Outcome

Inflation is high and is a global phenomenon. In response to this, central banks around the world are increasing their policy rates rapidly. Just this June, the Fed increased their policy rate by 75 basis points. Yesterday (29th of June), the Wall Street Journal published that another large rate rise was possible in July and that an increase of “50 (basis points) or 75 (basis points) is clearly going to be the debate”.

It’s clear that global interest rates are on the rise. If the RBA does not increase interest rates, this would lead to a depreciation of the AUD dollar, which would improve the terms of trade but would further increase inflation.

The Australian economy is in a strong position, with very low unemployment and, as published recently by the ABS, a very large increase in vacancies (13.6 % from February 2022). Given the expectation of annual inflation reaching 7 % later this year, I believe it would be appropriate to further increase the policy cash rate in the July meeting.

Households appear to be holding up well against the current headwinds, with retail spending up over 10% y/y in May. While a moderation in growth is inevitable over the coming months, as the headwinds to spending begin to bite, the combination of further scope for the savings rate to fall (it is still comfortably above pre-COVID levels) and the excess savings buffer should underpin continued positive momentum through the rest of 2022 and into 2023.

The latest data also suggests that other parts of the economy are also holding up. Capital expenditure by businesses is projected to hold up over the next twelve months. And while some parts of government spending are likely to fall back, as pandemic spending unwinds and the new government implements the now-flagged spending reductions in their October budget, other parts are set to see further increases. There is a significant amount of infrastructure construction activity still in the pipeline, expenditure on defence is set to rise sharply, and health and social care (particularly aged care) are likely to be net beneficiaries in the next budget.

Overall, the outlook remains positive, and it is appropriate for the RBA to continue with further policy rate normalisation.

Moving into 2023, it is likely to become appropriate for the RBA to slow or even pause interest rate rises. The full impact of the monetary tightening implemented in 2022 will not be known until well into 2023, and the Board will need to monitor the data carefully to ensure that they haven’t gone too far, too fast. Their job will also be made easier by a fall back in headline inflation (assuming no further shocks to the global economy), as the pace of increase of food, fuel and other commodities falls back sharply from early 2023 onwards. Indeed, there is a risk that the Board have to reverse some of the rate rises they will have implemented in late 2023/early 2024, if momentum slows too much or even turns negative.

The shift in inflation globally and in Australia has led to a significant reassessment of what is required to bring inflation back to target levels. The shocks driving Australian inflation are demand increases (from fiscal and monetary stimulus internationally and in Australia) and supply contraction (supply chain disruptions from Covid and the war in Ukraine, including energy and food shocks, as well as other key supply chain inputs, plus weather events such as the Australian floods). The RBA should be responding to the demand shocks but not the supply shocks (especially if the supply disruption is expected to improve). Fiscal policy also plays an essential part in supporting monetary policy by not further stimulating demand. Current events make this a difficult period for the RBA, and clarity of the communication of the policy rule acknowledging the uncertain effects of recent shocks and uncertainty about possible future shocks is as important as how much interest rates respond in the short term.

The global economic outlook is mixed and there is clearly a growing possibility of recession within the next 12 months. If this happens, the RBA should immediately reverse its raising cycle. In the meantime, they should be cautious about raising the policy rate quickly unless longer-term inflation expectations start to rise towards the top end or above the 2-3% target range. It is more important for fiscal policy than monetary policy to normalise at this time.

Updated: 22 November 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Shadow Board Recommends Yet Another Rate Rise

A tight labour market and high capacity utilisation rate, as well as substantive supply-side constraints, point to a further increase in the (headline) CPI inflation rate later this year, above the most recent reading of 5.1% (Q1 of 2022). The current environment, in which demand is strong and supply hampered, leave little option for the RBA but to increase interest rates, if it wants to bring inflation back into the mandated target band of 2-3%. This is clearly the view of the RBA Shadow Board, which is 70% confident that the overnight rate should be raised to above the current setting of 0.85%, whilst only attaching a 30% probability that keeping the overnight rate on hold this round is the appropriate policy.

The Australian labour market statistics remain strong. The official ABS (seasonally adjusted) unemployment rate remained steady at 3.9% in May, as predicted. The youth unemployment also kept steady, at 8.8%. Encouragingly, total employment increased by more than 60,000, with nearly 70,000 full-time positions filled. The labour force participation rate increased 0.3 percentage points, to 66.7%. The underemployment rate also improved noticeably; it fell from 6.1% to 5.7%, while monthly hours worked increased yet again, by 17 million, or 0.9%. Other indicators such as job vacancies and job advertisements also improved, underlining the remarkable strength of the Australian labour market. What remains unclear at this stage is the extent to which the labour market tightness will lead to wages growth. Most recent data, which is still from Q1 of 2022, shows that real wages are contracting. Unless the inflation rate quickly settles down inside official target band, which looks unlikely, nominal wages should continue to rise to make up for lost ground.

The Aussie dollar lost 4 US¢ since last month, finishing the second quarter just above 68 US¢. Yields on Australian 10-year government bonds have consolidated after the recent steep rise, equalling 3.47% on 1 July. Yield curves retain their normal convexity, and interest rate spreads, especially at longer term maturities (e.g. 10-year versus 2-year) have remained roughly stable. Australian stock prices continued their broad decline, in tune with global share prices: the S&P/ASX 200 stock index ended the past month below 6,600, some 650 points lower than a month earlier.

The challenges for the global economy are not going away any time soon: commodity shortages, high energy prices, inflation, disrupted global supply chains, the Ukraine war, Covid-19, natural disasters. Most OECD central banks are expected to lift policy rates by substantial amounts in order to curb inflation. In this environment it will be difficult for the RBA not to follow suit.

The inflation risks and wider concerns about the economy manifest in a further slide in consumer confidence: the Melbourne Institute and Westpac Bank Consumer Sentiment Index dropped for the seventh month in a row, to 86.35 in June. Retail sales basically remained flat, while private sector credit growth slowed slightly. Business confidence likewise suffered; NAB’s index of business confidence deteriorated from 10 to 6 in May, and the services PMI dropped from 57.8 to 49.2 in the same month. The manufacturing PMI, on the other hand, improved slightly, for the month of June. The capacity utilisation rate increased again, by more than a full percentage point, to 84.95%. The Westpac-Melbourne Institute Leading Economic Index fell by a mere 0.06% year-on-year, based on its most recent reading in May. Its six-month annualised growth rate declined further, to a paltry 0.58% in May. The S&P Global Australia Composite PMI was unable to regain any strength after its recent drop. The weak consumer and business confidence numbers stand in contrast to the strong current economic indicators, a difficult situation to navigate for policymakers.

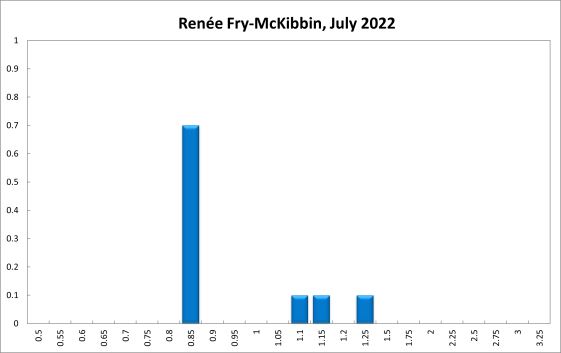

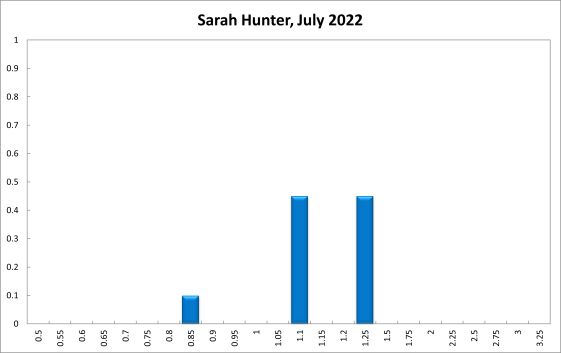

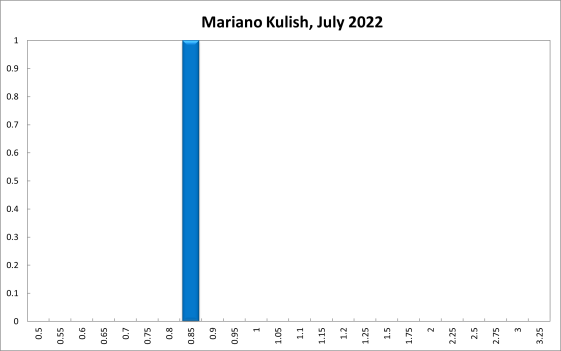

Two months ago the Reserve Bank of Australia embarked on a tightening cycle after the official cash rate target stood at the historically low level of 0.1% for one-and-a-half years. For the current (July) round, the Shadow Board is advocating that the overnight interest rate be raised further, above the current level of 0.85%, attaching a 70% probability that this is the appropriate policy stance. It attaches a 30% probability that keeping the overnight rate on hold is the appropriate policy and a 0% probability that a decrease is appropriate.

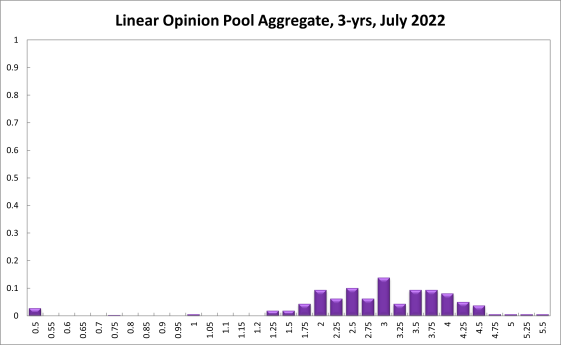

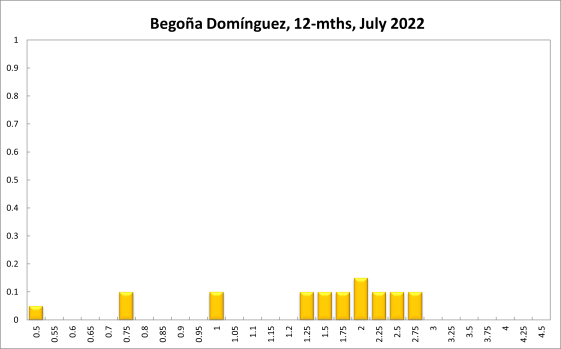

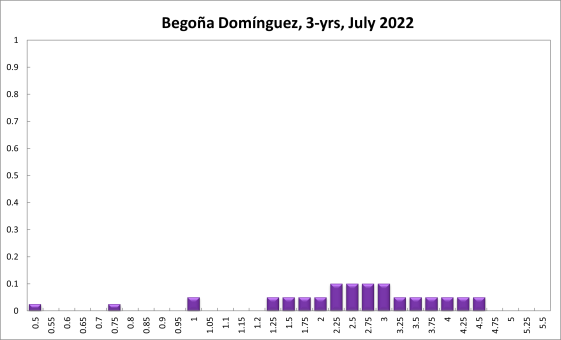

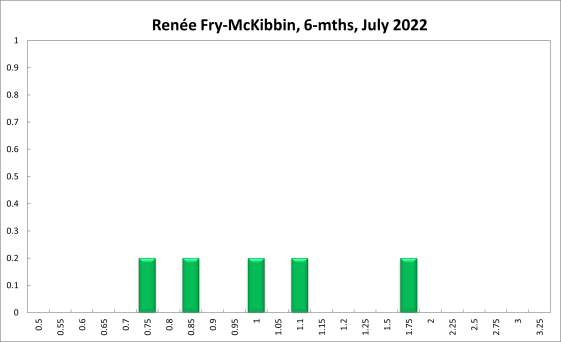

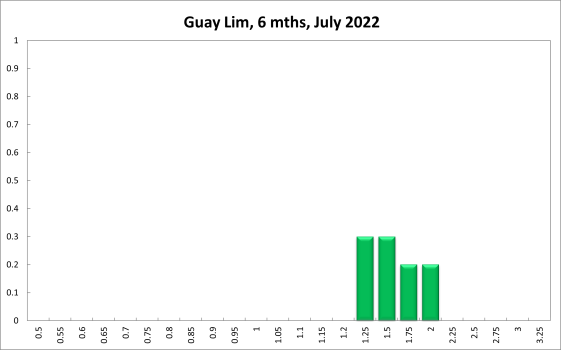

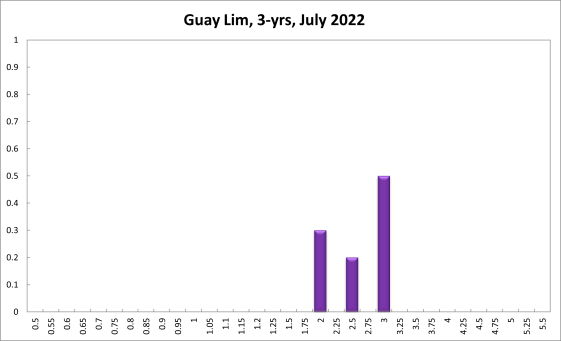

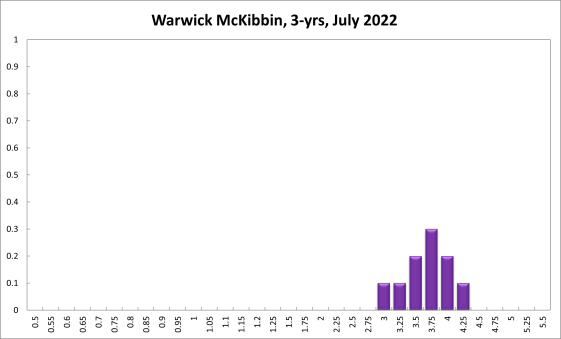

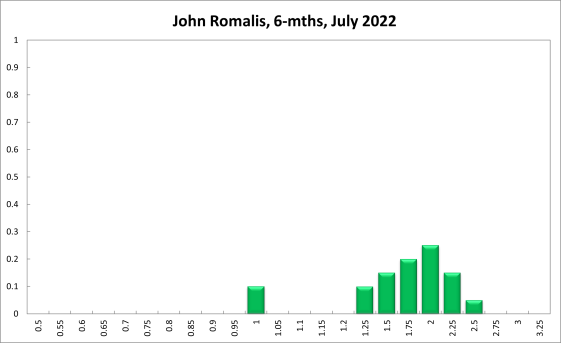

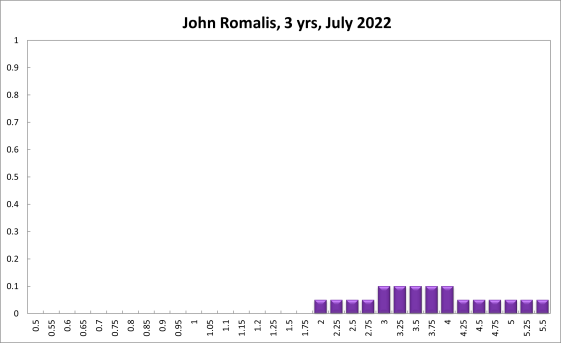

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at the current setting of 0.85% equals 6%; the probability attached to the appropriateness of an interest rate decrease equals 3%, while the probability attached to a required increase equals 91%. One year out, the recommendations are similar. The Shadow Board members’ confidence that the cash rate should be held steady equals 3%. The confidence in a required cash rate decrease, to below 0.85%, is 6% and in a required cash rate increase, to above 0.85%, equals 92%. Three years out, the Shadow Board attaches a 0% probability that the overnight rate should equal 0.85%, a 3% probability that a lower overnight rate is optimal and a 97% probability that a rate higher than 0.85% is optimal.

The range of the probability distributions for the current and 6-month recommendations, widened considerably, reflecting a reassessment by at least some members of the tail risks: for the current setting, it extends from 0.85% to 2.25%, and for the 6-month horizon it extends from 0.75% to 3.25% (compared to a range of 0.1 to 2% in the previous round). The range for the 12-month horizon expanded even more – it now extends from 0.5% to 4.5% - and likewise for the 3-year horizon, which now extends from 0.5% to 5.5%.