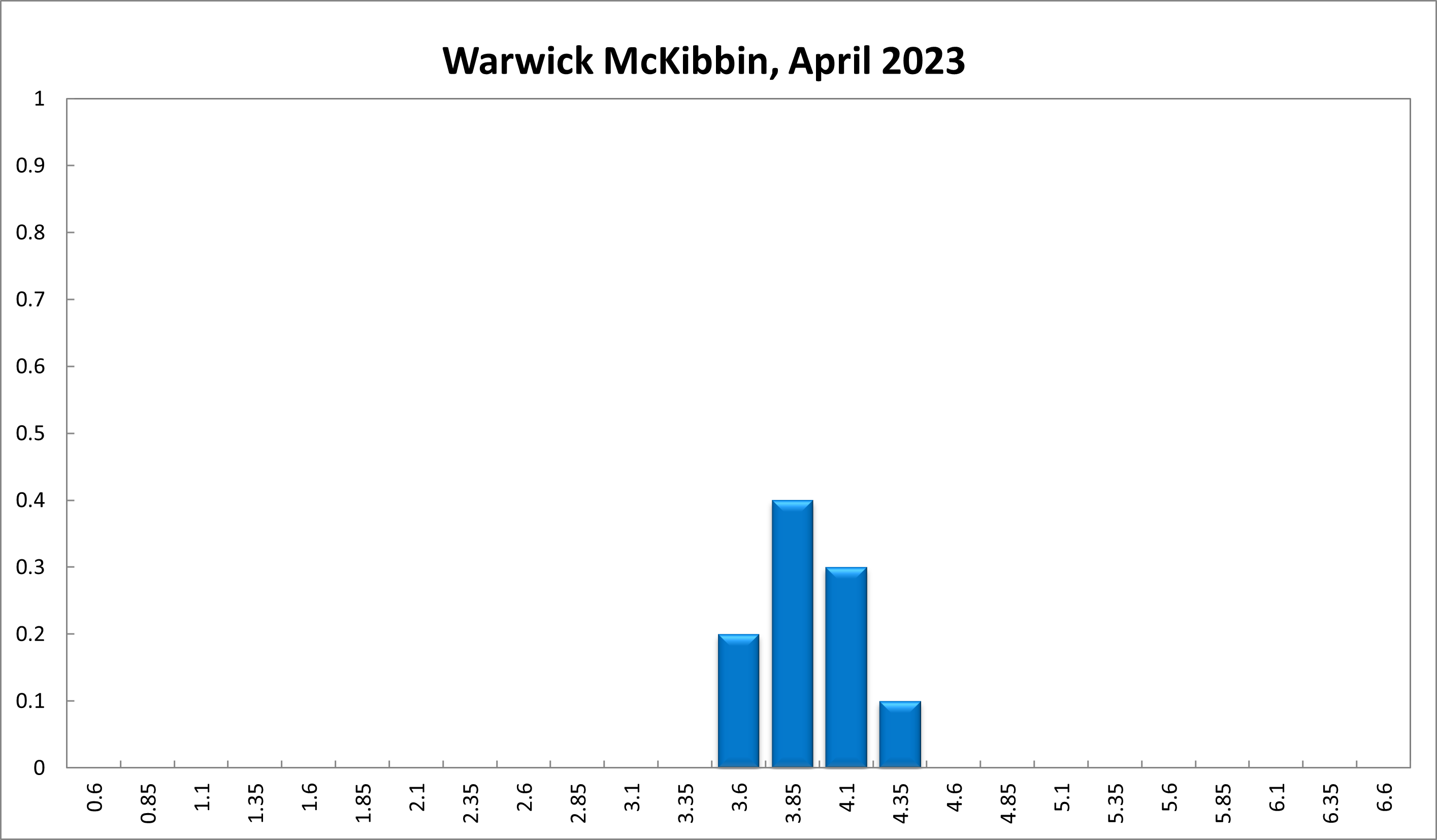

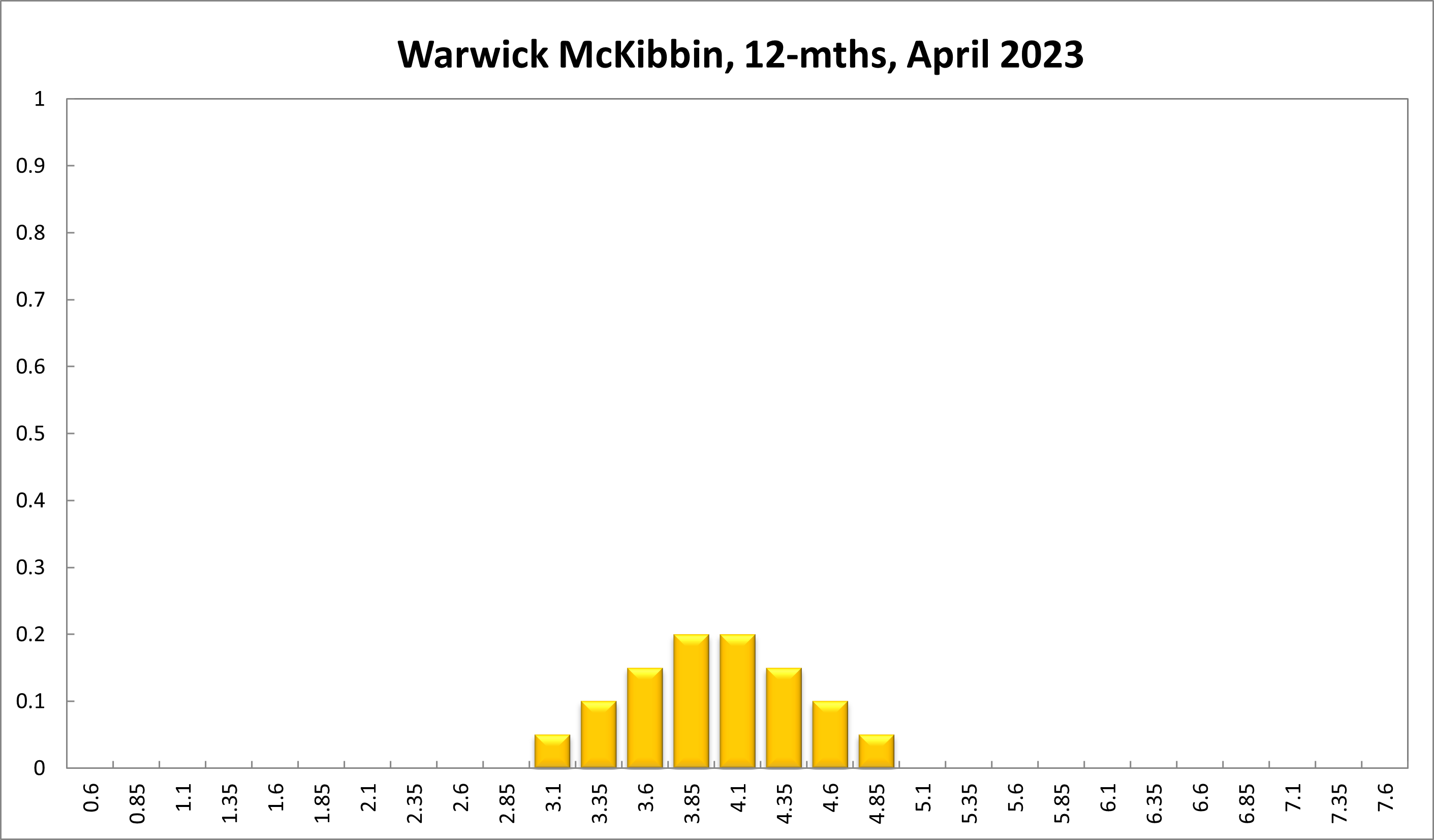

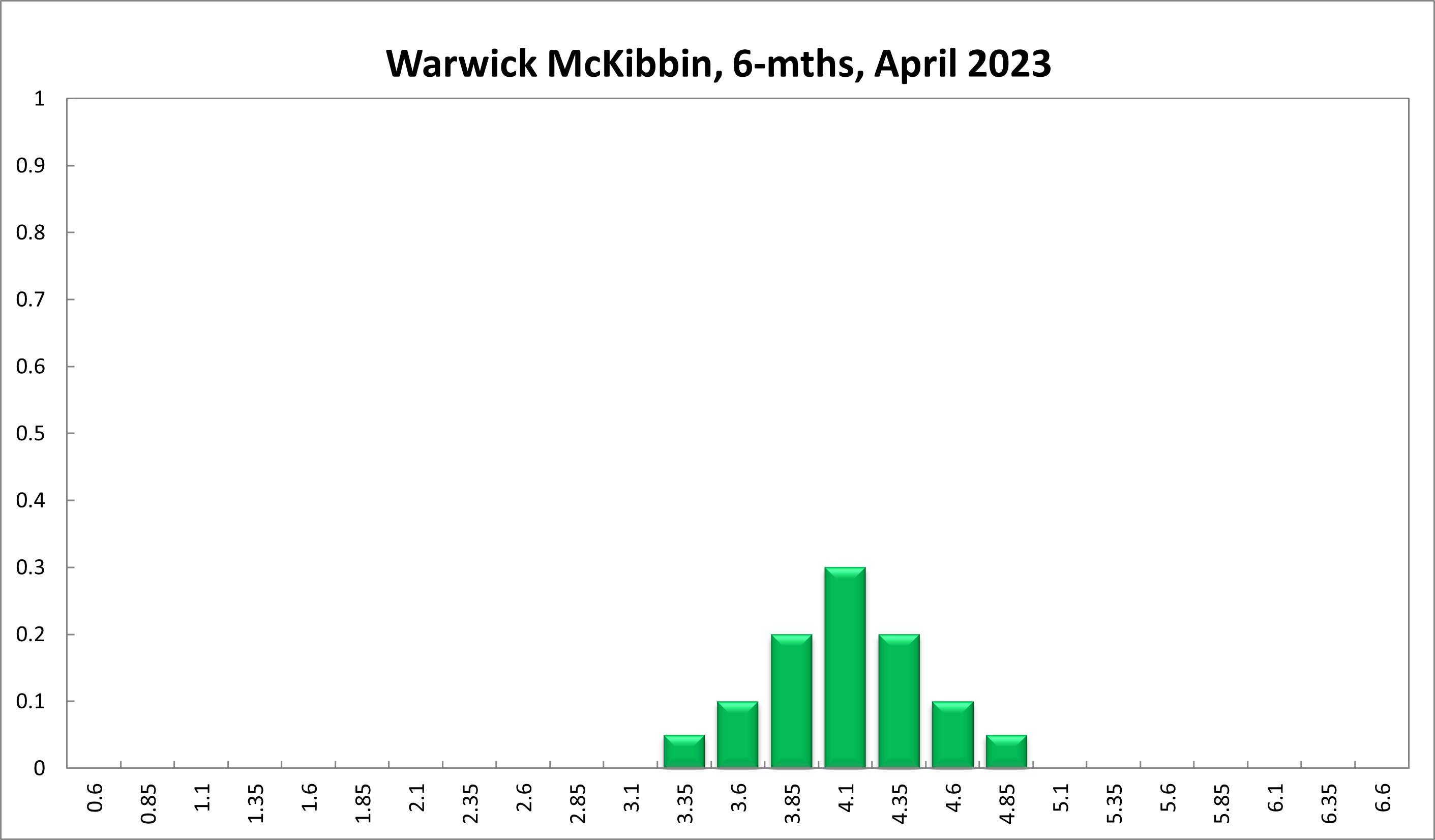

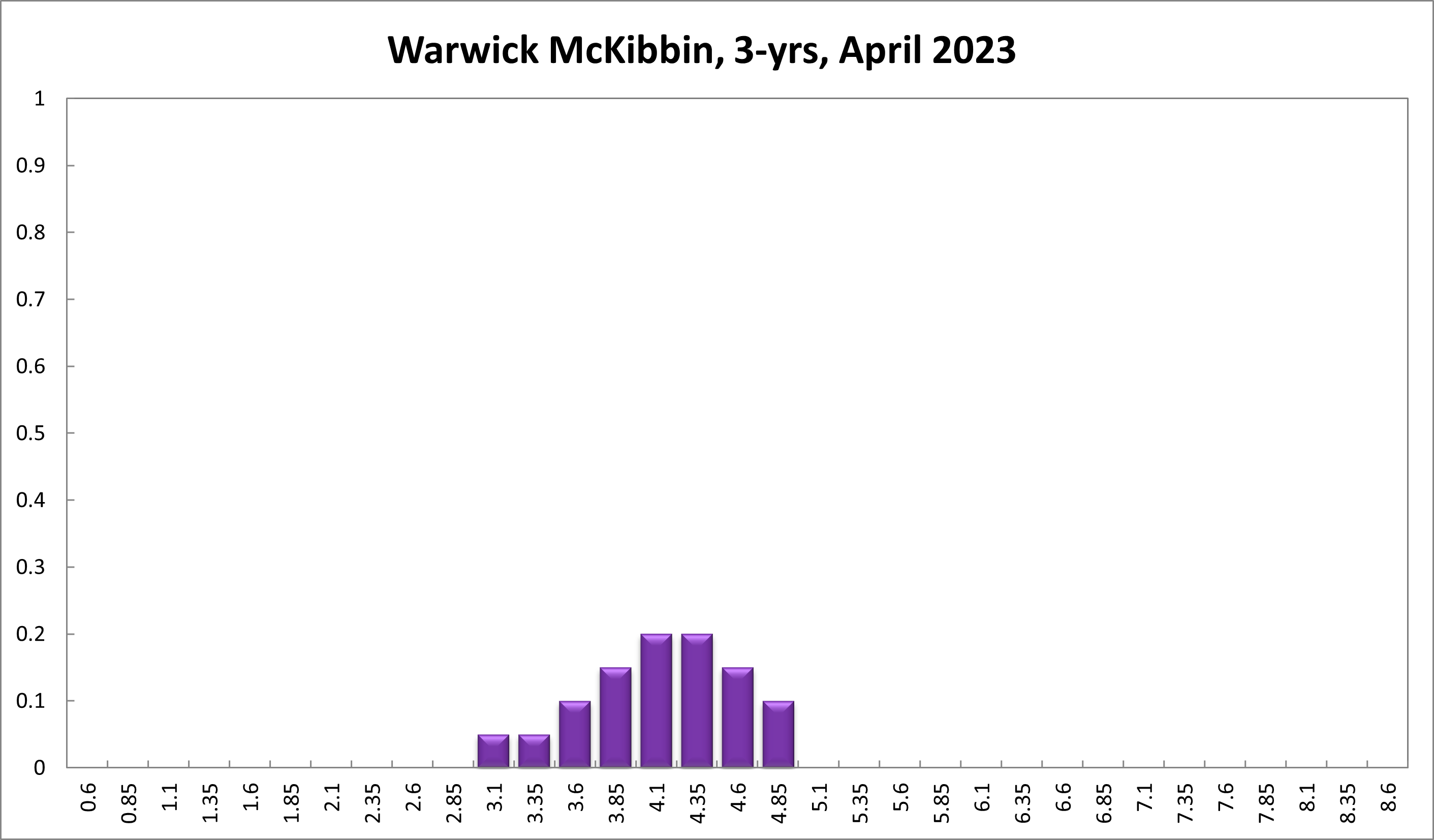

Warwick McKibbin

With CPI inflation running at 7.8% annually and 6.8% in February, and the policy rate at 3.6% real interest rates are significantly negative. The nominal policy rate is also well below the most recent growth in nominal GDP at 2.1% (8.4% annualized) in the December quarter and 12% of the year to December. Monetary policy will need to be more contractionary if inflation is to fall back into the target band of 2-3%. Higher interest rates are not only needed to slow consumption but also to offset the weaker $A which feeds further into imported goods inflation. While major central banks are raising interest rates the inflationary impulse from overseas will be felt in Australia through higher import prices exacerbated by a weaker $A. The more slowly the RBA responds the more likely that other input costs such as wages will also respond to the inflationary impulse making the work of monetary policy that much harder over the medium term. Concerns about possible financial stability can be dealt with using other instruments of financial stability policy and income distribution issues should be dealt with by fiscal policy. Neither of these issues should deter the RBA from its main goal of returning inflation to target.

Updated: 5 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin