James Morley

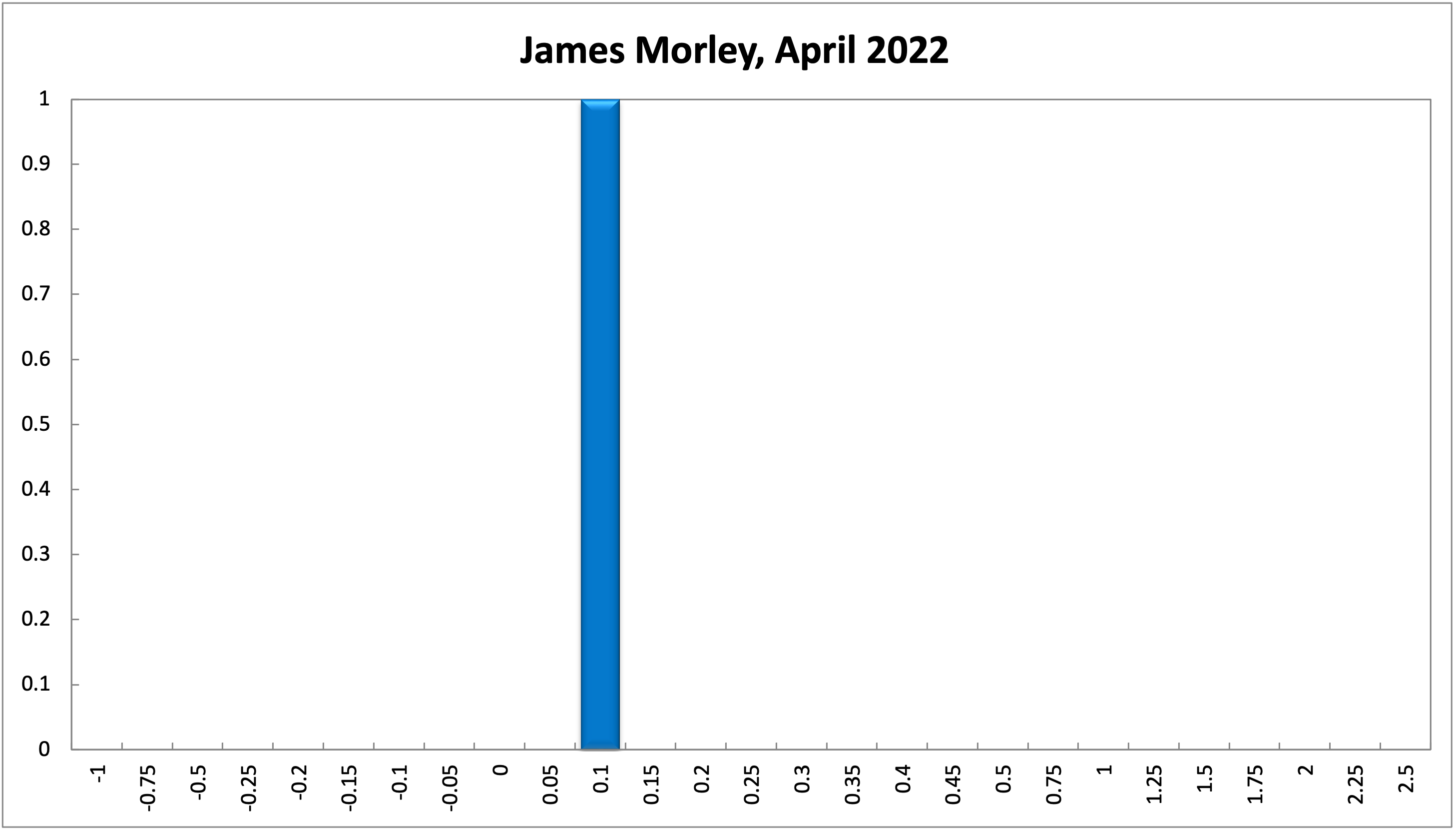

The just-released federal budget maintains a substantial deficit, despite higher than expected revenues due to commodity prices and an unemployment at 4%. Given relatively little slack in the economy, the main effects of the budget deficit will be higher inflation (headline and underlying) rather than to stimulate real activity. This provides a change in circumstances such that the RBA should consider beginning its raising cycle earlier than previously planned. It is true the RBA is still likely to wait for some indication of stronger nominal wage growth to pull the trigger. But that is almost certainly coming and will also imply higher real wage growth in 2023 and beyond given some easing of oil price and global supply chain effects on headline inflation later this year.

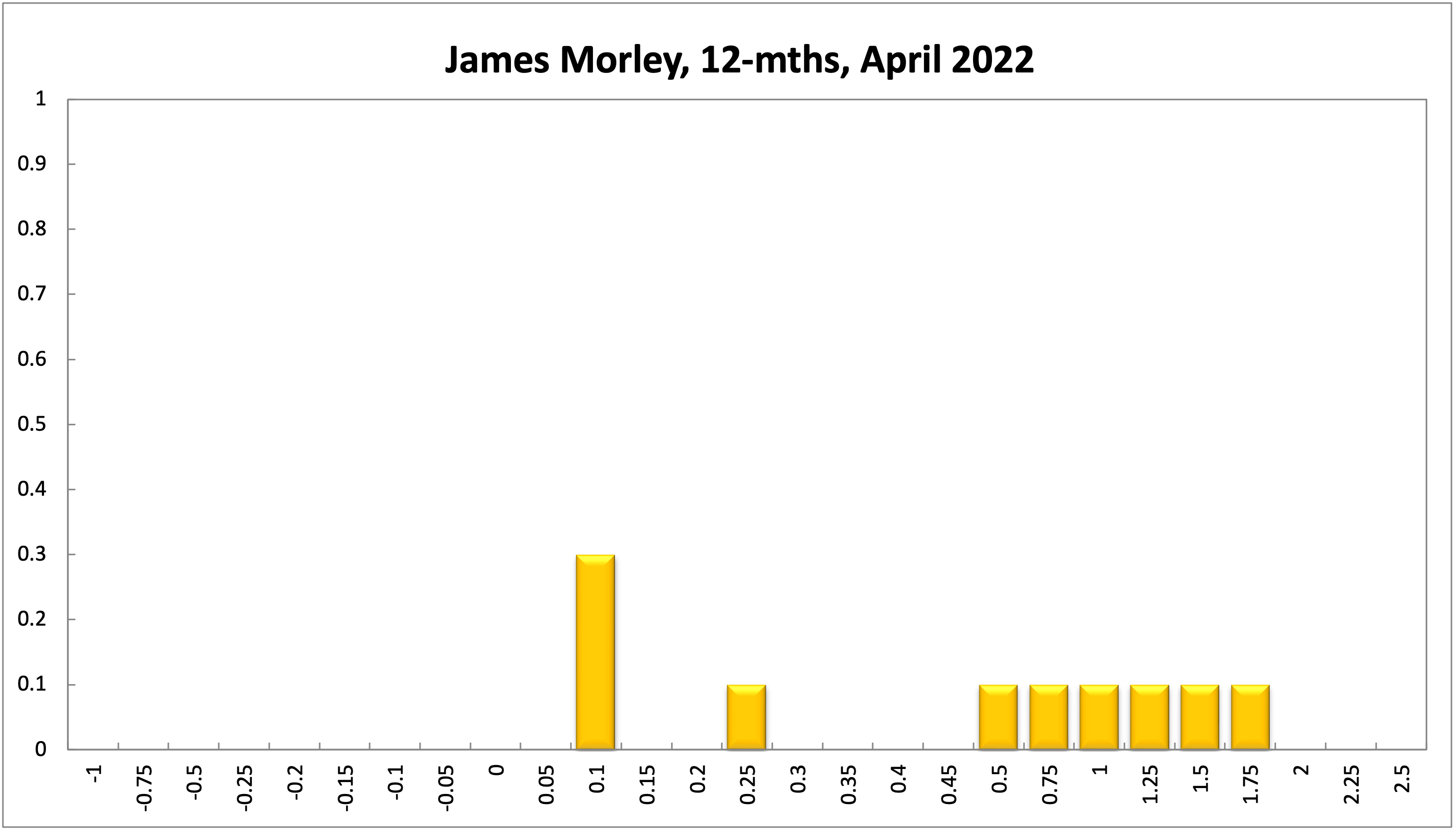

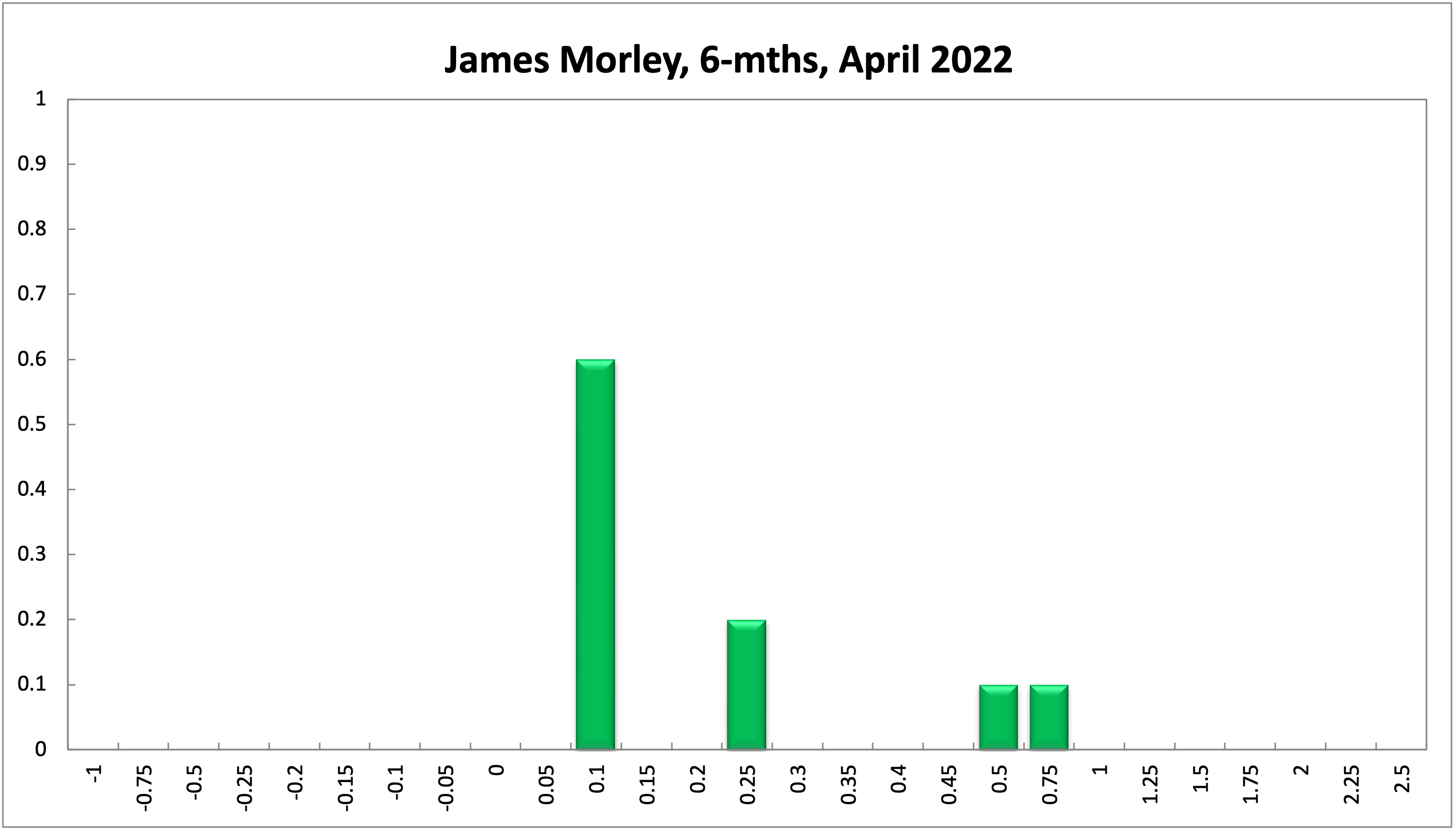

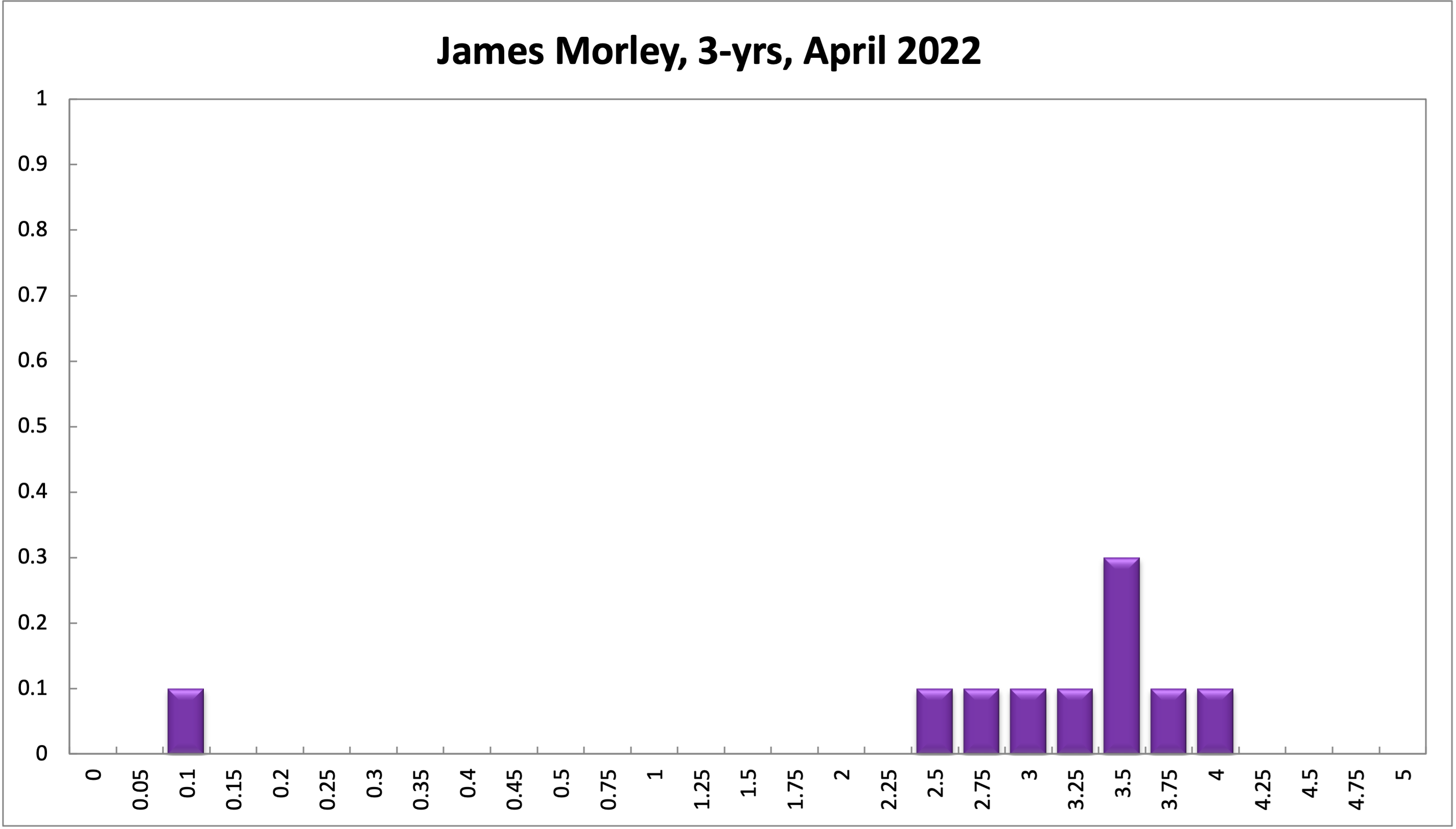

A change in government in May could mean a revised budget. But it is unlikely it would be particularly more fiscally responsible in the short term. So there is now a nontrivial chance that the RBA could and should start raising rates within the next six months, although I would still put this at below 50/50 odds given the need for wage growth to really pick up, while wages are generally slower to adjust in Australia than, say, the US given the different structure of the labour market.

However, the profligate budget does mean that liftoff will almost surely happen sooner than previously expected and likely in late 2022 or early 2023.

Updated: 18 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin