Outcome

Inflation is rising globally. In the U.S.A., the C.P.I. increased 7.5 per cent over the last 12 months. Wage growth is also on the rise, with an increase of over 5 per cent. On January 26th, the U.S. Federal Reserve signalled their intention to start the “lift-off”, i.e. increase interest rates. The president of the Federal Reserve Bank of St. Louis, James Bullard, believes that such increase in the policy rate could happen as early as March 2022 and expects as many as three increases in the policy rate during 2022.

Inflation is also increasing in Australia. Currently, the year-ended C.P.I. inflation is at 3.5 per cent. Wages have increased by 2.3 per cent according to data just released by the A.B.S.. Should the RBA signal also a lift-off? If yes, when?

I think it is important to establish a policy strategy on monetary policy normalisation (lift off and balance sheet management) and to communicate this strategy to the public.

However, inflation data in Australia is clearly healthier than that of the U.S.A. and/or Europe. Moreover, it is also not as high for our main trading partners. Importantly, many of the drivers of this inflation are largely outside of the control of the RBA. Supply chain disruptions are still in place and resolved only slowly. Now geopolitical factors (specifically Ukraine) are further pushing up petrol prices. Uncertainty is at one of its highest in decades, with the end of the pandemic still unclear and with the real and imminent possibility of war in Europe.

Given this situation, a lift-off of the cash rate in Australia just now would be premature.

Having said this, there are clear inflation risks ahead. And the RBA has a role to anchor expectations of inflation. Then, if inflation continues rising and wage growth picks up further, a lift-off should happen.

The latest data further confirms that the economy remains on track despite the short, sharp shock from omicron. Although hours worked fell sharply in January as a result of a sharp rise in people off sick, employment rose modestly, and the unemployment rate held steady at 4.2%. The tightness of the labour market is steadily translating into an upturn in wages growth, with the December quarter seeing a 2.3% gain on a year earlier, and price inflation is also being underpinned by global shifts in commodity prices.

Fiscal settings remain supportive and based on the high frequency data a further rebound in consumer spending (enabled by the re-opening of the economy) looks to be underway. And business investment intentions are still very buoyant, despite headwinds from rising inflation and borrowing costs.

Moving through 2022 momentum will naturally wane, as the easy gains from re-opening are exhausted and inflationary pressures weigh on household spending (notwithstanding a pick-up in wages growth). Government spending is also likely to fall back as emergency pandemic spending comes to an end. Taking these competing trends together, it will be appropriate for the RBA to begin raising the cash rate from Q3 2022 onwards but for the normalisation to proceed at a relatively steady pace after this. Compared to other central banks globally, the RBA is likely to lag behind in this cycle – the RBA do not need to be concerned about this, indeed it can be useful if leads to a depreciation of the AUD (which will ultimately feed through to improve the trade balance).

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Confidence in Keeping Cash Rate At Historic Low Gradually Waning

The annual (headline) inflation rate in Australia remains at 3.5% in the December quarter of 2021, well above the RBA’s official target band of 2-3%, even if the RBA’s trimmed mean CPI inflation rate equalled 2.6%, barely above the target band’s midpoint. The latest data on GDP will not be released until the day after the RBA meets to decide on interest rates. After the 1.9% contraction in Q3, GDP is projected to increase by 2.5% in Q4 of 2021. The RBA Shadow Board’s verdict is, once again, unchanged from the previous month: the overnight interest rate should remain at the current historic low; however, the confidence of this recommendation has weakened slightly, from 94% to 83%.

The official ABS unemployment rate remained steady at 4.2% in January. Whilst still too high, youth unemployment continues to improve, most recently equalling 9.4% (December 2021). Total employment grew by nearly 13,000, and the labour force participation rate edged up from 66.1% 66.2%. The underemployment rate ticked up, from 6.6% to 6.7%, reflecting a drop in full-time employment relative to part-time employment. Monthly hours worked contracted by 8.8%, bearing in mind that this includes the summer holiday period and a brief spike in Omicron-related sick days. (Nominal) wages merely increased by 2.3% in Q4 of 2021, up 0.1 percentage points from the previous quarter. This is less than the current inflation rate and implies that average real wages are falling, lessening the household sector’s purchasing power. While the unemployment rate looks favourable in a historical context, the persistent underemployment may prevent this from generating significant wage pressure. In the medium- to long-run, we need to see positive real wage growth or else the labour income share will continue to fall.

The Aussie dollar continues to be range-bound, oscillating between 70 and 72 US¢. Mirroring the global rise in interest rate, yields on Australian 10-year government bonds continued to climb, from a recent low of approx. 1.65% two months ago to 2.23% on 25 February. Correspondingly, the yield curves, all convex, have become a bit steeper. Interest rate spreads have shifted along the maturity profile: for short-term maturities (2-year versus 1-year) the spread is now 51.9 points; in mid-term versus short-term maturities (5-year versus 2-year) the spread is 75.2 bps and in higher-term maturities (10-year versus 2-year) the spread remains virtually unchanged at 101.1 bps. The Australian share market, after a mid-month high, fell rapidly, as did most stock markets worldwide; the S&P/ASX 200 stock index is again trading below 7,000.

Globally, the risks have precipitously shifted from concerns about Covid-19 to geostrategic issues, in particular the Russian invasion of the Ukraine earlier this week. This armed conflict greatly adds to uncertainty surrounding the global outlook and threatens to exacerbate the bottlenecks in global supply chains and energy markets. Consequently, inflationary pressures may persist for longer than anticipated, depending on how the conflict evolves. Should the war in Ukraine continue to intensify and even extend to neighbouring countries, the consequences could be terrifying. Given the recent high rates of CPI inflation and nominal wages growth, there is still a consensus that the Federal Reserve in the US will start tightening monetary policy as early as next month, with other central banks to follow shortly thereafter. However, recent events may lead to a modest reassessment and, at any rate, the need for the RBA to begin its cycle of rate rises is smaller compared to other advanced economies.

Australian consumer confidence barely changed; the Melbourne Institute and Westpac Bank Consumer Sentiment Index fell from 102 to 101 in February. Retail sales, after the exceptional 7.3% month-on-month increase in November, contracted by 4.4%, as forecast. NAB’s index of business confidence, which tends to be volatile, rebounded from -12 in December to 3 in January, reflecting the opening of eastern states’ economies. The services and manufacturing PMIs remained flat. The rebound in nationwide activity is reflected in a full percentage point increase of the capacity utilization rate, to 81.61%. The index measuring new orders, prepared by the Australian Chamber of Commerce and Industry, reached the highest level ever in Q4 of 2021. At the same time, the Westpac-Melbourne Institute Leading Economic Index rose by 0.1% year-on-year in January 2022, and the IHS Markit Australia Composite PMI climbed to a 9-month high of 55.9 in February. These are clear signs that aggregate demand is expanding.

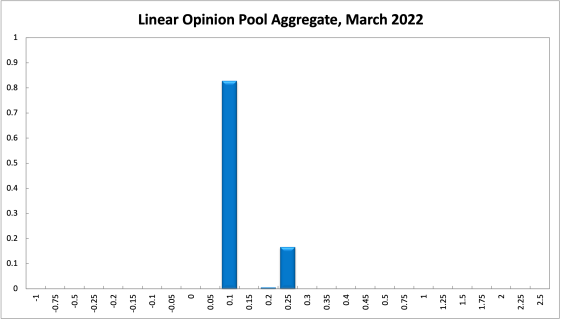

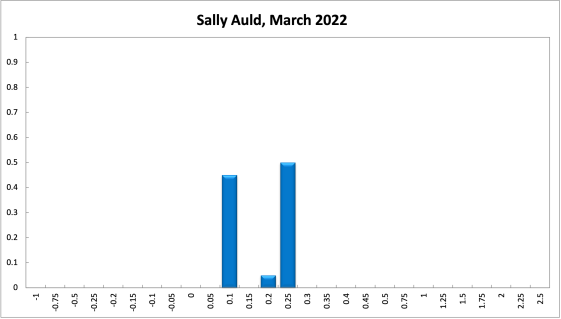

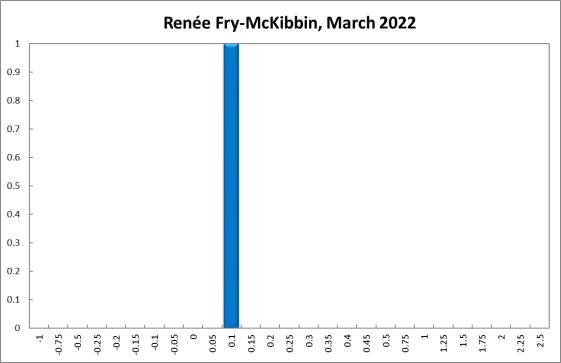

The official cash rate target has been at the historic level of 0.1% for 15 months. Though still strong, the Shadow Board’s conviction that the overnight interest rate should remain at this historic low for another round has weakened further. It attaches an 83% probability that “no change” is the appropriate policy (down from 94%) and a 17% probability that an increase is appropriate (up from 6%).

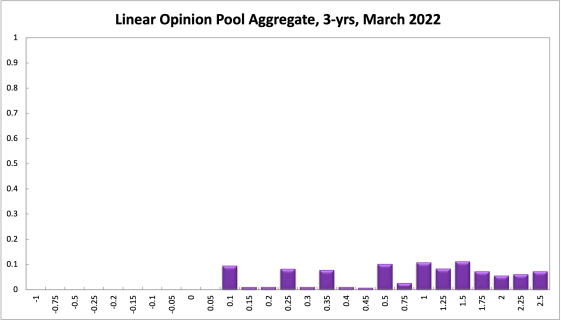

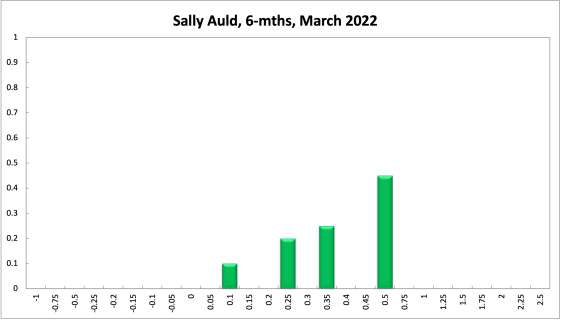

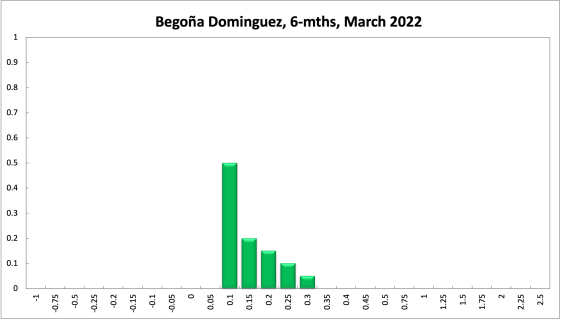

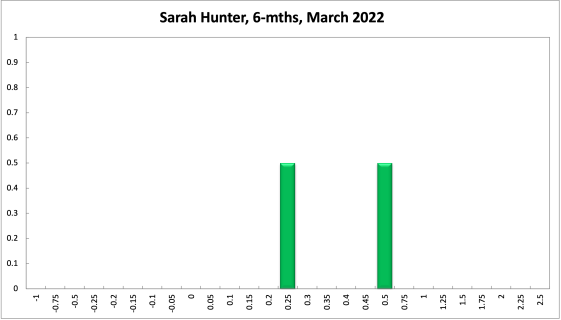

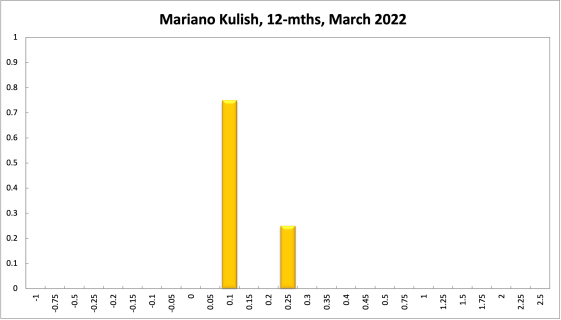

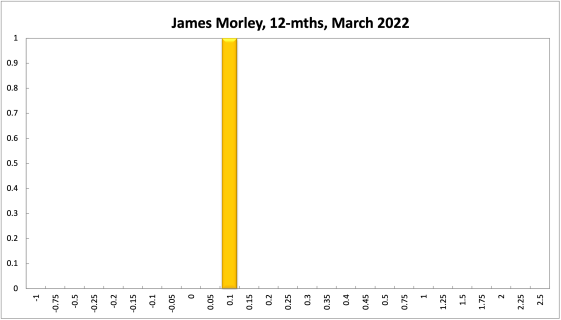

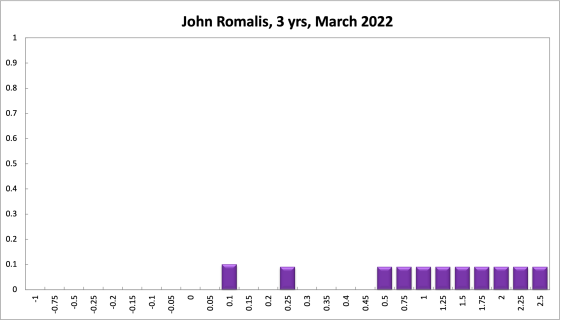

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at 0.1% has also continued to fall, from 59% in February to 51% in the current round; the probability attached to the appropriateness of an interest rate decrease remains unchanged at 0%, while the probability attached to a required increase correspondingly rose from 41% to 49%. One year out, a similar picture emerges. The Shadow Board members’ confidence that the cash rate should be held steady dropped again, from 39% in February to 33% in this round. The confidence in a required cash rate decrease, to below 0.1%, is 0% (unchanged) and in a required cash rate increase 67% (61% in February). Three years out, the probabilities shifted slightly in the opposite direction: the Shadow Board attaches a 9% probability that the overnight rate should equal 0.1% (up seven percentage points), a 0% probability that a rate lower than 0.1% is appropriate, and a 90% probability that a rate higher than 0.1% is optimal (down eight percentage points). The range of the probability distribution remain unchanged: for the 6-month horizon it extends from 0.1% to 0.75%, for the 12-month horizon from 0.1% to 2% and for the 3-year recommendation from 0.1% to 2.5%.