Aggregate

Interest Rate Should Fall No Further RBA Shadow Board Recommends

The RBA’s most recent cut of the cash rate, to 2%, went against the recommendation of the CAMA RBA Shadow Board. Since then economic data continues to show signs of weakness. Unemployment is up slightly, investment down, and consumer and business confidence remain fragile. The international economy continues to pose a threat to the Australian economy and inflation remains comfortably within the RBA’s target band. But asset prices, Sydney house prices in particular, continue to post high gains. The CAMA RBA Shadow Board on balance prefers to hold firm but believes the cash rate has bottomed and an increase is due in the near future. In particular, the Shadow Board recommends the cash rate be held at its current level of 2%; it attaches a 60% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals a mere 2%, while the confidence in a required rate hike stands at 38%.

Australia’s jobless rate, according to the Australian Bureau of Statistics, edged up to 6.2% in April. Worryingly, in the same month full-time employment, total employment and the participation rate have fallen. Wage growth remains at a record low: the Australian wage price index increased by 2.3% in the last quarter, well below the average of 3.5% for the period 1998-2015.

The Aussie dollar remains range bound between 76 US¢ and 80 US¢. Yields on Australian 10-year government bonds have increased further, to 2.84%, from its recent low of 2.59%, implying a steepening of the yield curve, normally a bullish sign.

Regional housing markets, particularly Sydney and Melbourne, and domestic share prices remain buoyant. This remains a primary concern for many Shadow Board members as the asset price increases coincide with an increase in private sector leverage, leading to misallocated investment and opening up the possibility of a costly price correction. According to the Reserve Bank of Australia total housing credit grew by 7.2% (year-ended) in April 2015, compared to 6% in April 2014.

The international economy remains subdued. For Europe a noticeable pickup in growth is not on the horizon, at least not until the Greek debt crisis is resolved. Recent revisions of US data indicate that US growth this year has been slower than initially thought, with some analysts suggesting the US economy actually contracted in the first quarter. Without a string of good news about the US economy, the Federal Reserve Bank’s increase of the cash rate is likely to be pushed back ever more. Commodity prices are likely to remain soft and possibly fall further.

Consumer and producer confidence measures continue to be mixed. However, of particular concern is the outlook for domestic investment. The ABS survey of chief financial officers conducted in April and May of this year reveals that total capital expenditure is still expected to fall significantly, with the current estimate for fiscal year 2015-16 being 24% less than the corresponding estimate for fiscal year 2014-15. The trend volume estimate for total new capital expenditure fell 2.3% in the March quarter 2015 while the seasonally adjusted estimate fell 4.4%.

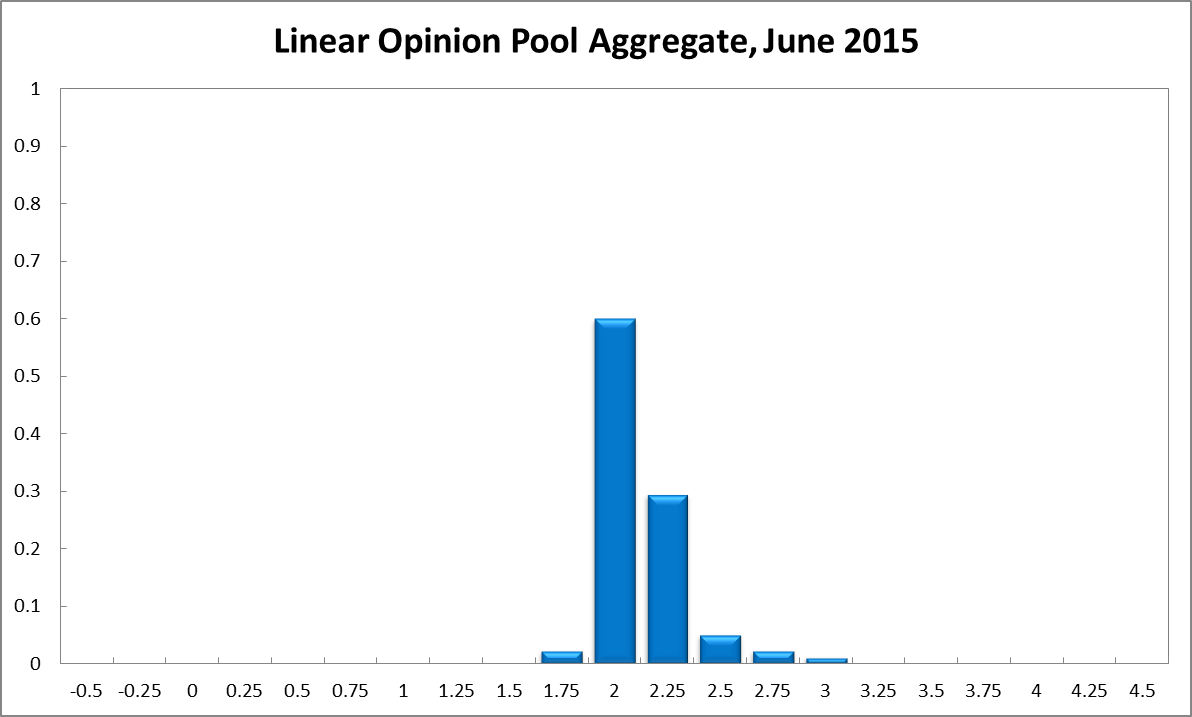

The Shadow Board’s confidence that the cash rate should remain at its current level of 2% equals 60%. The confidence that a rate cut is appropriate is a mere 2%, whereas the Shadow Board considers it much more likely (38%) that a rate increase, to 2.25% or higher, is the appropriate policy decision for this month.

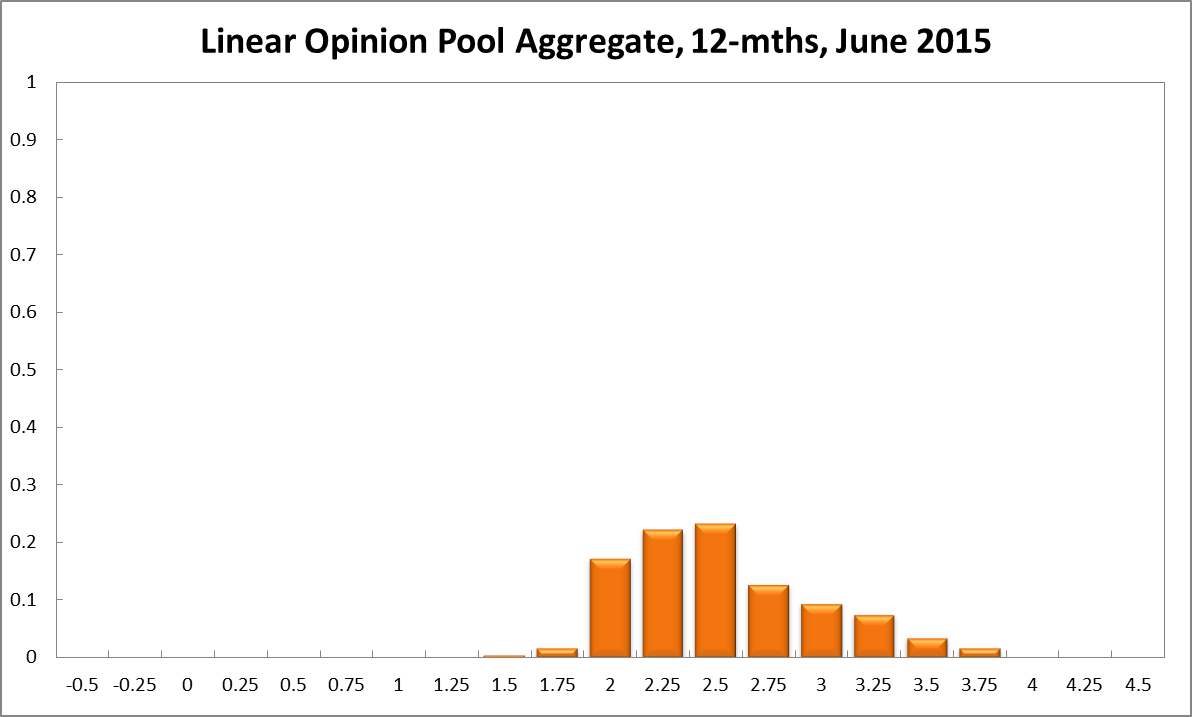

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2% equals 23%. The estimated need for an interest rate increase lies at 76%, while the need for a rate decrease is estimated at 3%. A year out, the Shadow Board members’ confidence in a required cash rate increase equals 81%, in a required cash rate decrease 2% and in a required hold of the cash rate 17%.

Updated: 18 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin