James Morley

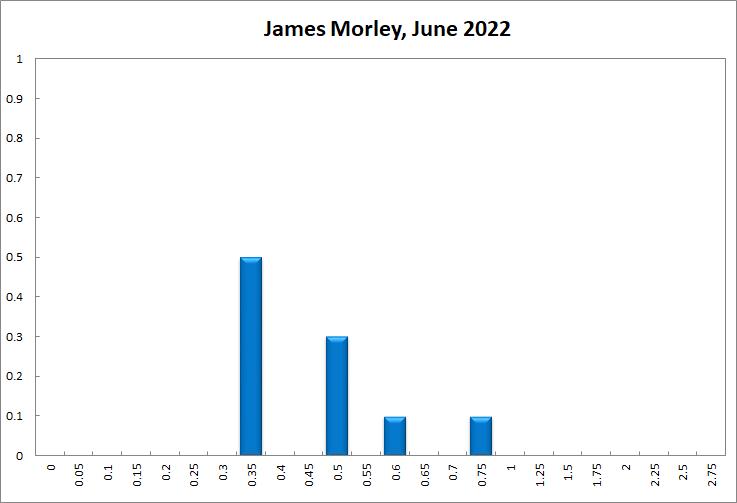

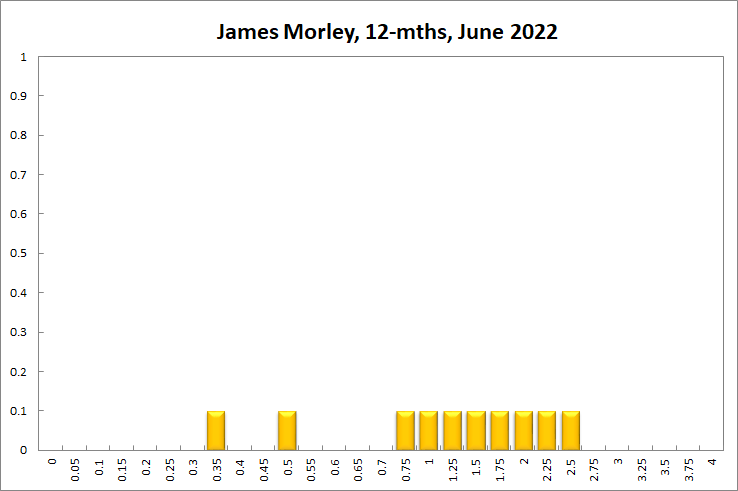

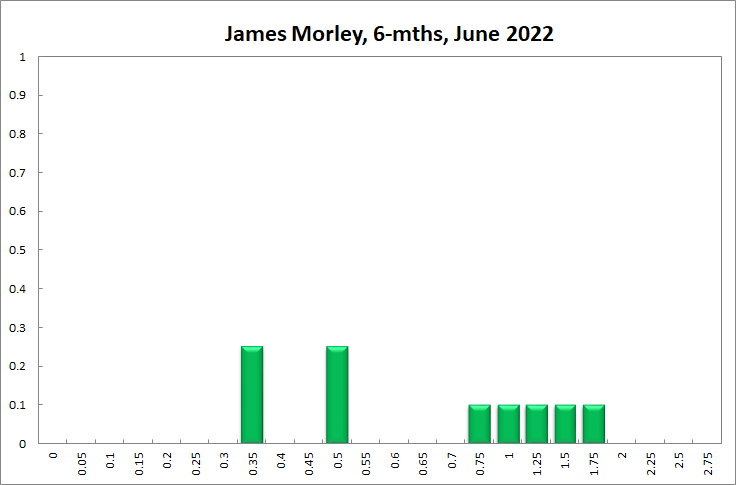

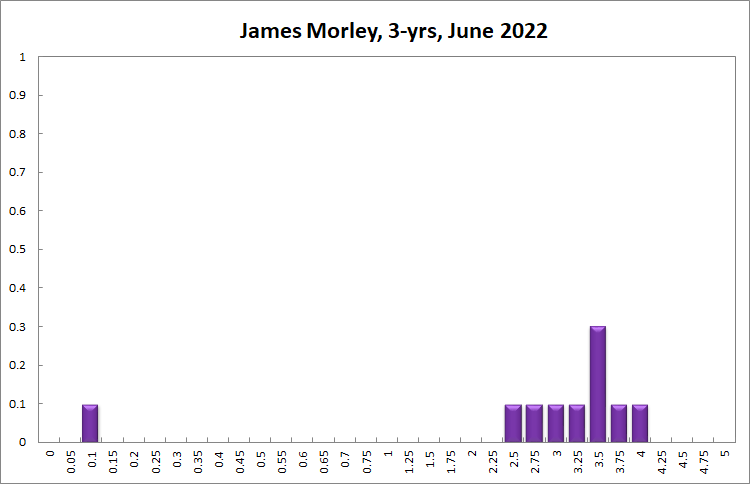

Now that the RBA is in a raising cycle, I don’t think they should immediately reverse themselves by moving back to the ZLB unless there is a quick deterioration in economic conditions globally (possible) or domestically (unlikely in the near term). However, given that wage growth came in weaker than anticipated by the RBA in making their decision to start raising the cash rate last month, they could pause the raising cycle or just raise 15bps to bring the cash rate to 50bps, a more conventional level than, say, 35bps or 60bps. Raising to 75bps is possibly justified by the very high year-ended GDP deflator inflation for 2022Q1. But if inflationary pressures do ease, the RBA risks raising too quickly and needing to correct with long and variable lags. Generally, it is more important for fiscal policy than monetary policy to return quickly to neutral at this point, at least as long as long-term inflation expectations measures such as the 10-year breakeven rate remain anchored within the 2-3% target range.

Updated: 27 December 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin