Sarah Hunter

The data released this month has broadly confirmed my view of the recovery. The easy wins from re-opening have largely been exhausted, and so growth momentum is now slowing to a more normal, sustainable pace. It looks as though the end of JobKeeper has not had a significant impact at the macro level and the outlook is still generally positive – I expect the economy will expand by over 4% this calendar year.

But challenges and risks remain. The latest Melbourne lockdown and spike in cases in other Asian economies that were previously successfully controlling COVID-19 highlights that until the majority of the population are vaccinated the risk of an outbreak and tighter restrictions remain. And it will not be possible for the economy to fully recover until all restrictions are removed. The labour market data is now starting to confirm the expected patchy nature of the recovery; NSW and VIC, who are most exposed to international tourism and higher education, are yet to return to pre-COVID employment levels while QLD and WA have moved significantly beyond this.

This macro observation aligns with survey data and other micro indicators that are flagging labour shortages in specific regions and sectors. How well the economy is able to shift resources to the states where demand is strongest, and away from the regions where it is relatively weak, will be a key determinant of the economy’s performance going forward.

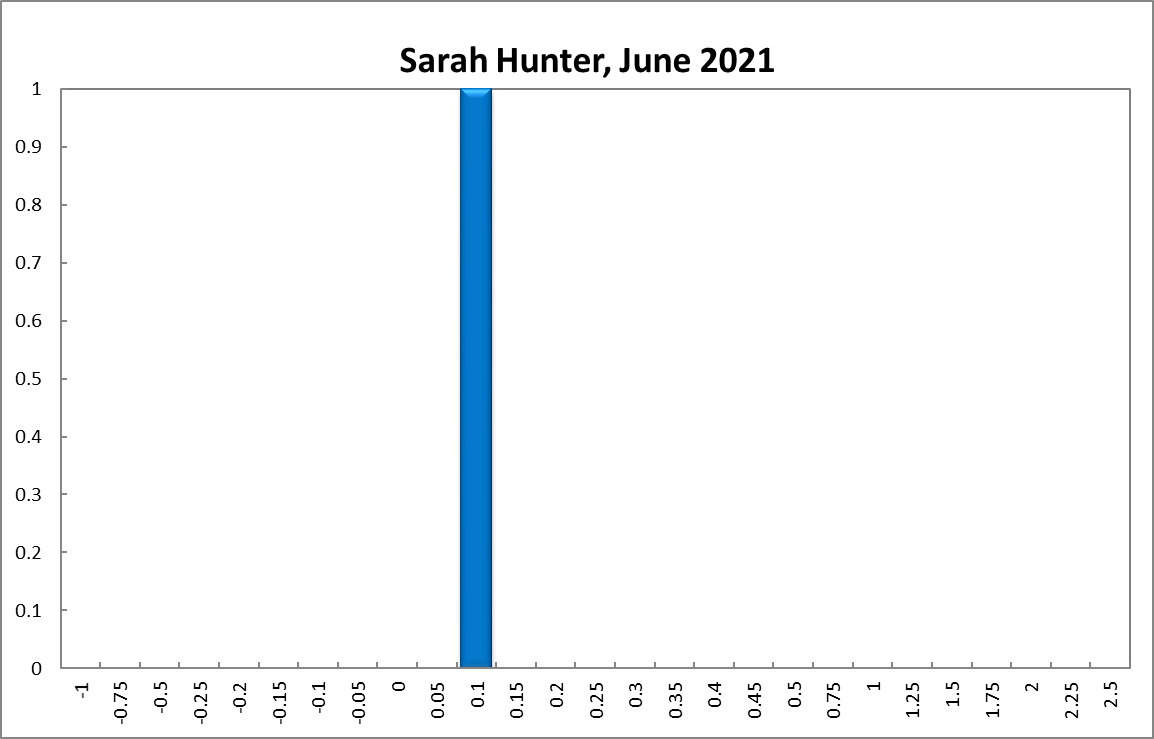

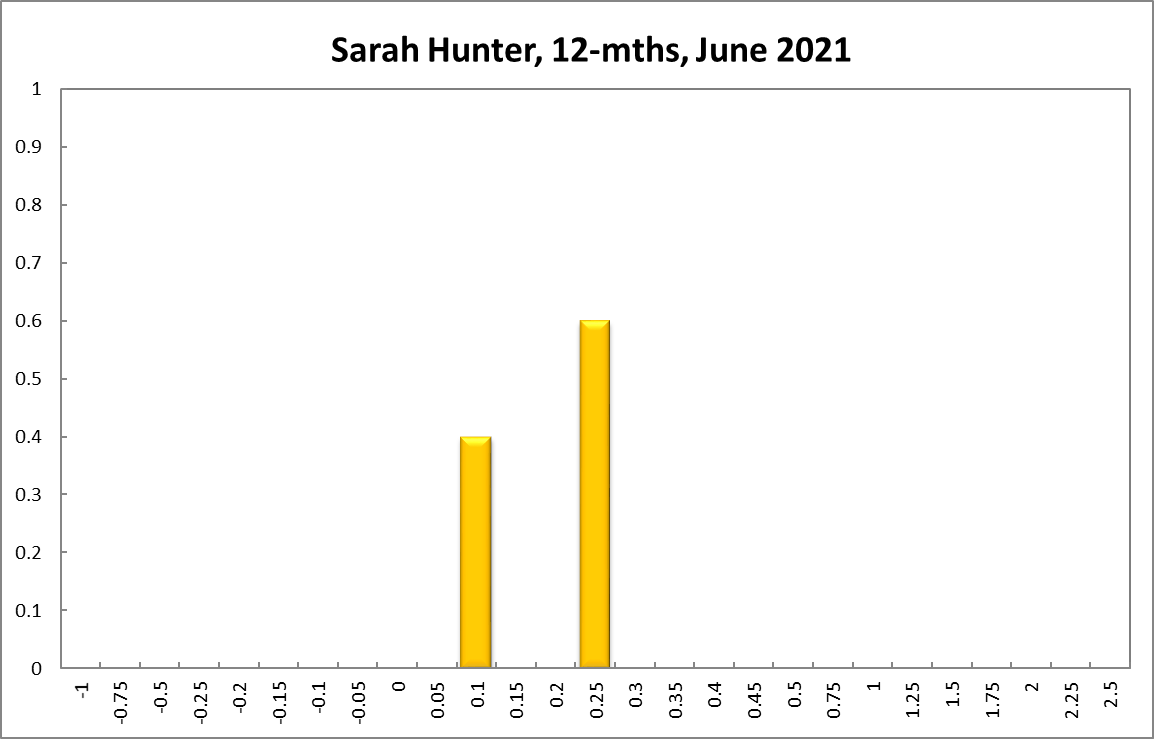

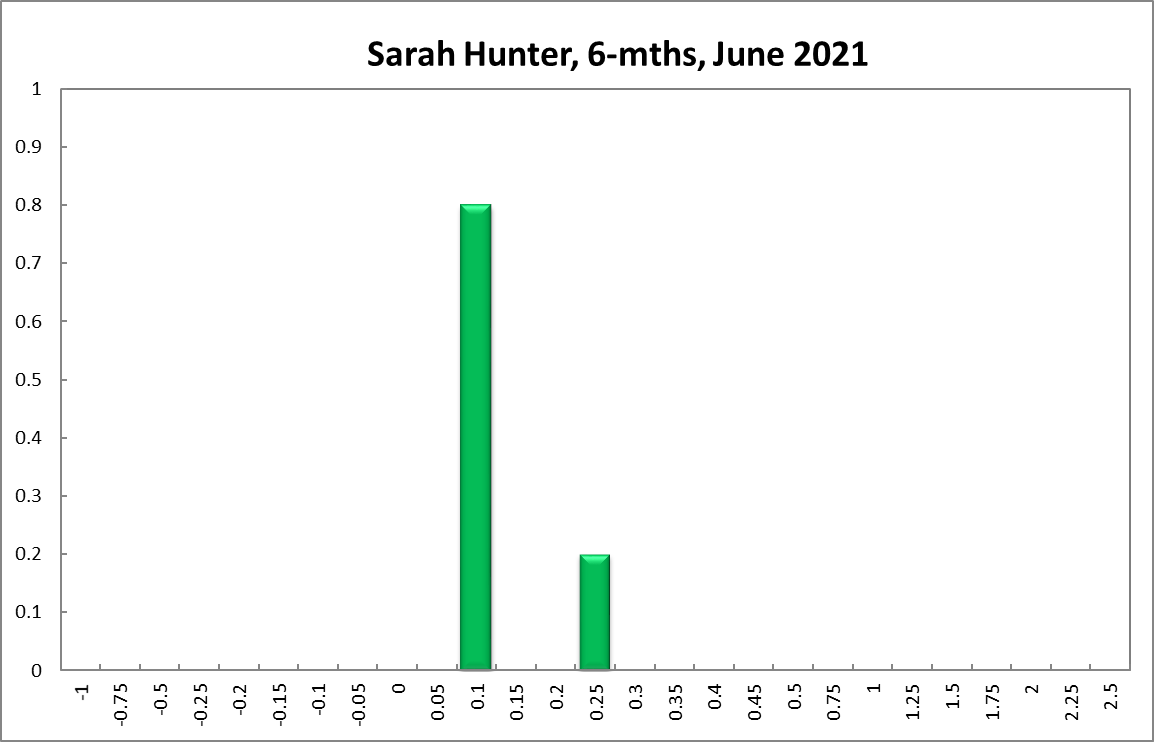

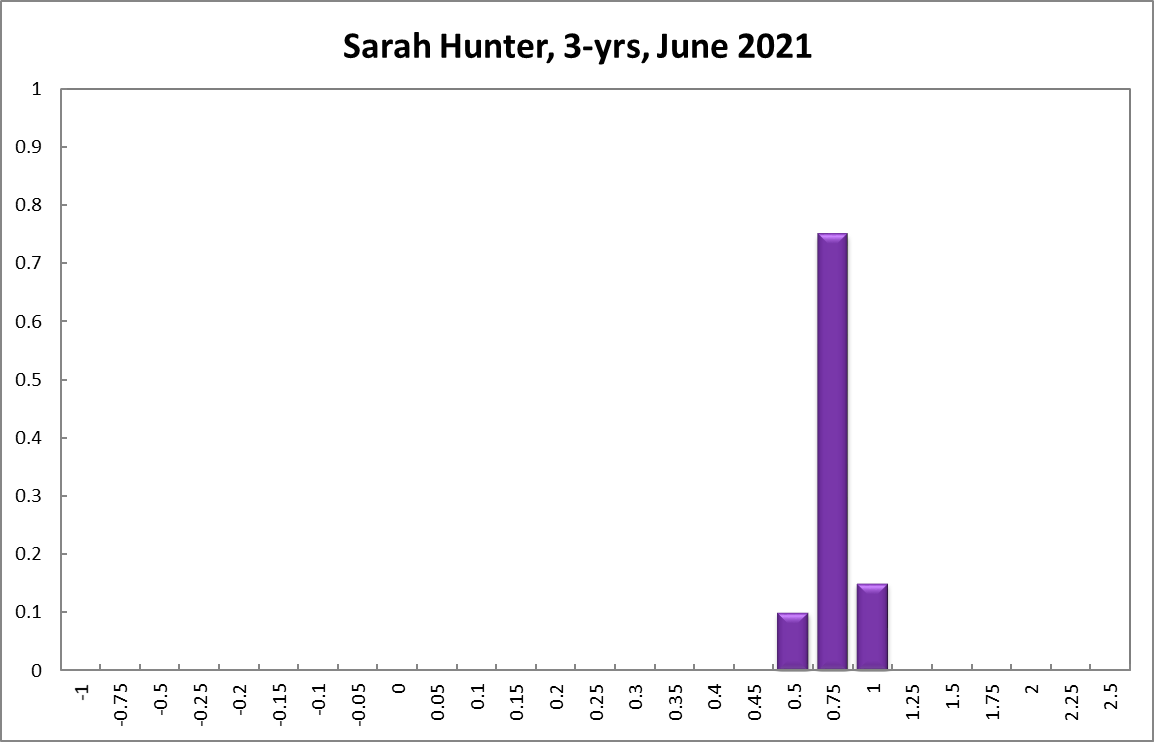

Given this remaining risks and challenges, and the need for a broad-based recovery to be well-entrenched to anchor inflation expectations and outcomes within the 2-3% target band, it is right for the RBA to hold its current settings through the rest of this year.

Updated: 24 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin