Aggregate

Shadow Board Marginally in Favour of Cash Rate Rise

The annual (headline) CPI inflation rate in Australia jumped to 5.1% in the first quarter of 2022, up from 3.5% in Q4 of 2021 and 0.5 percentage points higher than the consensus forecast. The RBA Trimmed Mean CPI increased by 3.7% (up from 2.6% in the December quarter), well above the RBA’s official target band of 2-3%. The latest GDP growth figure of 3.4% is still from the December quarter of 2021. The RBA Shadow Board’s verdict has shifted in favour of a rate rise. Although “no change” is the mode recommendation, the Shadow Board is only 47% confident that keeping the cash rate steady at its historic low is the appropriate policy setting. Correspondingly, it attaches a 53% probability that an interest rate increase to 0.25%, or higher, is appropriate.

The official ABS (seasonally adjusted) unemployment rate held steady at 4% in March; youth unemployment remains above 9%. Total employment increased by 17,900 and full-time employment by 20,500. The labour force participation rate, at 66.4%, did not budge. The underemployment rate dropped slightly to 6.3%, while monthly hours worked contracted by 0.6%. The RBA stated some time ago that it would like to consider the newest data on the wage price index (WPI), to be released on 18 May, before deciding on a possible interest rate increase. Indeed, given the high rate of headline inflation, next month’s WPI will provide significant information about the wider inflationary pressures in the economy.

The month of April has seen the Aussie dollar plummet from a local high of 76 US¢ to just above 71 US¢. Yields on Australian 10-year government bonds continued to rise, from a recent low of approximately 1.65% four months ago to 3.16% on the last week day in April. Yield curves retain their normal convexity. Interest rate spreads have narrowed along all segments of the yield curve, from short-term maturities (2-year versus 1-year) to higher-term maturities (10-year versus 2-year), indicative of an overall flattening of the yield curve. Australian stock prices have consolidated after a brief weak spell in the previous month; the S&P/ASX 200 stock index is trading near 7,400, 100 points lower than one month ago.

The outlook for the global economy is darkening in the face of commodity shortages, high fuel prices, and disrupted global supply chains, with the IMF in its April World Economic Outlook revising down global GDP growth forecasts to 3.6% in 2022 and 2023. Coupled with large fiscal stimuli in many economies, the supply-side constraints have dramatically pushed up global inflation rates, to as high as 8.5% in the US. Numerous central banks have raised their cash rate recently, including the Federal Reserve, the Bank of Canada, the Bank of England, and the Reserve Bank of New Zealand. All central banks have flagged further rate rises in the coming months, adding pressure on the RBA to follow suit. The Ukraine war and rising geopolitical tensions elsewhere add to the tail risks, raising the possibility – according to some financial market analysts – of the world economy slipping into recession in 2023, or earlier: the US economy contracted by an annualized 1.4% in the first quarter of this year.

Australian consumer confidence softened for the fifth consecutive month; the Melbourne Institute and Westpac Bank Consumer Sentiment Index fell from 101 in February and 96.6 in March to 95.7 in April. Private sector credit growth slowed from 0.6% month-on-month, to 0.4%, largely attributable to a contraction in consumer credit. NAB’s volatile index of business confidence improved for the third month in a row, coming in at 16 in March, compared to 13 in February. In the same period, the manufacturing PMI likewise improved slightly, from 53.2 to 55.7, while the services and PMI deteriorated from 60 to 56.2. The capacity utilization rate is continuing to recover from a recent trough, posting a 0.6 percentage point gain to 83.1%. The Westpac-Melbourne Institute Leading Economic Index for March rose by 0.3% year-on-year, after a revised increase of 0.4% in the previous month; the IHS Markit Australia Composite PMI is likewise indicative of an economic expansion.

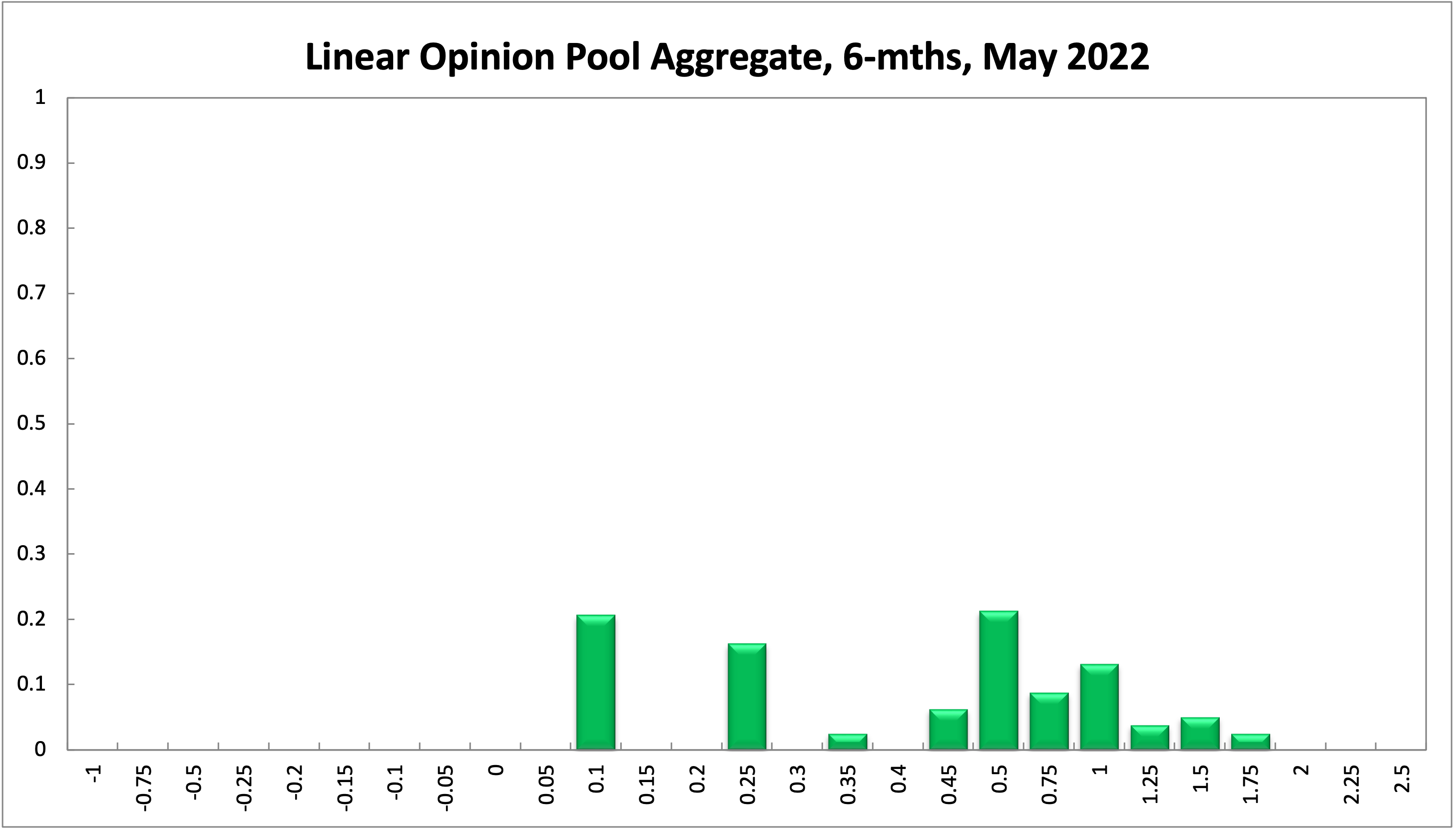

The official cash rate target has been at the historic level of 0.1% for 17 months. The Shadow Board’s conviction to keep the overnight interest rate at this historic low weakened considerably. While “no change” is the mode recommendation, the Board only attaches a 47% probability that this is the appropriate policy (down from 86% in April) and a 53% probability that an increase is appropriate (up from 13%).

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at 0.1% weakened further, from 33% in April to 21% in the current round; the probability attached to the appropriateness of an interest rate decrease remains unchanged at 0%, while the probability attached to a required increase correspondingly rose from 67% to 79%. One year out, a similar picture emerges. The Shadow Board members’ confidence that the cash rate should be held steady fell again, from 13% in April to 4% in this round. The confidence in a required cash rate decrease, to below 0.1%, is 0% (unchanged) and in a required cash rate increase 96% (88% in April). Three years out, the Shadow Board attaches a 7% probability that the overnight rate should equal 0.1% (unchanged) and a 93% probability that a rate higher than 0.1% is optimal (also unchanged). The range of the probability distributions widened, reflecting a reassessment by at least some members of the tail risks: for the 6-month horizon it extends from 0.1% to 1.75% (compared to a range of 0.1% and 1% in the previous round), for the 12-month horizon from 0.1% to 2.5% (compared to a range of 0.1% and 2% in the previous round), and for the 3-year recommendation from 0.1% to 4.25% (compared to a range of 0.1% and 4% in the previous round).

Updated: 5 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin