Outcome

The annual inflation rate in Australia went down to 4.1% in Q4 of 2023, well below the 5.4 % in Q3 and below the RBA forecast of 4.5 % (according to the November 2023 Statement on Monetary Policy). The CPI increased this quarter by a mere 0.6 %, lowest since March 2021. The inflation rate (4.1 %) is now below the cash rate (4.35 %). Measures of expectations of inflation indicate that expectations are well anchored. The unemployment rate remains at 3.8 %. While non-tradeable inflation remains high, it seems that we are on target to achieve a soft landing and at an earlier date than forecasted.

Around the world, inflation has eased. The debate now has turned to when central banks will start to cut rates and by how much. Traders in the federal funds futures market are betting that the US Federal reserve will cut the rate in March and investors are expecting the first ECB rate cut in April. Nevertheless, there are many geopolitical uncertainties.

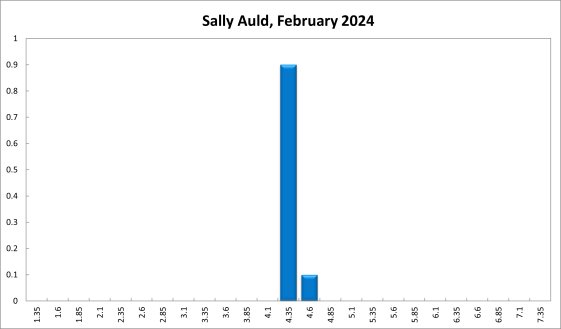

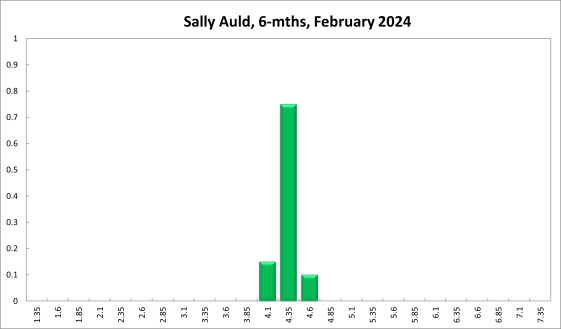

The cash rate in Australia is below many other central banks. However, research indicates that the prevalence of variable mortgage rates increases and speeds up the transmission mechanism of monetary policy. Given this, the current inflation trends and the restrictive monetary stand, my view is that the Reserve Bank of Australia should keep the cash rate on hold in the next meeting. My view is also that a cut rate may be desirable in a few months, but not just yet.

I support a faster and more certain return to the inflation target, now explicitly stated to be 2.5%, than most other commentators.

The longer inflation is allowed to remain above target, the more likely it is that inflation expectations increase. If that happens, then a substantial increase in unemployment would be required.

An increase in interest rates now would mean higher unemployment in the short run, but lower and more stable unemployment in the long run.

Updated: 19 September 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Overnight Rate Should Remain at 4.35% According to RBA Shadow Board

Australia’s quarterly inflation rate dropped by more than a percentage point, from 5.4% year-on-year in Q3 to 4.1% in Q4, below market expectations of 4.3%. Inflation moderated in most sectors, including food, housing, health, transport, and education. The RBA’s Trimmed Mean CPI, an inflation measure that leaves out items experiencing the most extreme changes, increased by 4.2% year-on-year, down from 5.2%, but still above the RBA’s target band of 2-3%. The unemployment rate rose slightly, consumer confidence appears to have bottomed out, and business confidence is painting a mixed picture, much like the global outlook. In this round, the Shadow Board is strongly in favour of holding the overnight rate steady at 4.35%, attaching a 61% probability that this is the optimal policy setting, while only attaching a 7% probability that a rate cut, to below 4.1%, is the appropriate policy.

The monetary tightening is making itself felt in the Australian labour market. The official seasonally adjusted unemployment rate increased in December 2023, though, at 3.9%, it remains historically low. A closer look at some other labour market statistics reveals growing weakness: full-time employment fell by more than 105,000 (the increase in part-time employment was only able to compensate for less than half of that) and the labour force participation rate dropped half a percentage point, from 67.3% to 66.8%. Job advertisements were basically flat, as was the underemployment rate, at 6.5%. Job vacancies fell slightly, to 389,000. Overall, though the labour market is weakening, it is doing so gradually and proving surprisingly resilient. Australia’s seasonally adjusted wage price index for Q4 of 2023 will be released on 21 February and should give further insight into the labour market’s tightness. The mean forecast is for a reading of 4.2% year-on-year, following a 4% increase in Q3.

After climbing a couple of cents in December, the Australian dollar weakened again, finding some support at the 65 US¢ mark on the Friday of the past week (2 February). The drop in the Australian dollar reflects market’s belief that interest rates have likely reached their maximum, following the recent inflation numbers. Yields on Australian 10-year government bonds continued their decline from the recent peak, to under 4.1%. The yield curve in short-term maturities (2y vs 1yr) remains inverted, with a considerable spread of -29.8 bps; the one in medium-term vs short-term maturities (5y vs 2y) also remains inverted since the last interest rate round, with a smaller spread of -7.4 bps. The yield curve in long-term vs short-term maturities (10y vs 2y), having a spread of 31 bps, is displaying normal convexity. Australian shares, on the other hand, have continued their bull run, much like the rest of the industrialised world, posting new all-time highs: the S&P/ASX 200 stock index managed to breach 7,700 and is expected to climb higher.

Consumer confidence in January, as measured by the Westpac-Melbourne Institute Consumer Sentiment Index, fell slightly, from 82.1 to 81, close to the average for the past 6 months. Retail sales declined by 2.7% month-over-month in December 2023, considerably worse than forecast, albeit after an unusually large increase of 1.6% in the previous month. Consumer credit posted a new high in December 2023, on the back of a further decline of the household saving rate, which declined from a peak of 19.2% in Q3 of 2021 to 1.1% in Q3 of 2023.

The NAB business confidence index improved to -1 in December 2023 from a downwardly revised -8 in November. The Judo Bank Composite PMI, the Services PMI and the Manufacturing PMI, likewise, improved, the latter jumping from 47.6 to 50.1, the highest reading in a year. The capacity utilisation rate, on the other hand, extended its 4-month decline, from 83.59% in November 2023 to 82.74% in December. The Composite Leading Indicator appears to have bottomed out in 2023 and gradually meliorating, whereas the Ai Group Industry Index contracted for the 19th consecutive month, showing worsening conditions in activity/sales, new orders, and input volumes. These indicators are giving mixed signals, with some sectors holding up and others suffering contractionary conditions.

The global economy remains a major source of uncertainty, with considerable downside risk. The World Economic Forum’s Chief Economists Outlook for January 2024 predicts a mild global downturn for this year. There is some optimism, fuelled by a surprisingly strong US economy and a significant drop in global inflation, but geopolitical factors in particular threaten to impede cross-border trade, increase energy prices and rattle financial markets. And the liquidation of Evergrande, one of China’s biggest property developers, could have significant knock-on effects for the Chinese economy. The International Monetary Fund in Washington is downplaying these risks and actually upgraded its outlook for the global economy and all major economies, Germany excepted.

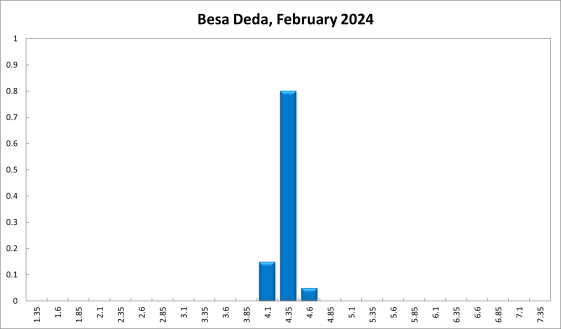

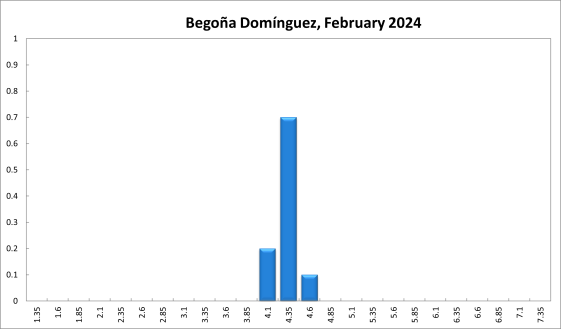

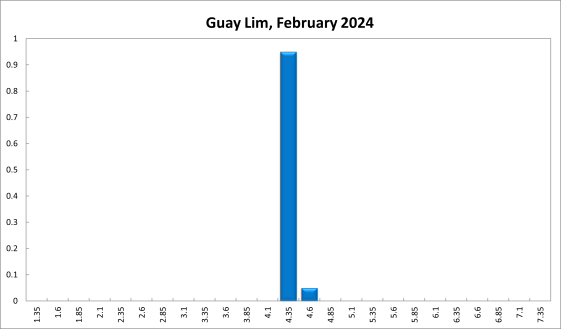

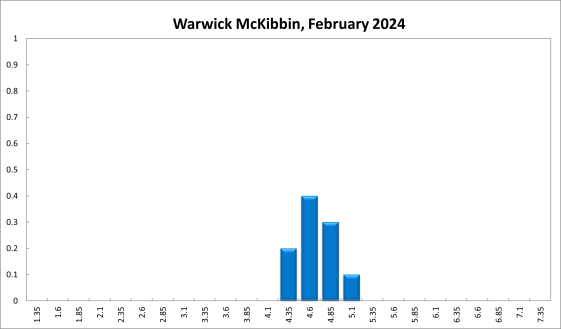

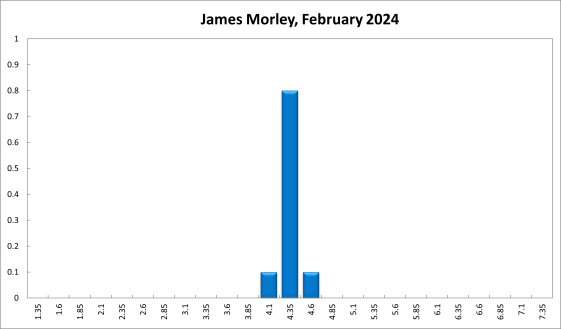

The Shadow Board’s current view of monetary policy is firmly in favour of holding steady: it attaches a 61% probability that keeping the overnight rate, currently equal to 4.35%, on hold is the appropriate policy, while attaching a 32% probability that the overnight right should increase, to 4.6% or higher, and a 7% probability that the overnight right should decrease to 4.1%.

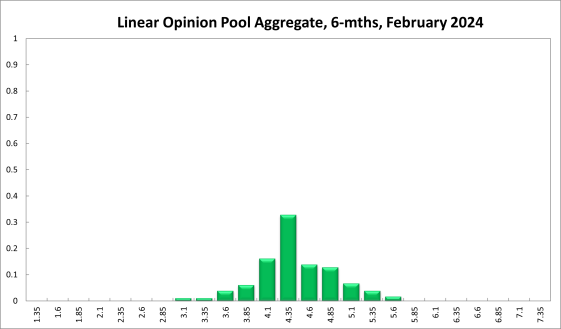

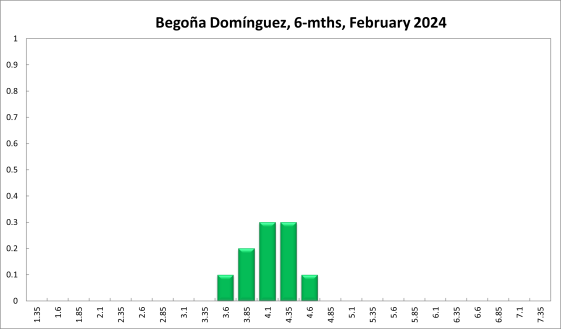

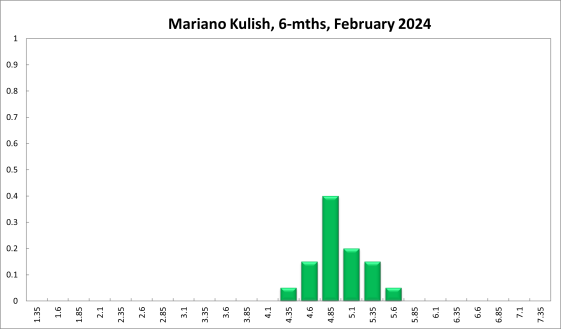

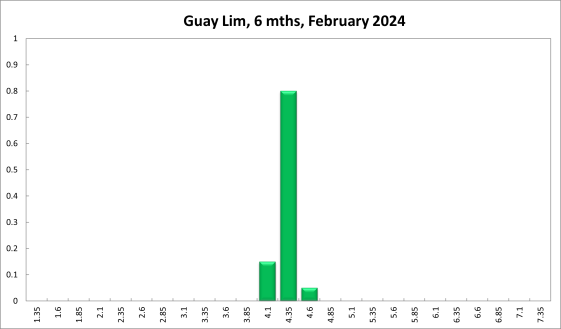

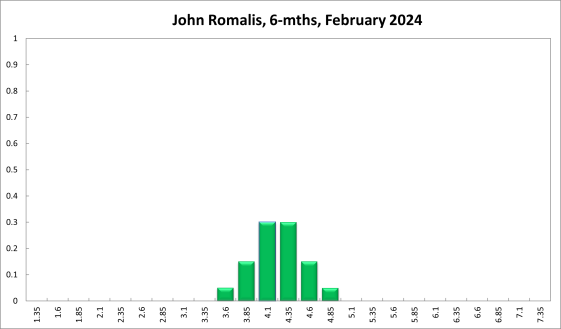

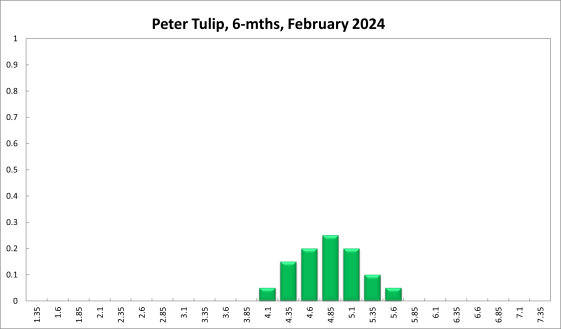

The probabilities at longer horizons have become slightly less restrictive: 6 months out, the confidence that the cash rate should remain at the current setting of 4.35% equals 33%; the probability attached to the appropriateness of an interest rate decrease equals 28%, while the probability attached to a required increase equals 39%. The mode recommendation at this horizon is 4.35%.

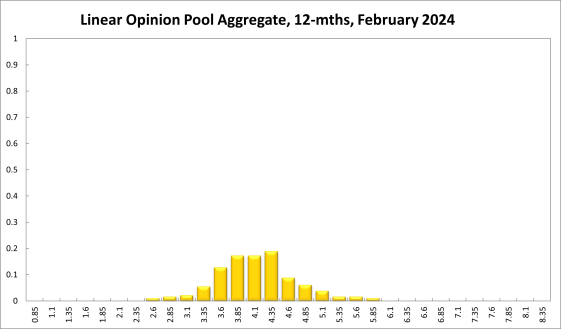

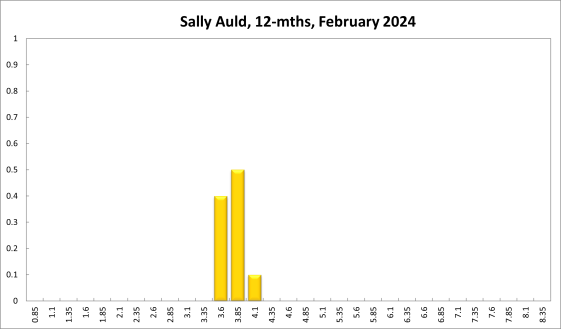

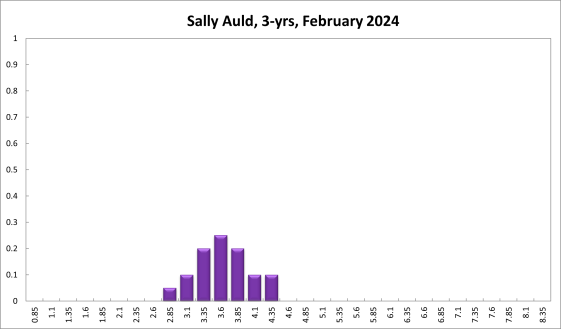

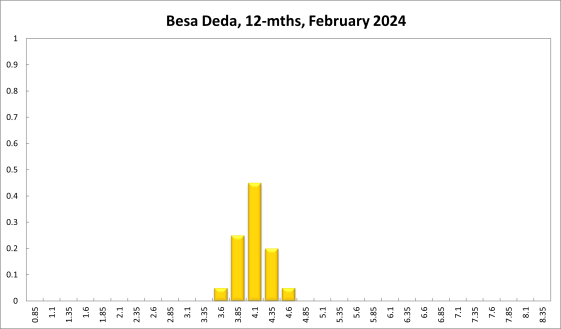

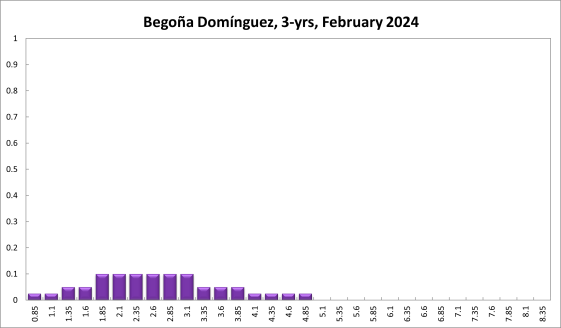

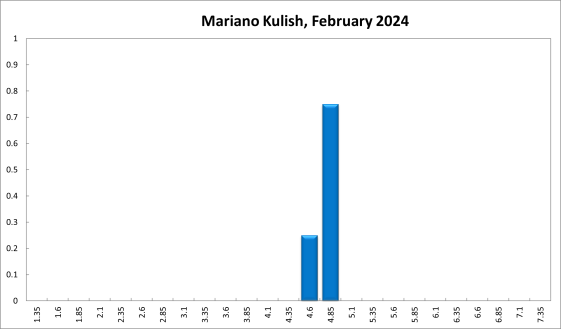

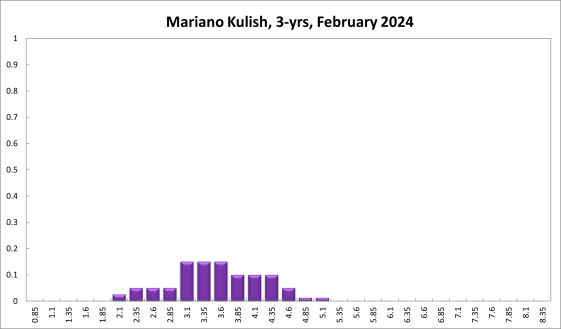

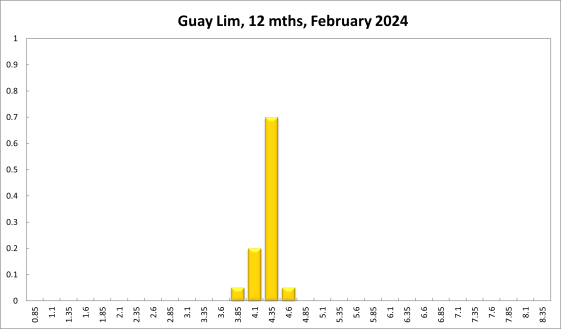

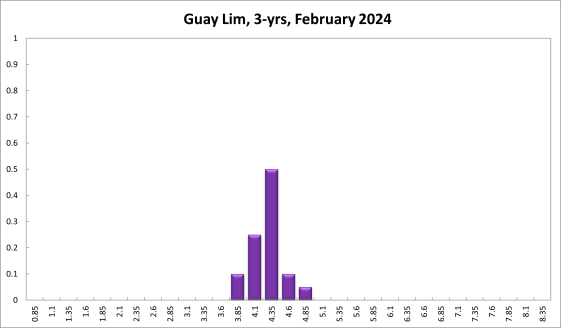

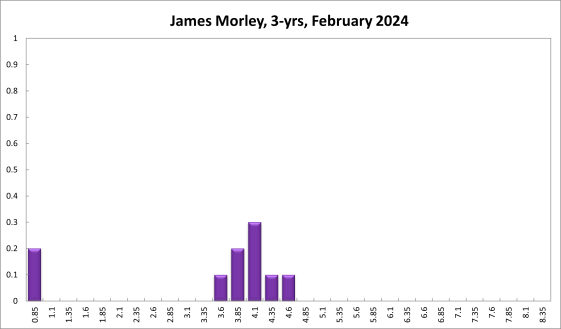

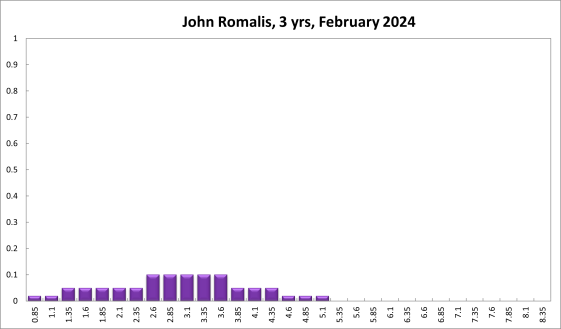

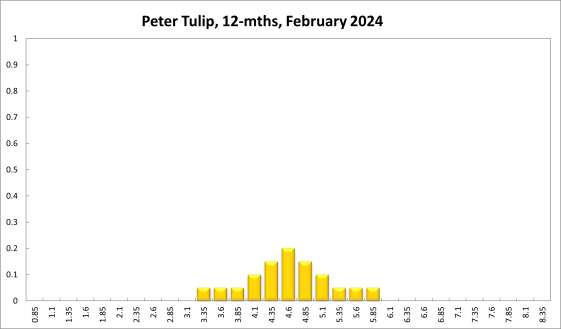

One year out, the Shadow Board members’ confidence that the appropriate cash rate should remain at the current level of 4.35%, equals 19%. The confidence in a required cash rate decrease, to below 4.35% equals 58%, and its confidence in a required cash rate increase, to above 4.35%, is a 23%. Three years out, the Shadow Board attaches an 14% probability that the overnight rate should equal 4.35%, a 77% probability that a lower overnight rate is optimal and a 9% probability that a rate higher than 4.35% is optimal.

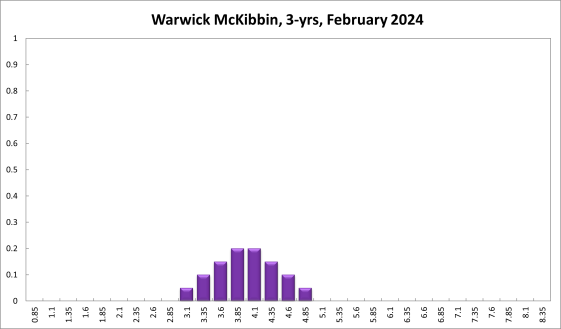

The range of the probability distribution for the current recommendation is unchanged, extending from 4.10% to 5.10%. For the 6-month horizon the range, extending from 3.10% to 5.60%, shrunk by 25 bps. The range for the 12-month horizon narrowed by 75 bps, now extending from 2.60%-5.85%, while the range of the 3-year horizon marginally narrowed to 0.85%-5.10%.