James Morley

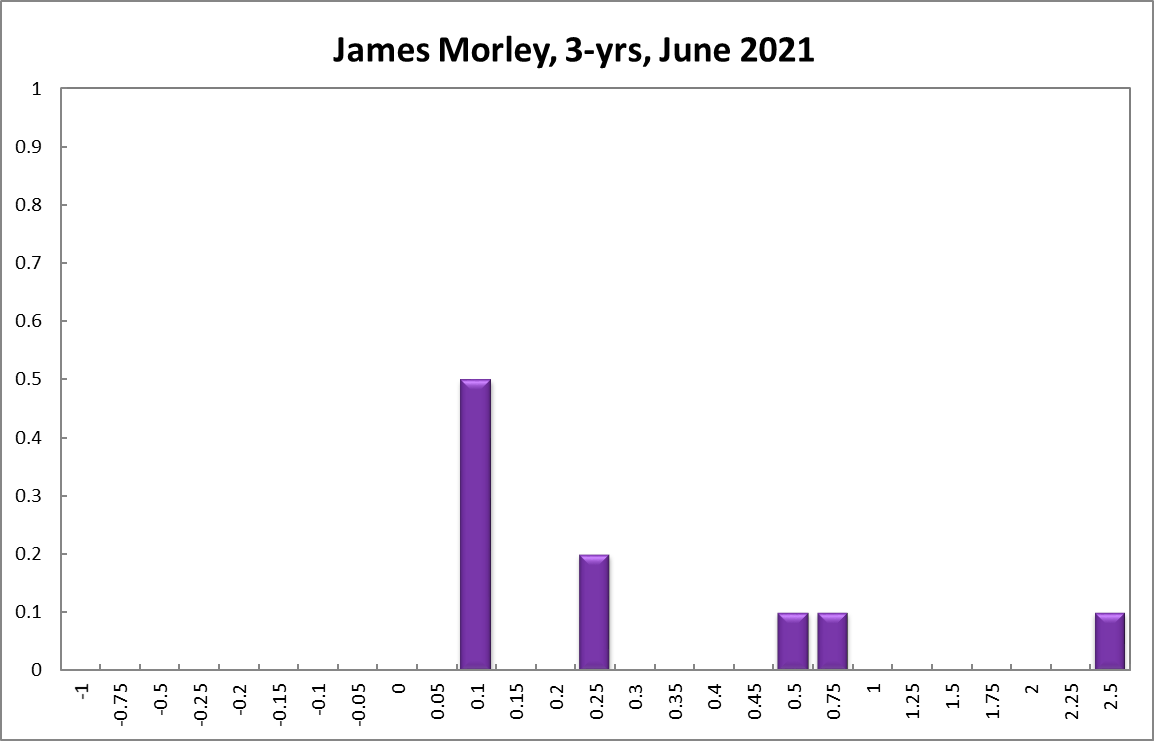

The RBA Board’s agreement at the May meeting to consider in the July meeting whether or not to retain the April 2024 bond as the target bond for 3-year yield-control target (hence suggesting when liftoff of the OCR might occur) or shift to the next maturity (the November 2024 bond, which would imply a six-month delay in liftoff for the OCR) is a welcome development. This provides a clear communication of how the yield-curve control measure could be adjusted in reaction to changes in expectations about future economic conditions. If the forecasts for inflation and inflation expectations move comfortably into the 2-3% target range by the July meeting, the RBA can signal liftoff could occur around April 2024. If they remain below, the RBA should move to the next bond issue and leave open the possibility of a further shift to a later maturity.

I suspect the forecasts for inflation will still not be strong enough by the July meeting and the discussion about which maturity to target will shift six months later. This is especially the case as “comfortably with the 2-3% target range” should be in the top half of the range to help partially offset the effects of the Covid crisis (and past misses of the target range) on the price level.

Updated: 4 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin