Aggregate

Turmoil in Global Markets Causing Headaches But Rate Hold Still Best Policy

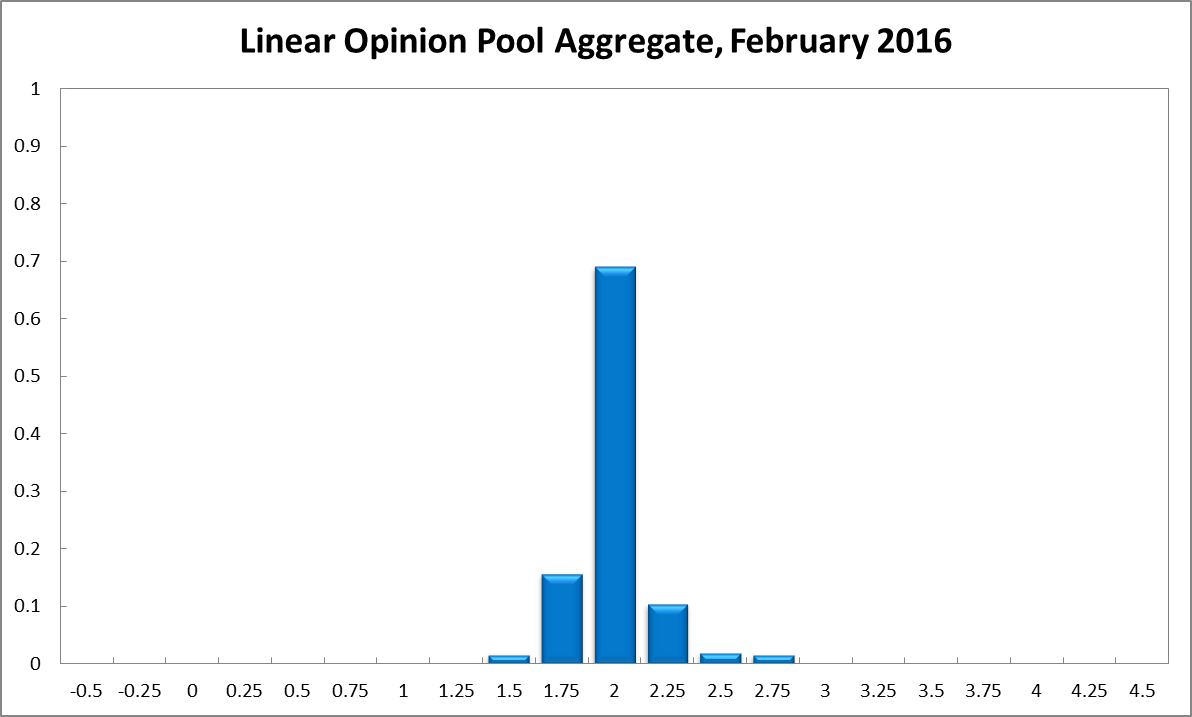

It has been an awful start to the new year for people invested in shares. Global stock markets have seen falls of more than 15% in places, as investors worry about slow growth in China and over-indebtedness in emerging markets. Losses on the Australian share market are more modest but the Australian dollar has been caught in the maelstrom, temporarily trading as low as 69 US¢. Unemployment is steady, while inflation in the December quarter edged up to 1.7%, from 1.5% in the previous quarter, and thus remains below the RBA’s target band of 2-3%. Latest figures estimate GDP growth at 2.5% annualized, a slight improvement over the previous quarter. The CAMA RBA Shadow Board on balance prefers to keep the cash rate on hold, attaching a 69% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 17%, down five percentage points from the previous month, while the confidence in a required rate hike has risen to 14%.

Australia’s unemployment, according to the Australian Bureau of Statistics, is steady at 5.8%. Employment has barely budged, though there has been an increase in full-time employment accompanied by an offsetting decrease in part-time employment. Even though the participation rate is down to 65.1%, the labour market, at least for moment, appears robust.

After pausing around the 72 US¢ for some time, the Aussie dollar has depreciated further, briefly falling to as low as 69 US¢. It now trades above 70 US¢ again. A further weakening of the international and domestic economies may see the Aussie dollar decline further. Yields on Australian 10-year government bonds have fallen again, most recently to 2.69%, pointing to weakness in the Australian economy.

Globally, the economic outlook is weakening. Even though the US Federal Reserve raised the federal funds rate during its last FOMC meeting of 2015, the rest of the world is teetering. Global share markets, led by China, suffered big losses in the opening weeks of the new year. Increasingly cracks are showing in emerging market economies, following excessive debt levels and plummeting commodity prices. Consequently, an estimated $740 billion (net) flowed out of emerging markets in 2015, most of it leaving China. Further capital flight is likely, and there is a genuine risk that some countries and some financial institutions will be in serious financial difficulties. Overall, global growth is likely to be sluggish, a view shared by the International Monetary Fund, which recently dropped its growth forecast for the world in 2016 from 3.6% to 3.4%.

Consumer and producer sentiment measures are pointing South. The Westpac/Melbourne Institute Consumer Sentiment Index fell from 101 in December 2015 to 97.3 in January. Business confidence, according to the NAB business survey, after a brief blip up, fell again from 5 to 3. The AIG manufacturing and services indices, leading economic indicators, both fell.

The Shadow Board’s confidence that the cash rate should remain at its current level increased marginally, from 67% in December to 69%. The confidence that a rate cut is appropriate has dropped for the second time in a row and now equals 17% (22% in December); the confidence that a rate increase, to 2.25% or higher, is necessary has risen to 14% (11% in December).

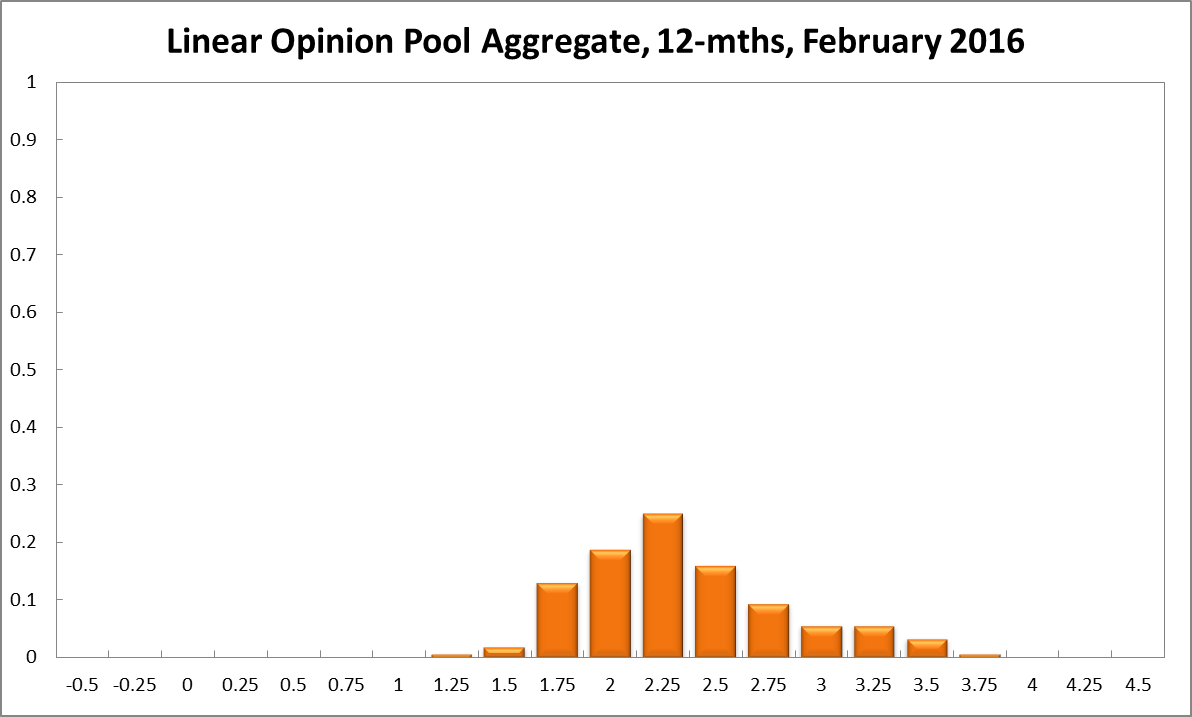

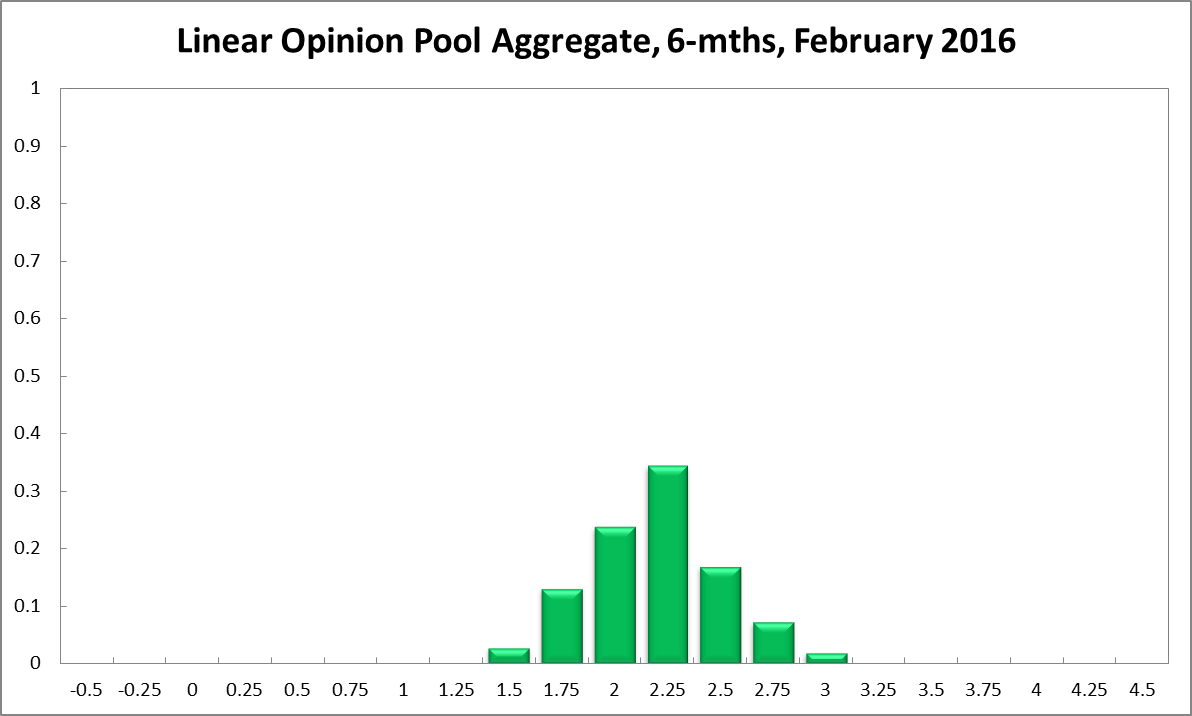

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2% is nearly unchanged at 24% (23% in December). The estimated need for an interest rate increase is unchanged at 60%, while the need for a rate decrease has slipped to 16% (17% in December). A year out, the Shadow Board members’ confidence that the cash rate should be held steady edged up a percentage point, from 18% to 19%, while the confidence in a required cash rate increase equals 66% (67% in December) and in a required cash rate decrease 16% (unchanged from December).

John Romalis did not vote this round.

Updated: 18 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin