Outcome

Inflation has clearly peaked in 2023Q1. The RBA can let the effects of past hikes in rates play out to bring inflation down further.

Much of the public opposition to further rate increases seems to assume that current unemployment rates are sustainable. The ACTU and left-wing think tanks argue that tight labour and housing markets will not lead to accelerating wages, prices and rents.

That is contrary to what happened in 2008 and the 1970s and to overseas experience. It is possible that relationships have changed, but I am not aware of any modelling or other research indicating this is likely, just wishful thinking.

This opposition to policy tightening rests on a refusal to make difficult decisions or to accept unpleasant trade-offs.

Updated: 19 September 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Shadow Board Marginally Favours a Stay on Rate Increase

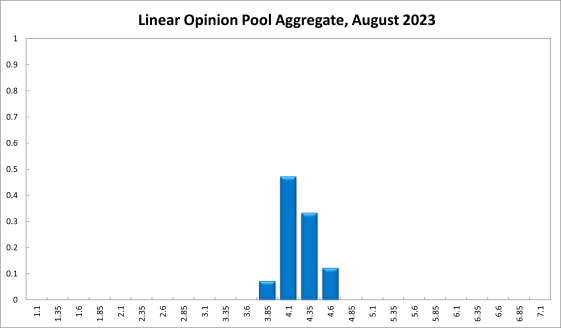

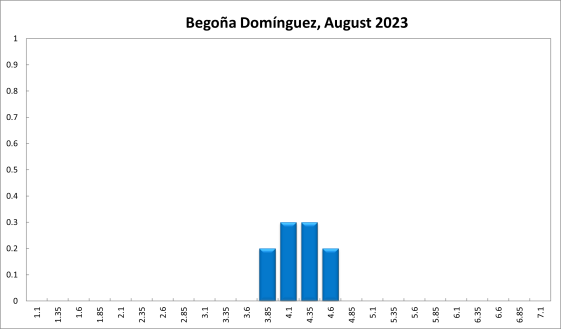

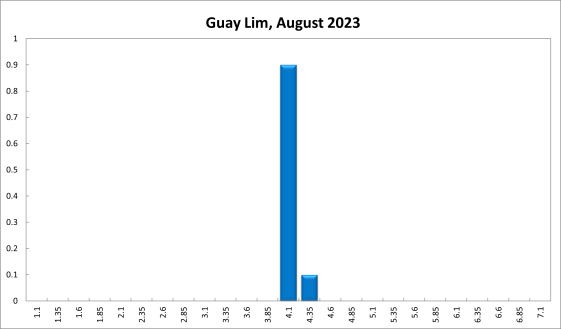

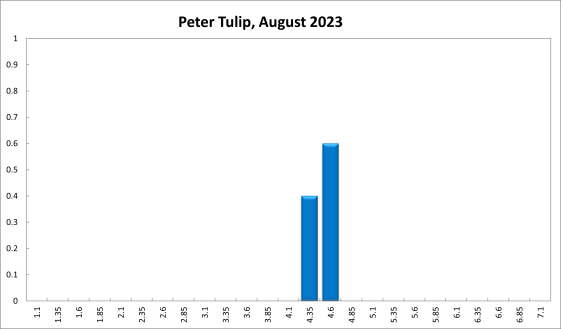

Recent inflation data continues to show positive signs overall. Australia’s quarterly measure of annual consumer price index (CPI) inflation slowed from 7% to 6% in the June quarter of this year. The biggest contributors to rising prices were rents (+2.5%), international travel and accommodation (+6.2%) and “other financial services” (+2.5%). New dwelling purchase prices by owner-occupiers have also increased. The monthly CPI inflation rate also slowed, from 5.6% in the twelve months to May, to 5.4% in June, bringing the inflation rate closer to the RBA’s target band of 2-3%. The official, seasonally adjusted unemployment rate was unchanged at 3.5%. The RBA Shadow Board marginally considers another rate pause to be the appropriate policy. In particular, it attaches a 47% probability that the overnight rate should remain at the current level of 4.10%, a 46% probability that the overnight rate should be higher, and a 7% probability that overnight rate should be lower.

The official Australian seasonally adjusted unemployment rate was 3.5% in June, unchanged from a revised figure in May, though the labour force participation rate fell by 0.1 percentage points, off its all-time high. Job advertisements decreased by 2.5% month-over-month in June, continuing their steady decline from their recent all-time high. They remain nearly 50% above pre-pandemic levels. Job vacancies are also down slightly, compared to the previous month. Overall, the labour market remains remarkably resilient. The national minimum wage was raised by 8.5%, to $23.23 per hour. Official figures on wages growth are not due until mid-August; however, there are signs that wages growth is picking up slightly, albeit at a slower pace than CPI inflation. Thus, real wages are currently still falling, on average.

The behaviour of the Australian dollar in July replicated its movement in June – a rally to 69 US¢ by mid-month, followed by a decline below 67 US¢. Yields on Australian 10-year government bonds, following the RBA’s decision to keep the cash rate unchanged last month, dropped slightly, to below 4%. In short-term maturities and mid-term vs short-term maturities, yield curves are inverted, with spreads around 16 bps. The yield curve in long-term vs short-term maturities, however, is basically flat, suggesting that markets believe current rates are close to their peak. The Australian share market joined the global rally, posting some impressive gains: the S&P/ASX 200 stock index gained nearly 500 points from its recent low at the beginning of the month, finishing above 7,400 on 28 July.

The Melbourne Institute and Westpac Bank Consumer Sentiment Index, despite a 2.7% month-over-month improvement in July 2023, to 81.3, remains in “deeply pessimistic” territory. Retail sales in June contracted by 0.8% month-over-month, reversing expansion from the previous month. Business confidence was mixed, with the Judo Bank Australia Composite PMI and Services Sentiment indicator falling for the third consecutive month, from 50.1 to 48.3, and from 50.3 to 48, respectively, while the Manufacturing PMI rose slightly, from 48.2 to 49.6. The capacity utilisation rate continued its decline from historic highs, falling from 84.47% to 83.45% in June. The Composite Leading Indicator, which is designed to signal early turning points in business cycles, appears to be bottoming out, posting a slight increase after a near two-year decline. If the leading indicators continue to improve in the next couple of months, this may point to Australia’s economy experiencing a soft landing, rather than a sharp contraction.

A soft landing for the world economy is what the International Monetary Fund’s (IMF) is currently predicting: Pierre-Olivier Gourinchas, the IMF’s Economic Counsellor and Director of Research, recently argued that since the Covid-19 pandemic is officially over and supply-chain disruptions have returned to pre-pandemic levels, “the signs of progress are undeniable.” However, many challenges – including persistently high rates of core inflation and policy-induced geoeconomic fragmentation – “still cloud the horizon, and it is too early to celebrate.” Mr Gourinchas also pointed out the need for an acceleration of the climate transition. The OECD seems to be echoing these sentiments.

For the current (August) round, the Shadow Board’s position has shifted. Compared to last month, it now marginally favours holding the overnight rate steady: it attaches a 47% probability that this is the appropriate policy (compared to 39% in July), while only attaching a 46% probability to the need for another rate rise (56% in July). The probability attached to a required rate reduction equals 7%.

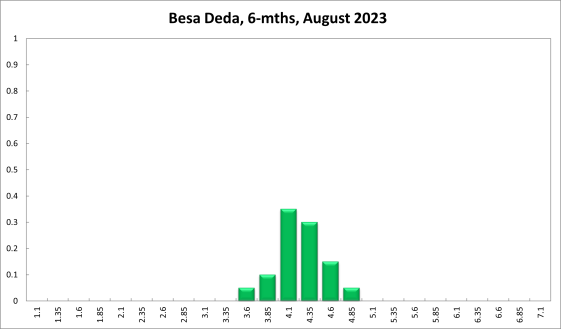

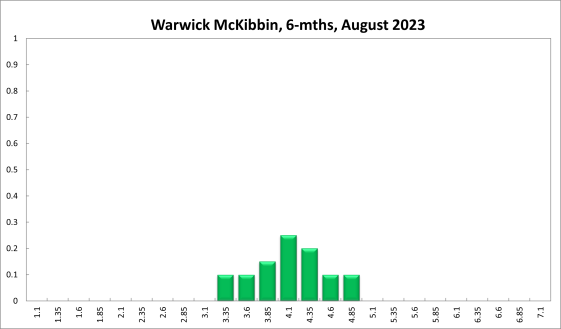

The probabilities at longer are as follows: 6 months out, the confidence that the cash rate should remain at the current setting of 4.10% strengthened from 15% to 26%; the probability attached to the appropriateness of an interest rate decrease equals 28% (compared to 26% in July), while the probability attached to a required increase equals 46% (down from 59%). The mode recommendation at this horizon is 3.35%, 50 bps lower than it was last month.

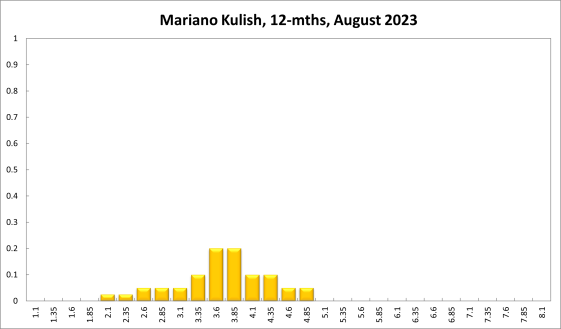

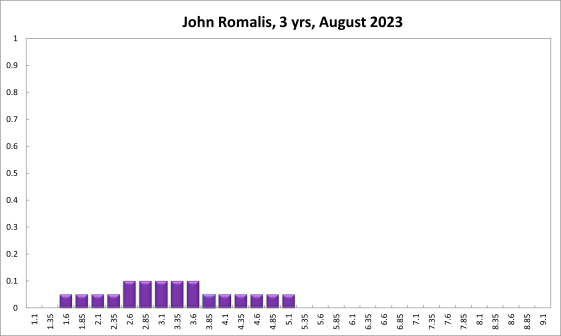

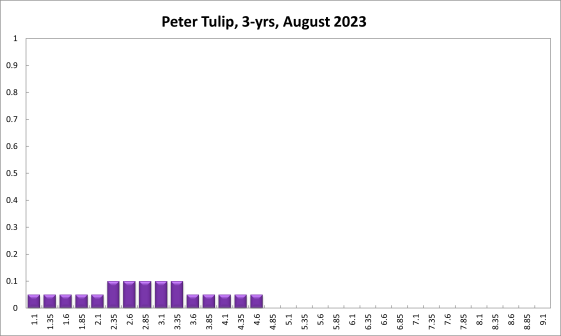

One year out, the Shadow Board members’ confidence that the appropriate cash rate should remain at the current level of 4.10%, equals 16% (compared to 14% in July). The confidence in a required cash rate decrease, to below 4.10% equals 44% (43% in July), and its confidence in a required cash rate increase, to above 4.10%, is 41% (43% in July). Three years out, the Shadow Board attaches a 10% probability that the overnight rate should equal 4.10%, a 72% probability that a lower overnight rate is optimal and a 18% probability that a rate higher than 4.10% is optimal.

The range of the probability distribution for the current recommendation narrowed by 50 bps, extending from 3.85% to 4.60% (compared to a range of 3.60% to 4.85% in the previous round). For the 6-month horizon it extends from 3.35% to 5.85% (unchanged). The range for the 12-month horizon, at 2.10%-6.10%, narrowed by 100bps, whereas the range of the 3-year horizon remains unchanged at 1.10%-5.1%.