Aggregate

Weakening Trade, Volatile Markets Spell Trouble: RBA Shadow Board Recommends Keeping Cash Rate Steady

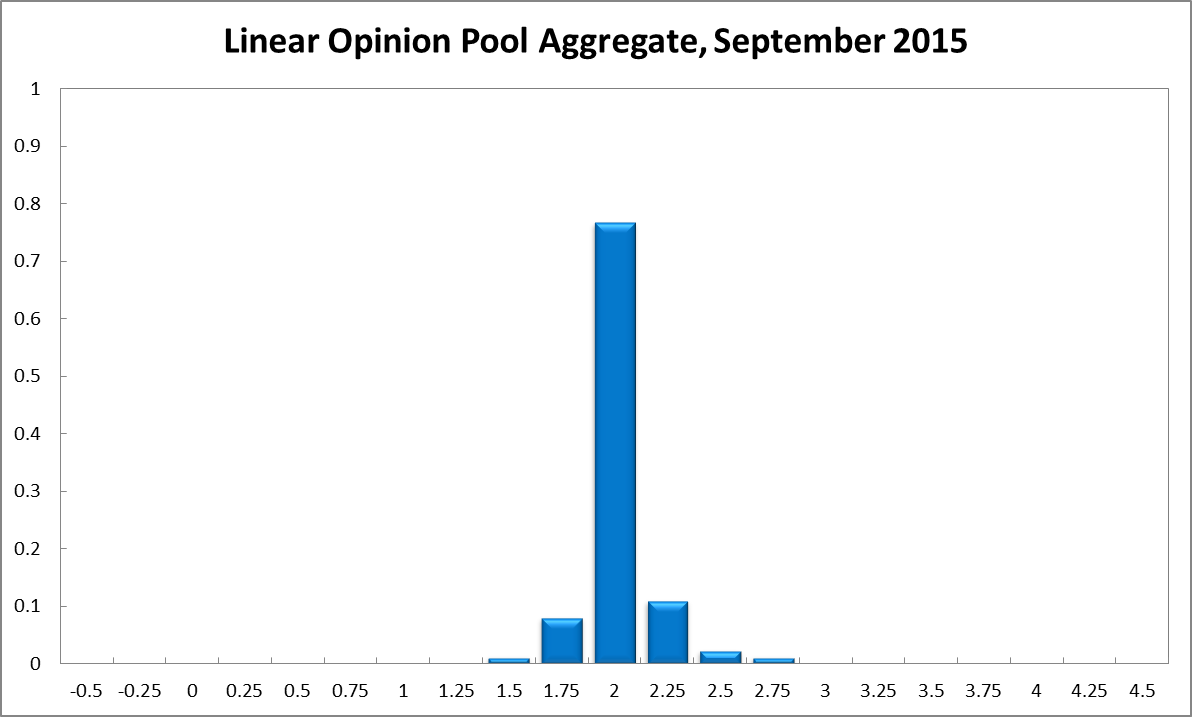

Wild swings in global stock markets have made investors edgy, the economic news coming out of China is not favourable and domestic private investment has plummeted. On the other hand, US growth surged to 3.7% annually and fears of a debt crisis in the Euro zone have abated. Latest estimates still put inflation at 1.5%, below the RBA’s target band of 2-3%. The CAMA RBA Shadow Board on balance prefers to keep the cash rate on hold, attaching a 77% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 9%, up 3% from the previous month, while the confidence in a required rate hike has fallen to 14%.

Latest figures show that Australia’s unemployment rate increased to 6.3% in July, according to the Australian Bureau of Statistics, even though total employment rose by nearly 40,000 in July. Nominal wage growth remains muted at 2.3% and is forecast to remain low in the next quarter.

The Aussie dollar depreciated further against major currencies. It now fetches less than 72 US¢. Yields on Australian 10-year government bonds remain low at 2.71%.

As already pointed out in last month’s statement, the Australian property market appears to be cooling and the local stock market is retreating further from its highs earlier this year. The elephant about to enter the room is the dramatic fall in new private capital expenditure, equalling a sizable 4.0% in the June quarter, bringing the annual decline to 10.5%, the largest drop since the last recession in 1992. The large drop is largely attributable to the contraction of the mining sector; however, firms in other sectors are also planning to cut spending, posing a serious threat to the Australian economy.

The recent gyrations in worldwide stock markets have highlighted the frothiness in global asset prices. To what extent volatility and uncertainty in asset markets spills over into the real economy is, of course, unclear. However, few economists doubt that asset markets are relying on ultra-low interest rates to persist. Concerns about any debt crisis in the Euro zone have waned since the recent 80 billion Euro credit extended to Greece. As in previous months, the deteriorating outlook for the Chinese economy pose the biggest immediate threat to Australia’s export markets and thus to Australia’s GDP. US growth, on the other hand, has been revised up to 3.7% (annualized) for the second quarter 2015, presenting a dilemma for the Federal Reserve Bank: the strong economic performance suggests an increase in the federal funds rate is around the corner but if volatility in stock markets persists, signalling heightened uncertainty about the future, the Fed may be tempted to postpone the interest rate increase. Commodity prices have continued to fall, with crude oil dipping below $40 a barrel.

Also of concern is the sizable contraction of world trade in the first half of this year. The volume of global trade shrank by 0.5% in the June quarter, while the figures for the March quarter were revised to a 1.5% contraction, indicating that world trade recorded its largest contraction since the 2008 global financial crisis.

Consumer and producer sentiment measures paint a motley picture. The Westpac/Melbourne Institute Consumer Sentiment Index jumped from 92.3 in July to 99.5 in August. Business confidence, according to the NAB business survey slumped from 10 in July to 4 in August, at the same time as the AIG manufacturing and services indices, both considered leading economic indicators, recorded notable improvements.

The Shadow Board’s confidence that the cash rate should remain at its current level of 2% equals 77% (up from 68% in August). The confidence that a rate cut is appropriate has edged up three percentage points, to 9%; conversely, the confidence that a rate increase, to 2.25% or higher, is called for has decreased considerably for the third time in a row, from 35% in July and 25% in August to 14%.

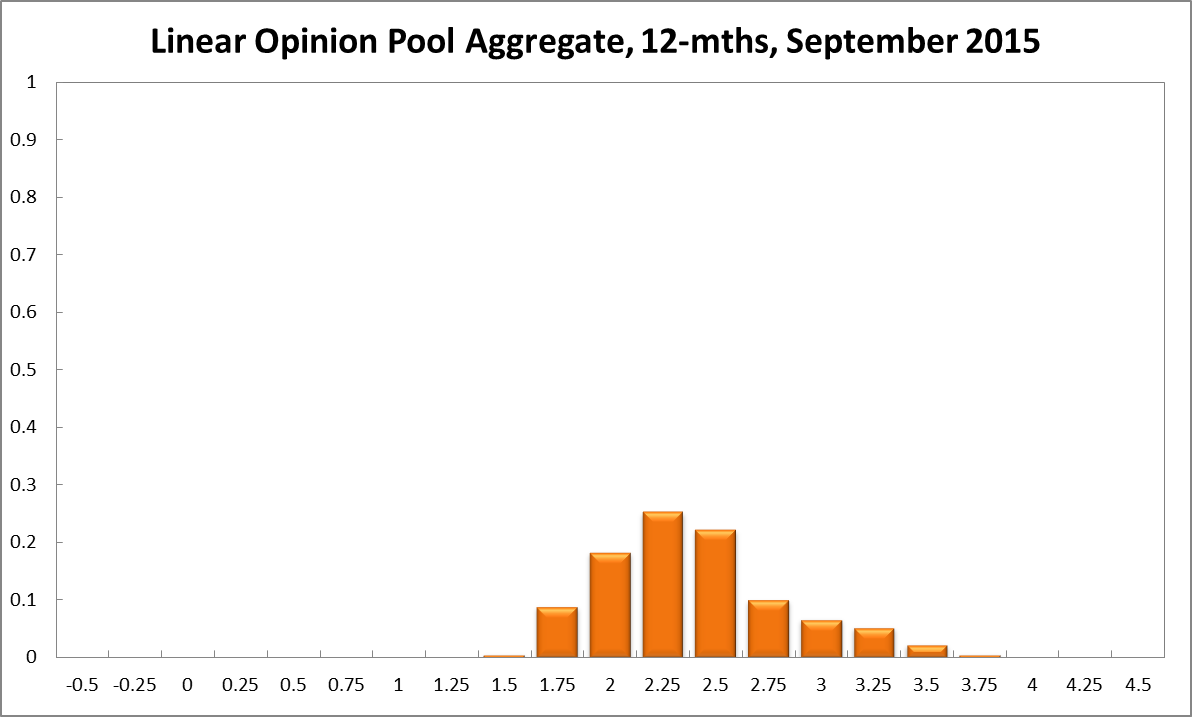

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2% equals 27% (23% in August). The estimated need for an interest rate increase lies at 65% (73% in August), while the need for a rate decrease is estimated at 8% (4% in August). A year out, the Shadow Board members’ confidence in a required cash rate increase equals 72% (six percentage down from August), in a required cash rate decrease 9% (7% in August) and in a required hold of the cash rate 18% (up from 15% in August).

Updated: 22 November 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin