Sarah Hunter

The economic data continue to confirm that demand in the economy is running hot relative to supply. Furthermore, developments globally over the last month have confirmed that this year’s shocks to commodity markets and supply chains have become at least semi-permanent (and in some cases have worsened) – further policy tightening is needed to realign supply side capacity with demand.

Against a more inflationary global backdrop, there is further evidence of broadening inflation pressures domestically, with the domestic final demand price deflator rising 1.4% q/q in March quarter. It is also looking increasingly likely that this year’s award wage setting process and collective bargaining agreements will result in significant pay rises for those covered by these agreements, while momentum in private sector wage setting looks likely to deliver wage increases of c.3.5% on average.

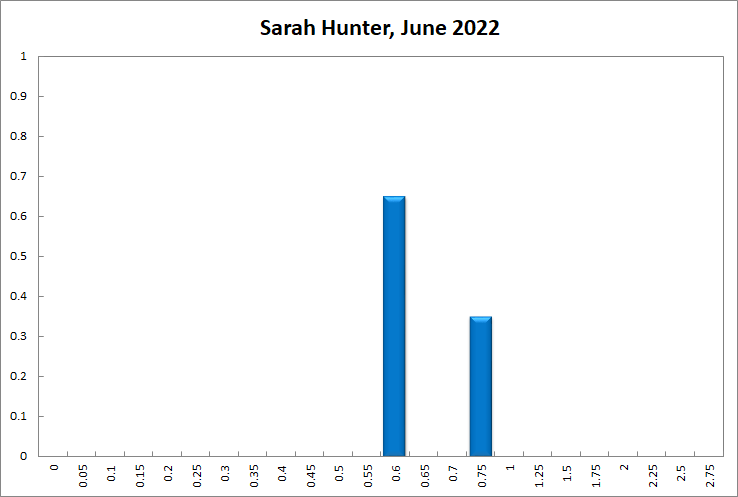

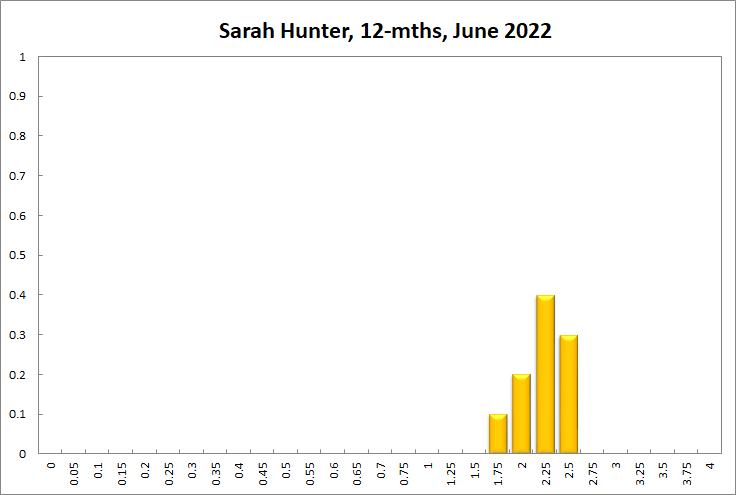

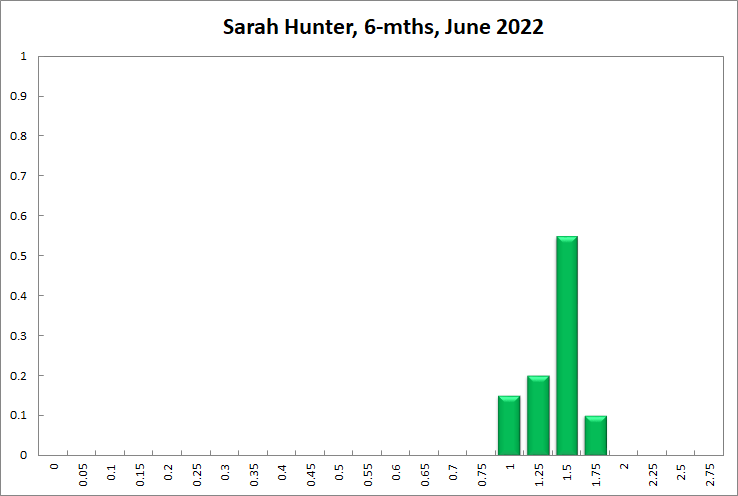

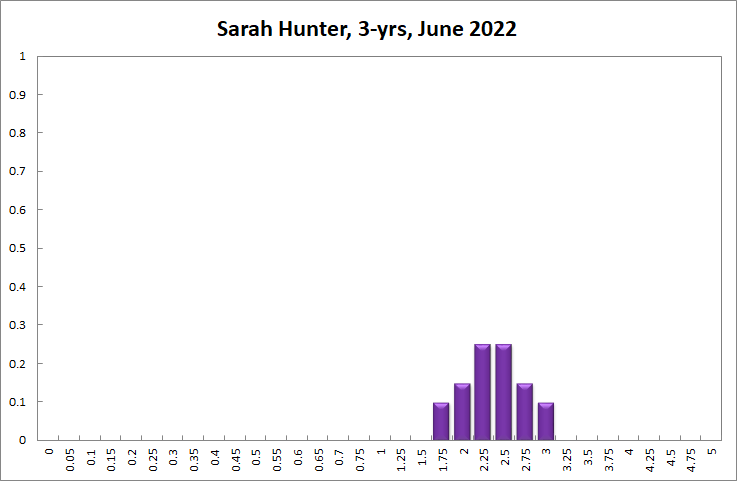

To ensure that inflation expectations remain anchored and mitigate the need for a much sharper slowdown in growth momentum in the future, the RBA Board should raise the cash rate again at its June meeting, and follow this with further rate rises through 2022 and H1 2023.

Updated: 1 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin