Aggregate

Economic Outlook in Australia Remains Murky

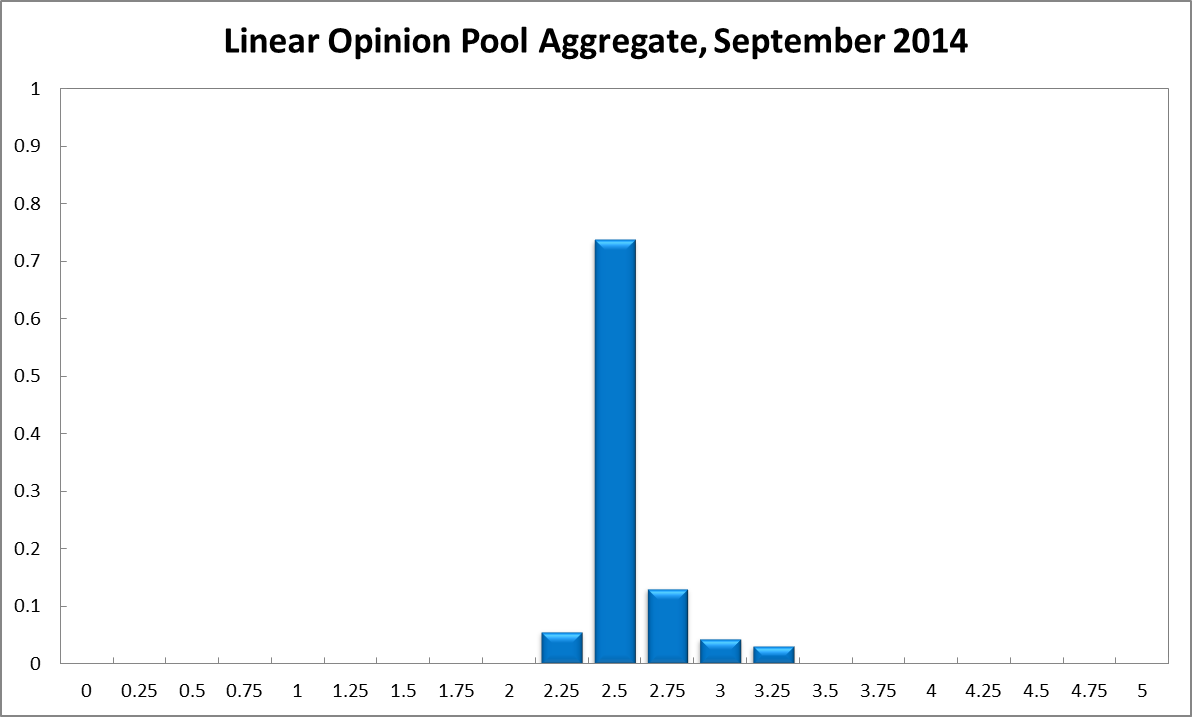

The picture of the Australian economy painted by the latest data is murky. The housing market and indicators of sentiment are strengthening but growth remains slightly below trend and the unemployment rate rose to 6.4% in July. Relative to the previous month, the CAMA RBA Shadow Board has become slightly more cautious in its recommendations for interest rates. The Board attaches a 74% probability that the cash rate ought to remain at 2.5% in September. The confidence attached to a required rate cut equals 6%, while the confidence in a required rate hike has dropped to 21%.

Australia’s unemployment rate increased 0.3 percentage points to 6.4% in July 2014, a 12-year high. This rise is largely attributed to an increase in the participation rate - the number of persons in the labour force swelled by 43,000, while total employment fell slightly. Policy makers will be keeping a close eye on the developments in the labour market, in particular whether the additional job seekers are going to succeed in finding employment in the near future.

There is no new inflation data available to guide this month’s policy decision, with headline inflation officially still hugging the top of the 2-3% target band. Business indicators are looking up, with the NAB Business Confidence, the Manufacturing PMI, the Australian PSI, and the capacity utilization rate all improving in the last month. GDP growth is estimated to lie just below trend. The construction industry is responding positively to the housing boom, picking up some of the economic slack left behind from the slowdown in mining investment but, among the Board members, concerns about inflated asset prices, particularly house prices in Sydney and Melbourne, remain.

Worldwide foreign exchange markets are characterized by exceptionally low volatility. The Australian dollar has moved very little in the past few months, still buying around 93 US cents. There is still some uncertainty about the federal government’s budget and the government’s ability to navigate the Senate remains.

Mixed news also characterized the global economy. The US economy looks more solid, with recent second quarter GDP growth revised up to 4.2% (annualized). The Federal Reserve’s hints of future tightening of US monetary policy is likely to weaken the Australian dollar and may provide greater scope for a rate domestic rate increase. News of the Chinese real estate markets is providing further evidence of considerable excess supply with house prices in some cities, especially at the luxury end, falling considerably. Europe’s recovery is faltering and, most worryingly, there are signs of Germany’s economy slowing significantly. The major geopolitical conflicts (Syria, Ukraine, Middle East) are unlikely to be resolved any time soon.

The consensus to keep the cash rate at its current level of 2.5% has strengthened to 74% (up 3 percentage points from August). The probability attached to a required rate cut equals 6% (5% in August) while the probability of a required rate hike has fallen again to 21% (24% in August).

The probabilities at longer horizons are as follows: 6 months out, the probability that the cash rate should remain at 2.5% edged up two percentage points to 49%. The estimated need for an interest rate increase equals 42% (45% in August), while the need for a decrease equals 9% (8% in August). A year out, the Shadow Board members’ confidence in a required cash rate increase slipped 4 percentage points to 61%, the need for a decrease ticked up to 10%, while the probability for a rate hold strengthened slightly to 29% (26% in August).

Note: John Romalis, Professor of Economics at the University of Sydney, has been appointed on the CAMA RBA Shadow Board, replacing Saul Eslake.

Updated: 18 July 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin