Aggregate

Rates Should Stay Steady But Downside Risks Rising

Australia’s inflation rate, at 1.6% (June quarter), remains well below the Reserve Bank of Australia’s official target range of 2-3%. The unemployment rate rose slightly to 5.3% in August, while real wage growth remains low at 0.7%. The RBA Shadow Board’s conviction that the cash rate should remain at the historically low rate of 1% has fallen from 71% to 65%, while the confidence in a required rate cut has increased from 14% to 24% and the confidence in a required rate hike has fallen from 14% to 11%.

Based on ABS figures for August, the seasonally adjusted unemployment rate in Australia ticked up to 5.3%. The labour force participation rate also edged up to 66.2%. Total employment rose by nearly 35,000 but there was a drop in full time employment of more than 15,000. There were no new data on wages growth.

The Aussie dollar, relative to the US dollar, found support near the 67 US¢ mark. Yields on Australian 10-year government bonds, after reaching all-time historical lows of 0.89%, rebounded to around 1.00%, which is still exceptionally low. The inversion of the yield curve in short- and medium-term maturities (2-year versus 1-year and 5-year versus 2-year), often considered a portent of economic weakness, remains in place. The Australian share market rallied for much of September, reflecting the overall strength of global share markets; the S&P/ASX 200 stock index now trades near 6,700.

Australia’s current account posted a $5.85 billion surplus in the second quarter of this year. This was the first current account surplus since the second quarter of 1975, coming on the back of a soaring trade surplus in goods. The services balance remained in deficit but narrowed slightly. However, this is likely to be a once-off: the third quarter current account, to be announced in early December, is expected to be heavily in deficit, by $13 billion. This deficit will subtract from aggregate demand and add to the economy’s weakness.

The global economy continues to face the prospect of a downturn, a concern publicly expressed by the new IMF head Kristalina Georgieva. In a recent statement the economist admitted she was taking on her new role at a time of faltering economic growth, trade tensions and historically high debt levels. She also pointed out that the IMF’s long-term objectives included “dealing with issues like inequalities, climate risks and rapid technological change.” China’s economic growth slowed to a near 30-year low of 6.2% in the second quarter of 2019. With a bloated state sector, ballooning debt and growing concerns about political instability, in part fuelled by the protests in Hong Kong, the near-term outlook does not point towards an improvement. In Europe, the uncertainty surrounding Brexit is likely contributing to a continued softening of the European economy. The sabre rattling between the US and Iran are likewise cause for concern.

Consumer confidence, as measured by the Melbourne Institute and Westpac Consumer Sentiment Index, softened slightly to 98.2% in September. Retail sales contracted slightly by 0.1% (month-on-month) in July, the last month for which data are available. Business confidence (NAB) fell while the manufacturing PMI increased in August from 51.3 to 53.1 and the services PMI rebounded from 43.9 to 51.4. The capacity utilisation rate also rebounded from 80.89% in July to 82.04% in August.

There are signs the housing market is at least temporarily recovering. While the house price index dropped by 0.7% quarter-on-quarter, this was less than expected and followed a 3.0% decline in the previous quarter. Clearance rates are also rising and the construction PMI increased from 39.1 to 44.6 in August. While a recovery of the housing market may help support consumer spending in the short term, which the Treasurer in a recent speech is clearly hoping for, this brings with it the significant risk of continued inflation of the housing bubble and a further rise in household indebtedness.

The Shadow Board now attaches a 65% probability that the overnight interest rate should remain at 1%, 6 percentage points less than in the previous month. It attaches a 24% probability that a rate cut, to 0.75%, is appropriate (up from 14%) and an unchanged 11% probability (down from 14%) that a rate rise, to 1.25% or higher, is appropriate.

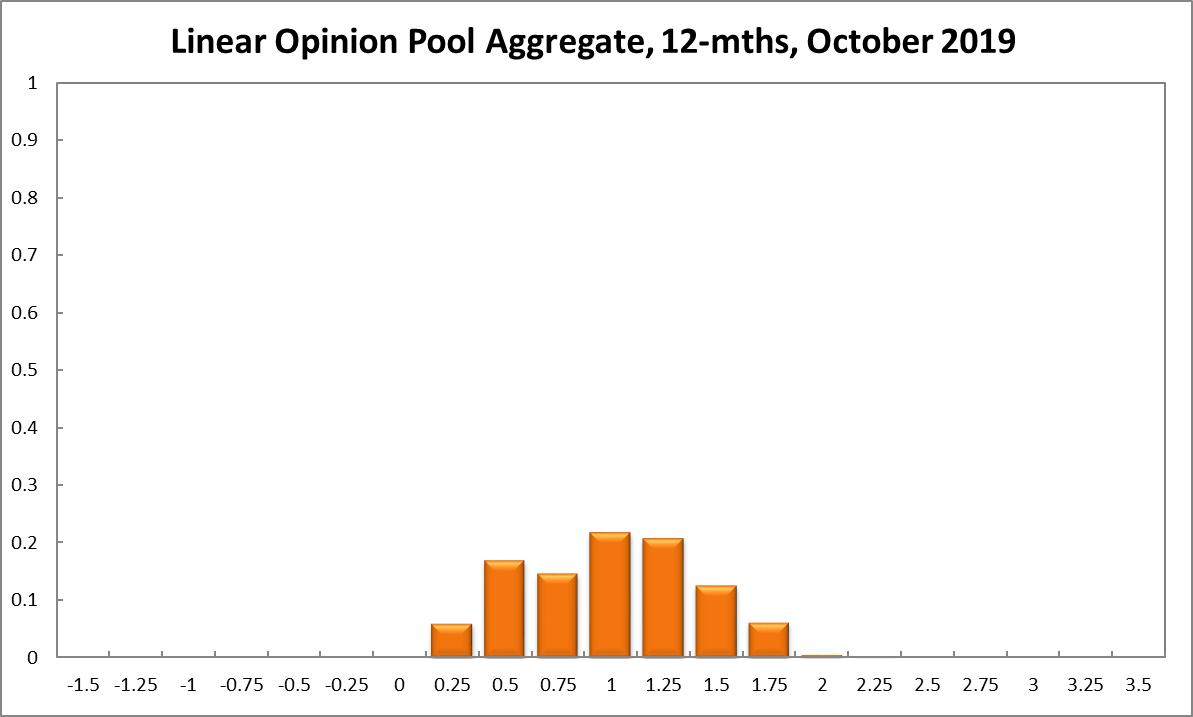

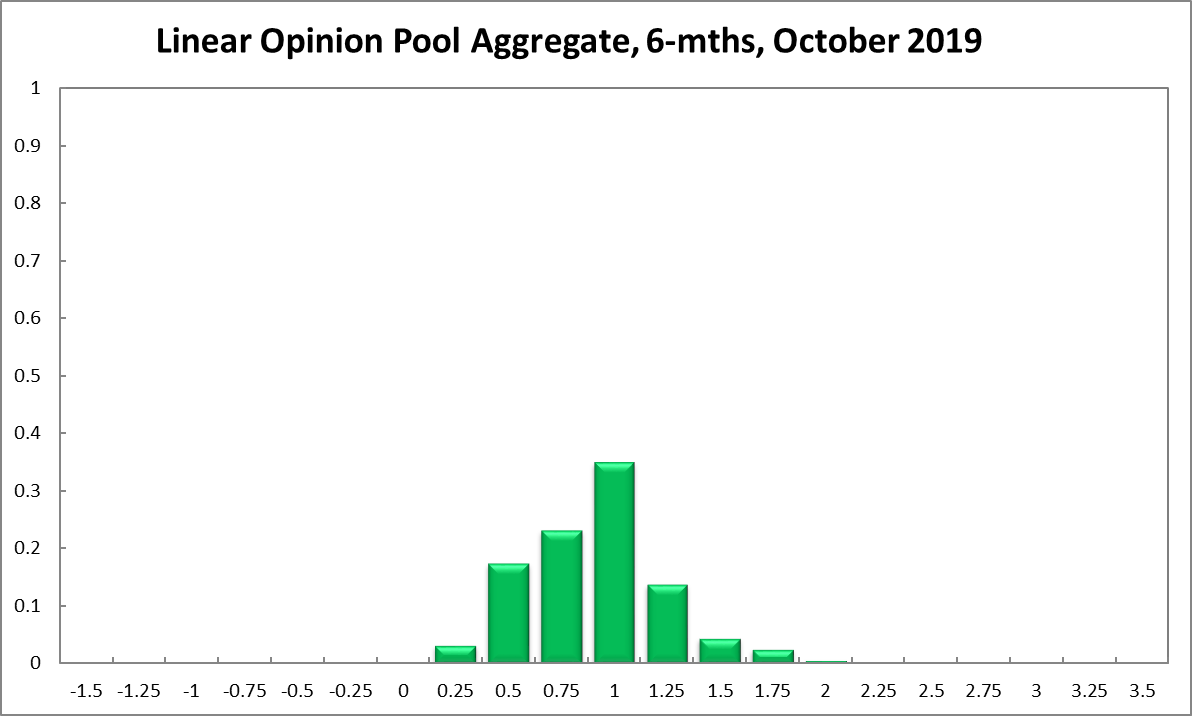

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 1% equals 35%, just one percentage point higher compared to the previous month. The probability attached to the appropriateness for an interest rate decrease stands at 44% (37% in September), while the probability attached to a required increase equals 21% (28% in September). The overall distribution for the recommendations a year out has again added probability mass to the left-hand side. The Shadow Board members’ confidence that the cash rate should be held steady equals 22% (unchanged), while the confidence in a required cash rate decrease equals 38% (32%) and in a required cash rate increase 41% (46%). The range of the probability distributions over the 6 month and 12 month horizons has remained constant, extending from 0.25% to 2.25%.

Updated: 27 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin