Aggregate

Divergence Between Financial Markets and the Real Economy Widens

Two months have passed since the CAMA RBA Shadow Board’s last interest rate setting and the uncertainties surrounding the domestic and foreign economies are not abating. Globally, asset markets are performing well but GDP growth remains subdued, pointing to a disparity that must be resolved eventually.

The picture for the Australian economy has not changed much since December. Inflation is well within the 2-3% target range, investment and consumption remain tepid. The economy is supported by historically low interest rates and an Aussie dollar that is now hovering around 87 US cents, a 21% fall from its recent peak. This expansionary policy setting is generating early signs of improvements in retail sales, building approvals and local business conditions.

Overseas, the picture continues to be characterized by uncertainty. While growth in US output has accelerated to an annualized rate of 3.2%, underscoring the Federal Reserve’s decision to scale down its asset purchases, the rest of the World is looking less promising. Europe will probably continue to show tepid growth as long as the debt overhang and structural problems are not fully addressed and China will likely settle on a lower growth trajectory, with the possibility of a more damaging credit crisis persisting.

Surprisingly, asset markets, domestically and overseas, have experienced double digit gains in 2013, fuelled by cheap credit and possibly excessive optimism. This divergence between the real economies and asset prices will ultimately need to narrow, either because global economic growth picks up significantly, validating the large increases in asset prices, or because asset prices will fall to more realistic levels.

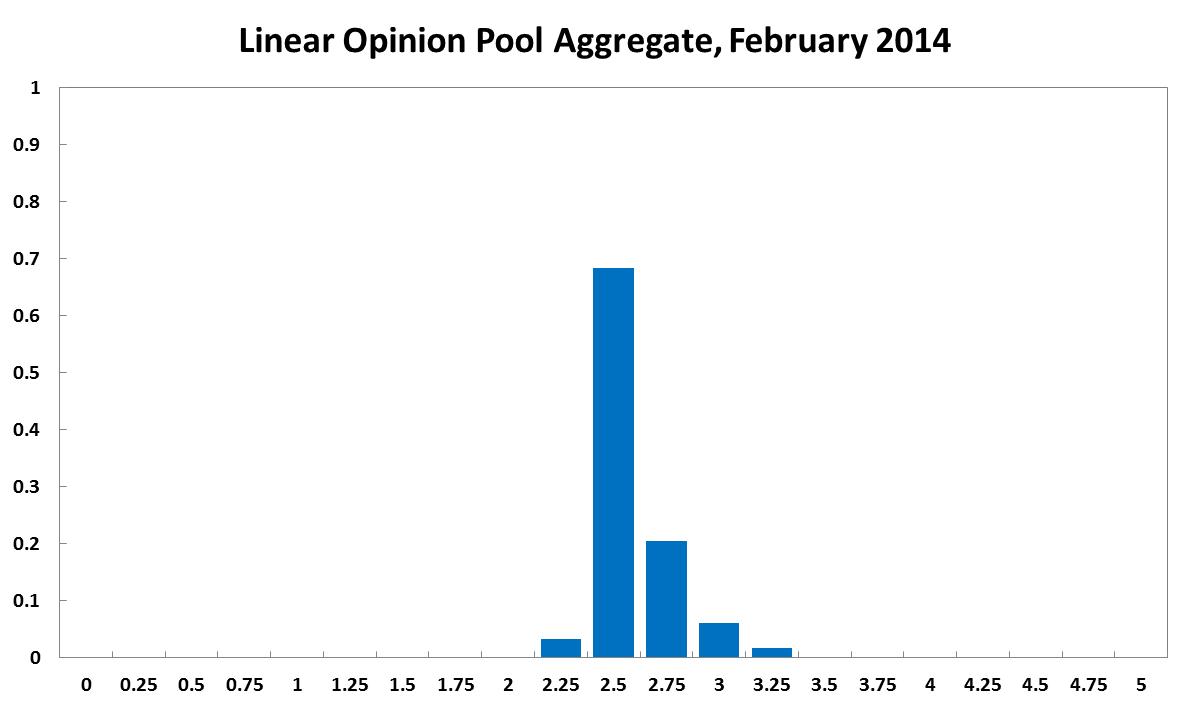

Without a clear direction of where the Australian economy is heading, the consensus to keep the cash rate at its current level of 2.5% remains strong. The Shadow Board’s confidence in keeping the cash rate steady rose to 68% (up from 63% in December 2013). The probability attached to a required rate cut now equals 3% (7% in December) while the probability of a required rate hike equals 28% (30% in December).

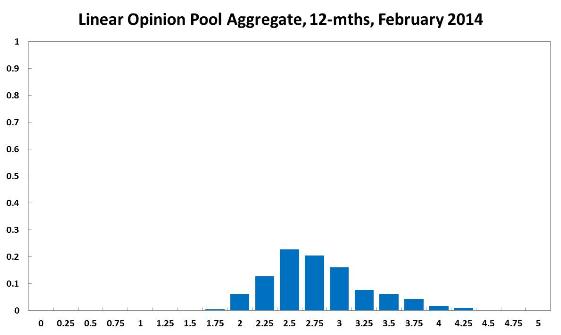

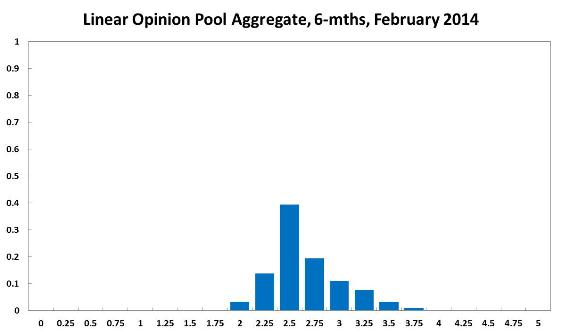

The probabilities at longer horizons are as follows: 6 months out, the probability that the cash rate should remain at 2.5% has increased to 39% (up from 34% in December 2013). The estimated need for an interest rate increase fell three percentage points to 44%, while the need for a decrease has nudged down to 17% (18% in December). A year out, the Shadow Board members’ confidence in a required cash rate equals 58% (59% in November), the need for a decrease has fallen further to 19% (21% in December), while the probability for a rate hold is given by 23% (up from 20% in December).

Updated: 21 November 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin