Aggregate

RBA Shadow Board Continues to Favour Holding Overnight Rate Steady

The latest reading on Australia’s inflation rate (based on the quarterly consumer price index) is from June, at 3.8% year-on-year, with the trimmed mean measure of core inflation 3.9% year-on-year. Both are still well above the Reserve Bank of Australia’s official target range of 2-3%. The labour market, despite its remarkable resilience, is finally showing signs of weakening. Asset prices continue to perform, with Australian shares posting record gains, against a backdrop of global geopolitical tensions. Once again, the Shadow Board recommends holding the overnight rate steady at 4.35%, attaching a 52% probability that this is the optimal policy setting.

The seasonally adjusted unemployment rate held steady in August, at 4.2%, even though total employment increased by 47,500. The labour force participation rate, at 67.1%, is the highest it has ever been. The underemployment rate ticked up from 6.3% to 6.5%, and total monthly hours worked in all jobs grew by 0.4% in seasonally adjusted terms. Australian job advertisements contracted by 2.1% in August, month-over-month, constituting the seventh consecutive decline in job ads and confirming the impression that the labour market is weakening. Q2 wages growth, released one week ago, came in at 4.1%, slightly above the CPI inflation rate, implying that real wages are finally making up some lost ground. The consensus forecast is that wages growth will slow to 3.8% year-on-year in Q3 of 2024.

The Australian dollar, after falling 3 US¢ in July, has rebounded and passed the 68 US¢ mark at close of trading (20 September). The yield on Australian 10-year government bonds extended its decline: as of 22 September 2024, it stands at 3.93%. The short-term yield curve (2y vs 1y) remains inverted, with a reduced spread of -22 bps; the medium-term yield curve (5y vs 2y) has flattened again, with a narrow spread of 0.5bps. The long-term yield curve (10y vs 2y) is displaying “normal convexity”, with a spread of 34.7bps. The bull run in the Australian stock market continues unabated; the S&P/ASX 200 Index is currently trading at an all-time high, above 8,200.

Consumer confidence, as measured by the Westpac-Melbourne Institute Consumer Sentiment Index, currently near the 85 mark, remains firmly below the neutral value of 100. Month-on-month retail sales stayed flat in July and grew by only 2.3% year-on-year. The NAB business confidence index turned negative again, from +1 to -4 (August reading), the lowest reading for this calendar year. The Judo Bank Manufacturing and Services PMIs both softened in September, the former now well below the neutral level of 50. Capacity utilisation weakened in July, from 83.5% to 82.7%, but still above the long-term average of 81.3%. Worryingly, the six-month annualized growth rate in the Westpac-Melbourne Institute Leading Economic Index, which predicts economic activity relative to trend three to nine months ahead, turned well south, coming in at -0.27 in August from 0.04 in July. Overall, consumer and business sentiment indicators point to a softening of the Australian economy, helping to reduce inflationary pressures.

Concerns about the global economy are mounting as geopolitical tensions in the Middle East are intensifying and the global trading system is fracturing. In a speech at the International Monetary Fund in Washington D.C., ECB President Christine Lagarde warned that the global economy is facing rifts comparable to the pressures that resulted in “economic nationalism” in the 1920s. The past four years, what with the pandemic-related global supply chain disruptions, Russia’s invasion of Ukraine and the consequent rise in energy and food prices, posed an “extreme stress test”, according to the ECB head. She did mention it was remarkable that central banks have been able to bring inflation under control within two years, without a large increase in unemployment, but warned against complacency and the need to better manage uncertainty. As a small, open economy, these challenges directly affect Australia.

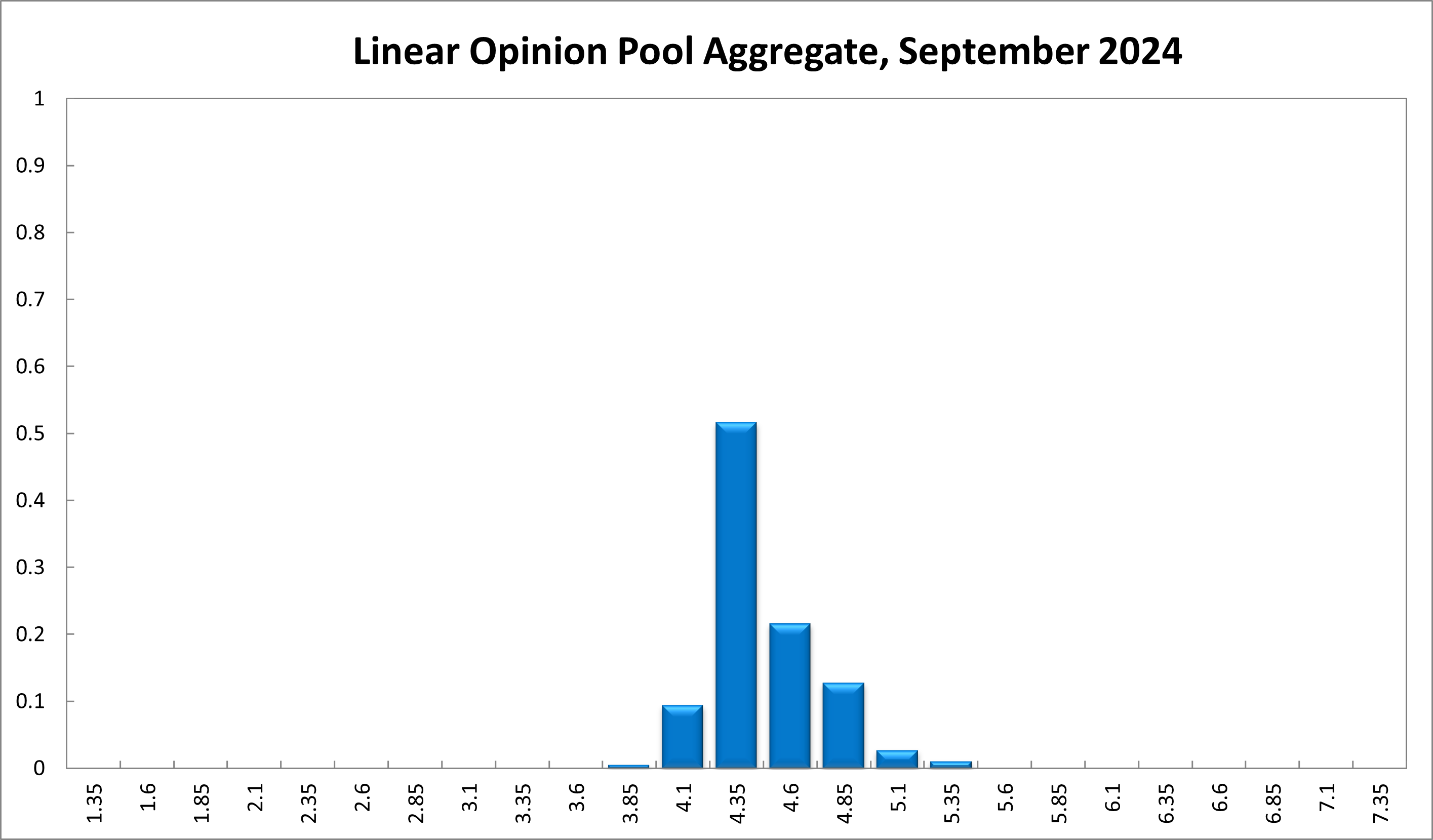

The Shadow Board’s conviction of keeping the overnight rate, currently equal to 4.35%, on hold has strengthened mildly. The Board attaches a 52% probability that this is the appropriate setting (up from 48%), a 38% probability (down from 42%) that the overnight right should increase, to 4.6% or higher, and an unchanged 10% probability that the overnight right should decrease to 4.1%.

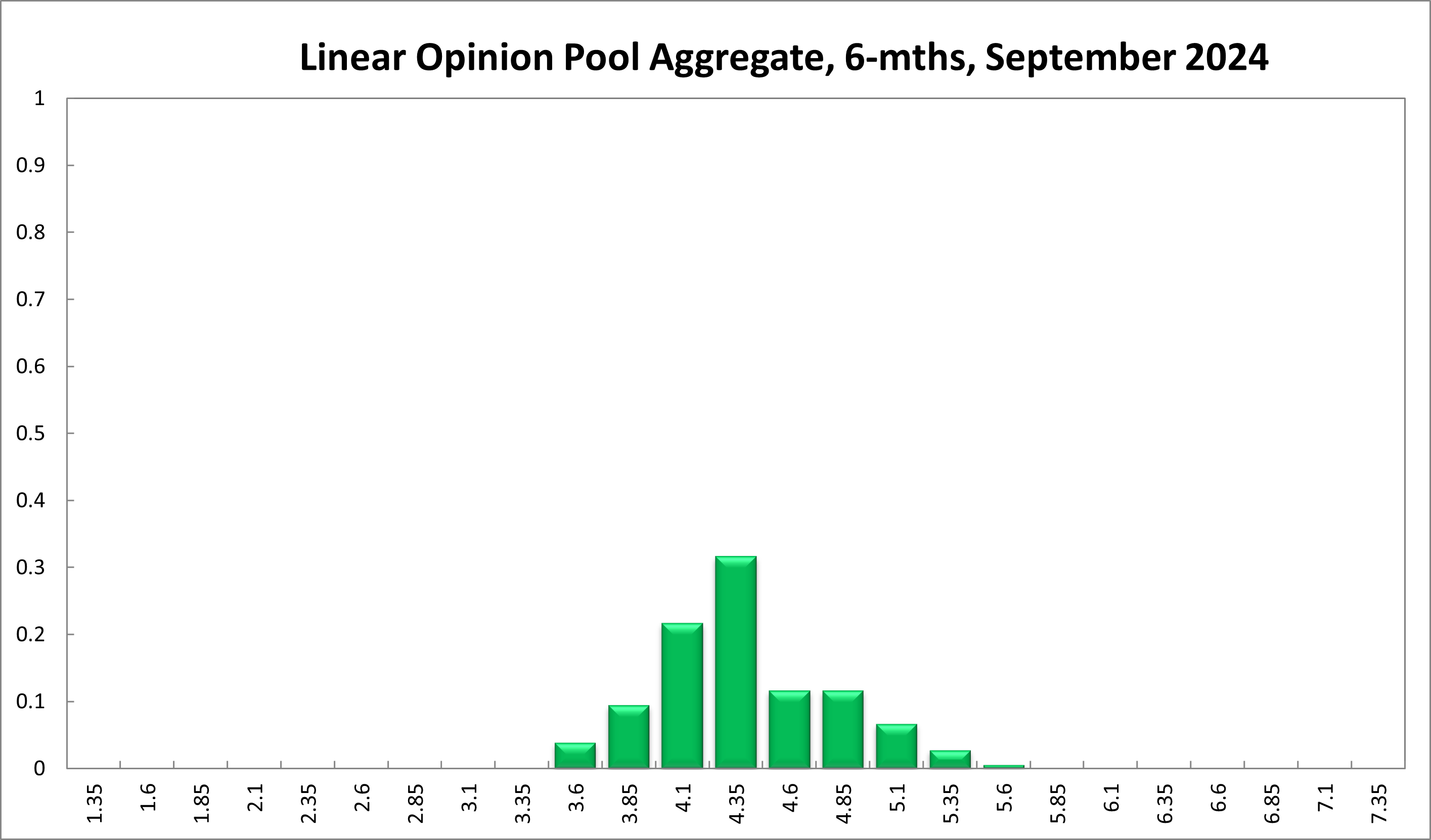

This strengthened conviction carries over to longer horizons: 6 months out, the confidence that the cash rate should remain at the current setting of 4.35% equals 32% (up five percentage points); the probability attached to the appropriateness of an interest rate decrease equals 35% (up two percentage points), while the probability attached to a required increase has shrunk from 40% to 33%.

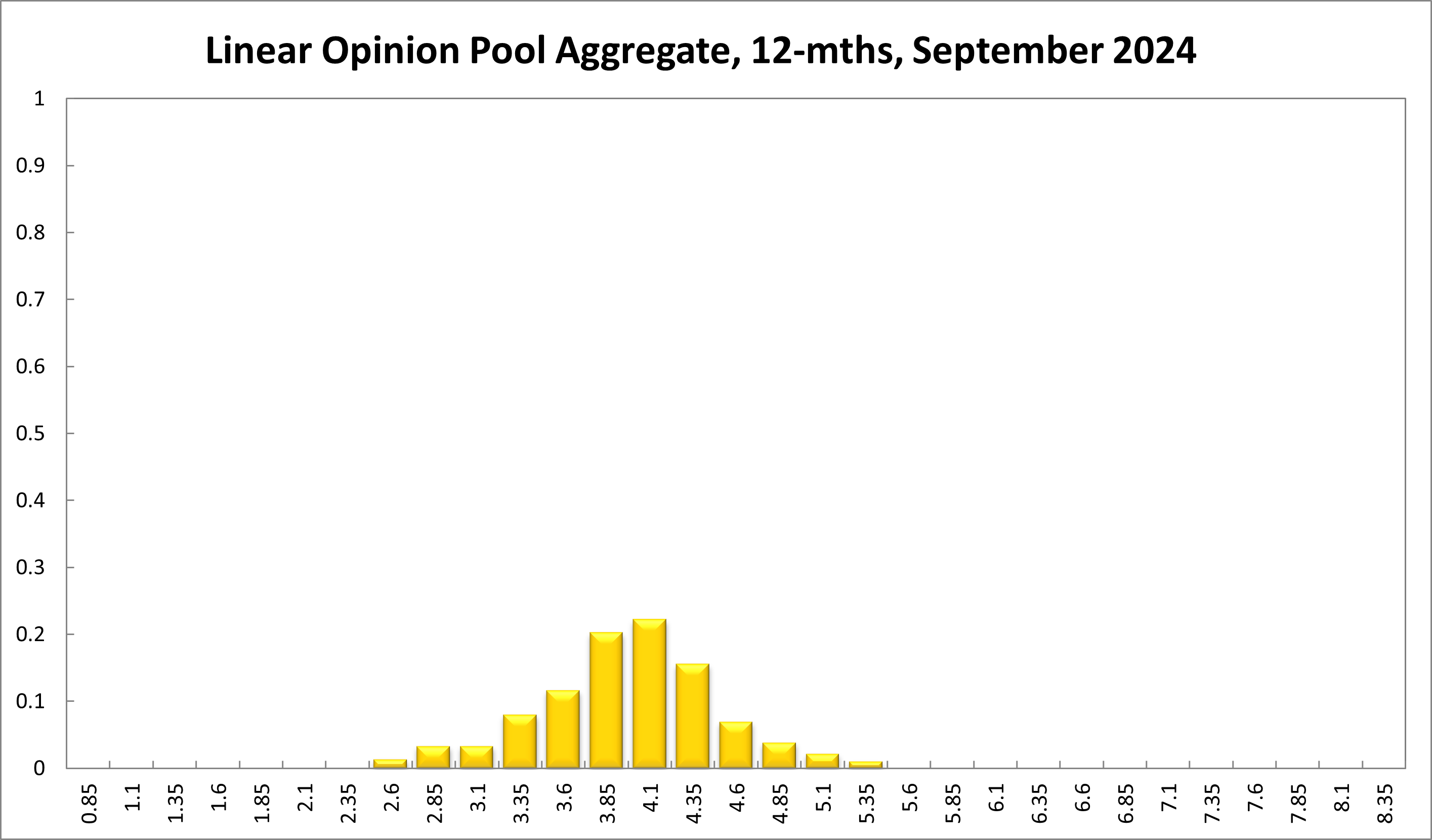

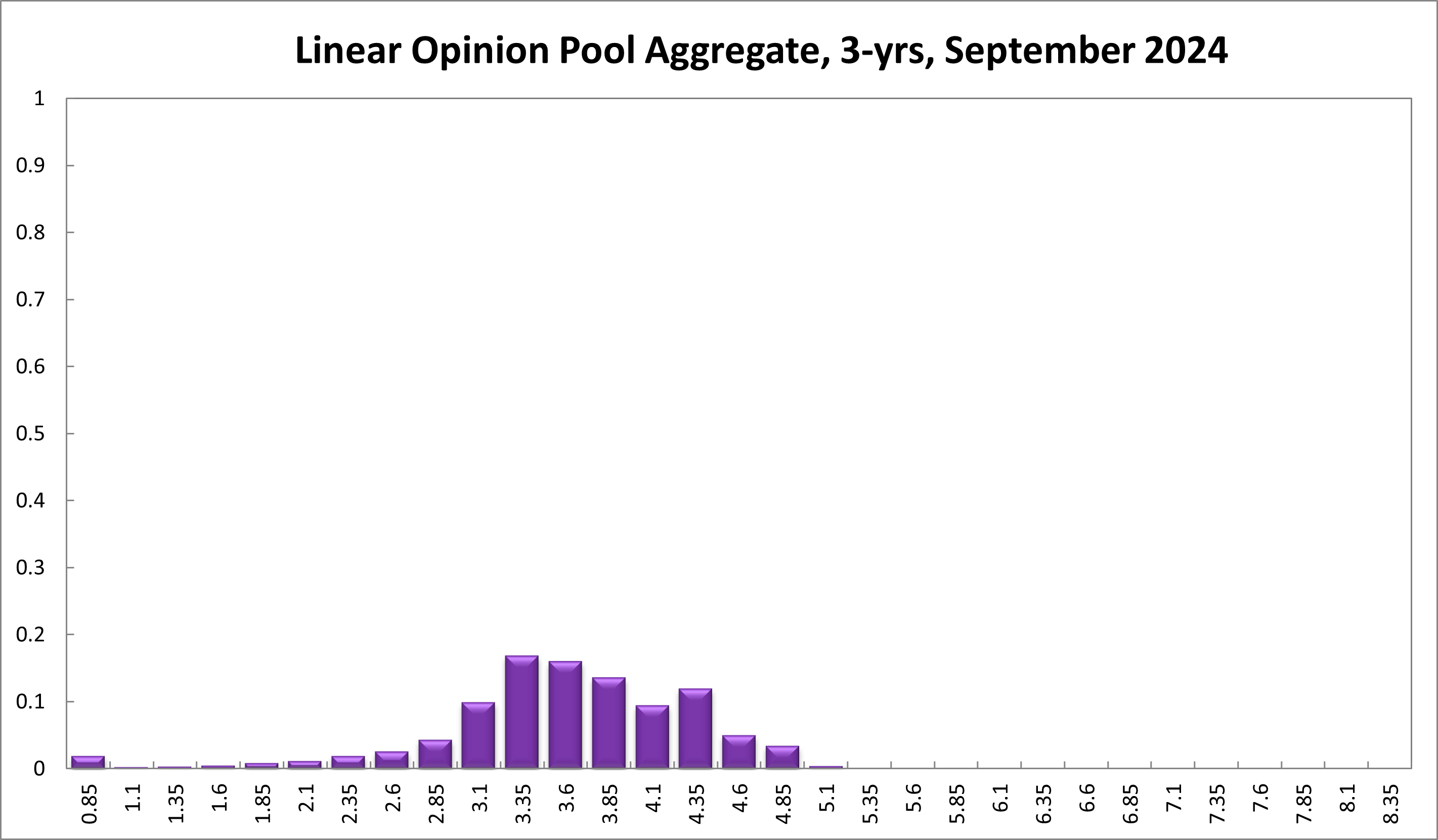

One year out, the Board’s recommendation is to tilt towards monetary easing: members’ confidence that the appropriate cash rate should remain at the current level of 4.35%, equals 16% (down from 18%), while the confidence in a required cash rate decrease, to below 4.35%, equals 70% (up from 59%), and its confidence in a required cash rate increase, to above 4.35%, is 14% (down from 23%). Three years out, the Shadow Board attaches a 12% probability that 4.35% is the appropriate setting for the overnight rate (previously 11%), a 79% probability that a lower overnight rate is optimal (81%) and a 9% probability that a rate higher than 4.35% is optimal (7%).

The ranges of the probability distributions have only changed a little and are as follows: they extend from 3.85% to 5.35% for the current recommendation, from 3.60% to 5.60% for the 6-month horizon, from 2.60% to 5.35% for the 12-month horizon, and from 0.85%-5.10% for the 3-year horizon.

Updated: 16 October 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin