Aggregate

Steady Is the Word, Again

Former Bank of England Governor Sir Mervyn King famously wrote that, “a successful central bank should be boring”. The recent consensus in monetary policy, given the absence of major news about the Australian and overseas economies to inform policy makers, appears to be just that.

The unemployment rate, according to the latest ABS figures, fell to 5.8%, and inflation, at 1.7%, remains below the RBA’s target band of 2-3%. Economic growth came in at an annual 3.0 per cent at the end of 2015, fuelled by stronger household spending and government expenditure, while investment declined by 0.6 per cent in the fourth quarter, subtracting from GDP growth. Yet real domestic income increased by only 0.1 per cent in the fourth quarter, reflecting a decrease in Australia’s terms of trade.

Overall, the outlook for the Australian economy looks much the same as the previous month. The CAMA RBA Shadow Board’s policy preferences remain virtually unchanged from last month. It continues to have a strong preference for keeping the cash rate on hold, attaching a 69% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 23%, while the confidence in a required rate hike only equals 8%.

The fall in Australia’s unemployment rate can be almost entirely attributed to a fall in the participation rate from 65.1% to 64.9%. There has been no new data on real wage growth, which remains worryingly subdued.

The weakening of the US dollar has seen the Aussie dollar rebound to above 77 US¢. The trade balance remains firmly in deficit, equalling $2.9 billion in January (down from $3.5 billion in December 2015). Yields on Australian 10-year government bonds have inched up to 2.53%. The yield curve thus remains relatively flat.

Global stocks have rebounded spectacularly since the rout at the beginning of this year, while commodity prices have also gained some ground. Conversely, volatility, as measured by the VIX volatility index, has been declining steadily since its peak in early February. The last month has brought little in the way of news about the health of the world economy. The US economy still looks to be the pacemaker, with Europe, Japan, the BRICS countries and other developing economies expanding only modestly. High indebtedness in many countries remains a concern, even at historically low interest rates.

The Shadow Board’s confidence measures are virtually unchanged from the previous month. It attaches a 69% probability that “no change” is the appropriate policy, a 23% probability that rate cut is appropriate and an 8% probability that a rate rise, to 2.25% or higher, is appropriate.

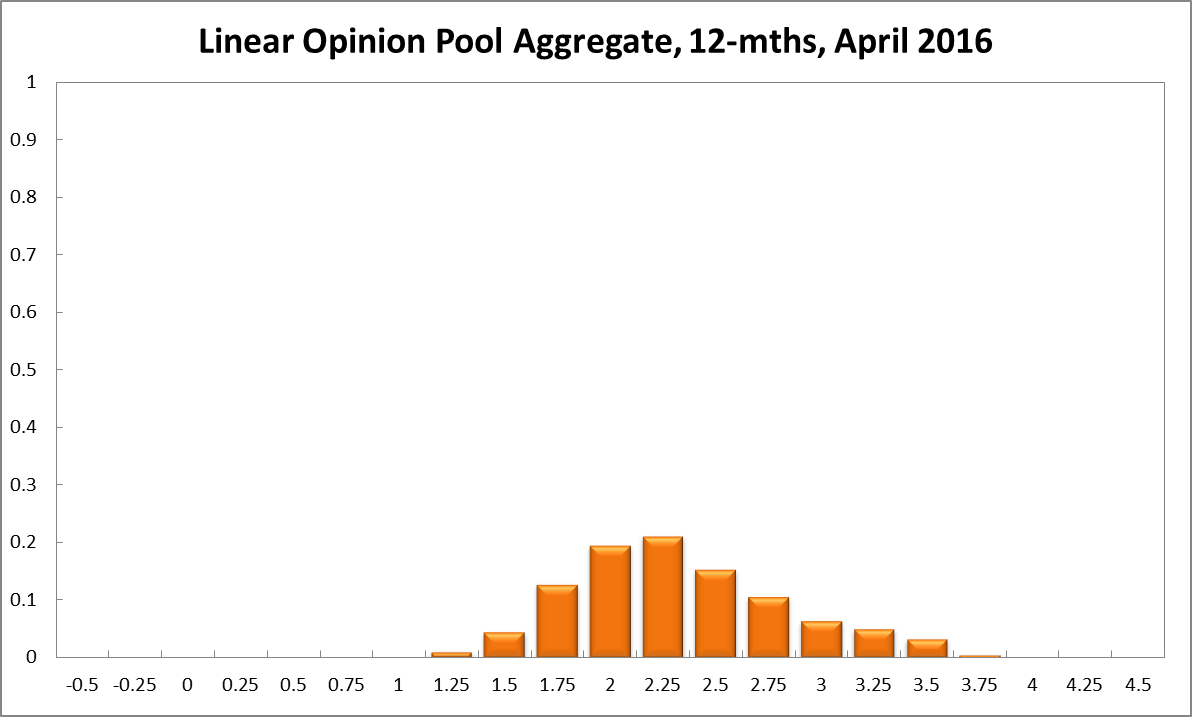

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2% remains at 30%. The estimated need for an interest rate decrease has risen to 25% (23% in March), while the need for a rate increase has fallen to 45% (47% in March). A year out, the Shadow Board members’ confidence that the cash rate should be held steady dropped three percentage points, from 22% to 19%, while the confidence in a required cash rate decrease equals 18% (16% in March) and in a required cash rate increase 62% (63% in March).

Updated: 17 August 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin