Aggregate

After Last Month’s Pause, Shadow Board Recommends a 25bp Cash Rate Increase

Australia’s monthly consumer price index (CPI) rose 6.3% in the twelve months to March, down from 6.8% in February, a continued improvement but still above the RBA’s target band of 2-3%. The biggest contributor was once again housing (+9.5%), followed by food and non-alcoholic beverages (+8.1%), and furnishings, household equipment and services (+7.2%). The labour market remains surprisingly robust, and even consumer and business outlook appear to weather the interest rate storm. As in the previous month, the RBA Shadow Board believes a rate rise of 25 basis points, to 3.85%, is called for. In particular, it attaches a 66% probability that the overnight rate should be higher than the current level of 3.60%. It attaches a 34% probability that keeping the overnight rate on hold this round is the appropriate policy, signalling a degree of uncertainty about further tightening.

The official Australian seasonally adjusted unemployment rate in March was unchanged, at 3.5%, as was the labour force participation rate, at 66.6%. Total employment increased by 53,000 but the underemployment rate also rose, from 5.8% in February to 6.2% in March. Also in seasonally adjusted terms, total monthly hours worked in all jobs were nearly constant. The next update on the wage price index will be in mid-May, which will provide valuable information about the extent to which inflation is feeding wage pressure.

The Australian dollar continued to be range-bound, ending the month a little over 66 US¢. Yields on Australian 10-year government bonds stabilised below 3.3%, which is below the current cash rate. The spread between 2-year and 10-year bonds is roughly unchanged. The slopes of the yield curves fell slightly in absolute terms: at medium-term and longer term maturities, the yield curve is flat, at short-term maturities it remains inverted. Australian shares rallied somewhat, with the S&P/ASX 200 stock index closing the month of April above 7,300.

The Melbourne Institute and Westpac Bank Consumer Sentiment Index rose by more than 9% month-over-month in April 2023 to its highest reading for nearly a year. NAB’s index of business confidence, after a 10-point drop in February, climbed three points to -1 in March. The Composite Leading indicator held steady at 98.5 points, the lowest reading in more than two-and-a-half years, whereas the Westpac-Melbourne Institute Leading Economic Index, a leading indicator of economic activity, was practically flat for the month. The Judo Bank Australia Composite PMI dropped to 48.1 in April, down 1 point, and the Services PMI jumped four points to 52.6; however, both numbers are subject to revision. The capacity utilisation rate also dropped by one tenth of a percentage point, to 85.07%. It is notoriously difficult to paint a clear picture from these noisy and somewhat contradictory numbers, but it does not look like consumer and business sentiment are taking big hits following the recent interest rate increases, even though we are witnessing the most aggressive monetary tightening in decades.

The biggest source of uncertainty still lies in the global economy. The International Monetary Fund (IMF) in Washington published its World Economic Outlook, summarizing the road ahead as a “rocky recovery”. The baseline forecasts for GDP grow were revised downward slightly, to 2.8% in 2023 and 3.0% in 2024, with the slowdown concentrated in advanced economies. The report considers multiple scenarios, among them one which accounts for higher financial sector stress, which would shave half a percentage point off the growth rate in 2023. Global headline inflation in the baseline scenario is projected to fall from 8.7% in 2022 to 7.0% in 2023, assuming commodity and energy prices continue to flag. The IMF does not expect inflation to return to target before 2025 in most countries.

For the current (May) round, the Shadow Board’s assessment is identical to last month’s: it is attaching a 34% probability that pausing the tightening cycle is the appropriate policy and a 66% probability that another rate rise, above the current level of 3.60%, is the appropriate policy stance, with a mode recommendation of a 25 bp increase to 3.85%. Once again, the Board completely rules out the possible need to cut the overnight rate.

The probabilities at longer horizons have shifted slightly: 6 months out, the confidence that the cash rate should remain at the current setting of 3.60% equals 21%, down two percentage points from April; the probability attached to the appropriateness of an interest rate decrease equals 21%, up four percentage points, while the probability attached to a required increase equals 58% (down from 60% in April). The mode recommendation at this horizon is, once again, 3.85%, 25 bps above the current level, the same level as in the past three interest rate rounds.

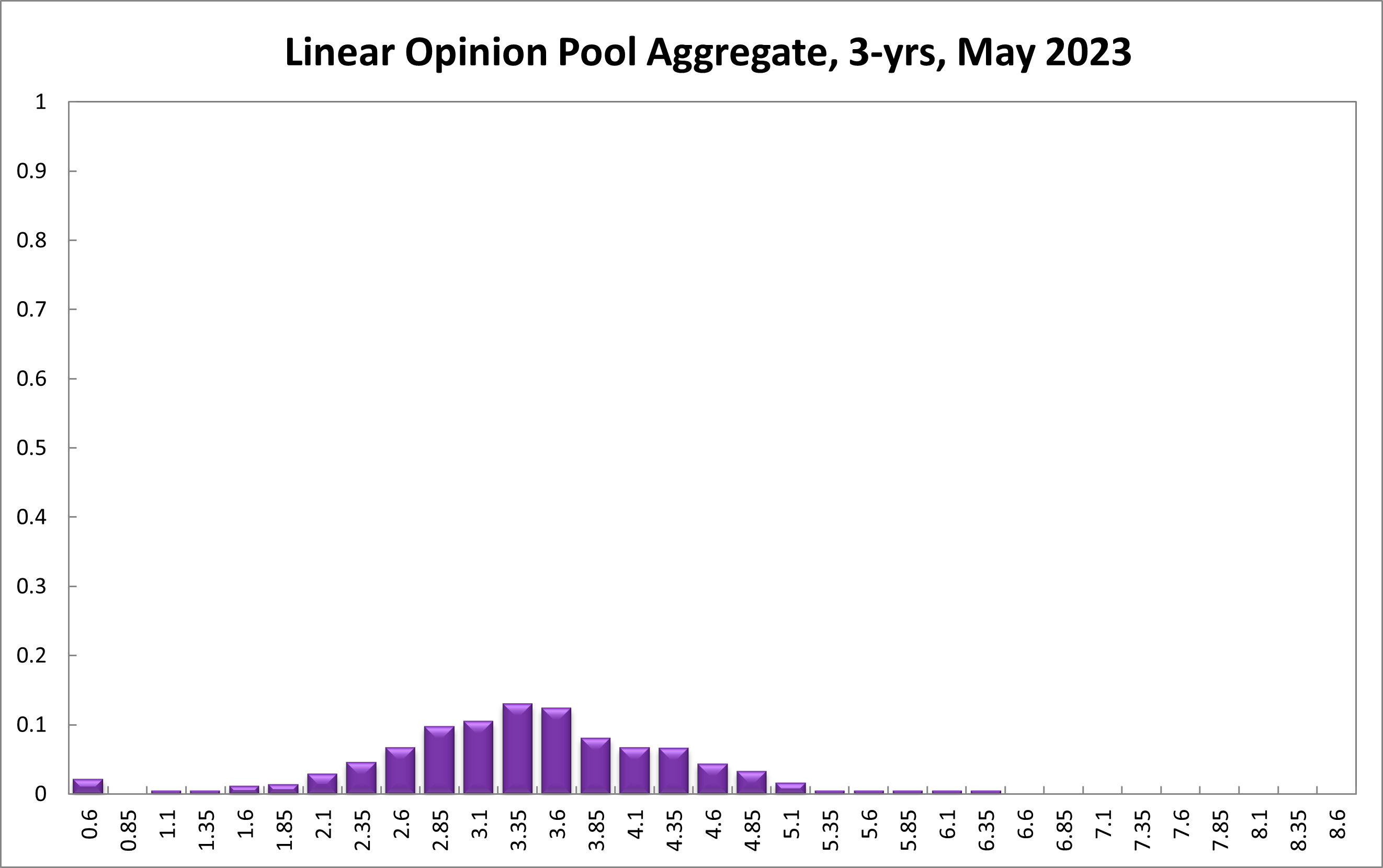

One year out, the Shadow Board members’ confidence that the appropriate cash rate is at the current level of 3.60% increased from 14% to 16%. The confidence in a required cash rate decrease, to below 3.60%, fell slightly, from 43% to 41%, and its confidence in a required cash rate increase, to above 3.60%, remained steady at 43%. Three years out, the Shadow Board attaches a 12% probability that the overnight rate should equal 3.60% (unchanged), a 54% probability that a lower overnight rate is optimal (up three percentage points) and a 34% probability that a rate higher than 3.60% is optimal (down three percentage points).

The range of the probability distribution for the current recommendation contracted, extending from 3.60% to 4.35% (compared to a range of 3.60% to 4.85% in the previous round). For the 6-month horizon it extends from 2.60% to 5.60% (compared to a range of 2.60% to 5.35% in the previous round). The range for the 12-month horizon, at 0.60%-5.85%, is unchanged, whereas the range for the 3-year horizon widened by 25 bps, from 0.60%-6.10% to 0.60%-6.35%.

Updated: 5 January 2025/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin