Aggregate

RBA Shadow Board Recommends Keeping Overnight Rate at 4.35% Going Into 2025

Australia’s monthly Consumer Price Index rose 2.1% in the 12 months to October, the most significant price rises affecting food and non-alcoholic beverages (+3.3%), recreation and culture (+4.3%) and alcohol and tobacco (+6.0%). This reading puts inflation comfortably in the Reserve Bank of Australia’s official target range of 2-3%. However, the most recent estimate of the RBA’s trimmed mean CPI, a more reliable indicator of underlying inflation, increased by 3.5% year-on-year in Q3 2024, above the 2-3% target range. The labour market remains pretty resilient overall, while consumer and business sentiment, on balance, took a turn for the better. The outlook for the global economy remains highly uncertain, which has not prevented stock markets from posting record highs, however. The Shadow Board’s stance has remained very steady in the past few months and so its recommendation is only marginally different from the last round: it attaches a 55% probability that holding the overnight rate steady at 4.35% is the optimal policy setting and only a 11% probability that a decrease to 4.1% might be the correct setting.

The seasonally adjusted unemployment rate remained at 4.1% in October 2024, as total employment rose by just under 16,000. The labour force participation rate edged down to 67.1%, while the underemployment rate eased to 6.2%. Monthly hours worked increased slightly, up 0.1% to 1,972 million. However, job advertisements fell by 1.3% in November. The Wage Price Index increased by 3.5% in Q3 2024, suggesting moderate wage pressures amid a tight labour market. The Reserve Bank likely welcomes a boost to households’ real wages, which have taken a significant hit over the past four years, yet sustained growth at the current clip could raise concerns about inflation expectations settling at a level above the official inflation target range.

The Australian dollar has weakened since the last interest rate decision, dipping below 64 US¢. The yield on Australian 10-year government bonds stands at 4.29%, reflecting a downward revision of growth and inflation forecasts by central banks and a reduction of expectations for central bank policy rates by market participants. The short-term yield curve (2y vs 1y) has turned slightly inverted, with a spread of -22.8 bps, while the medium-term yield curve (5y vs 2y) remains flat at 1.2 bps. The long-term yield curve (10y vs 2y) shows “normal convexity,” with a spread of 38.0 bps. Meanwhile, the Australian stock market surged to a new all-time high, with the S&P/ASX 200 Index nearing the 8,500 mark.

Australian consumer confidence saw a notable boost in November 2024, with the Westpac-Melbourne Institute Consumer Sentiment Index climbing 5.3% to 94.6 points — its strongest reading this year, though still shy of the neutral benchmark of 100. On the retail front, sales posted a robust 3.4% year-on-year increase in October, accelerating from September’s 2.4% rise. Monthly retail sales also surprised on the upside, growing 0.6% and outpacing market forecasts of a 0.3% gain, hinting at resilient consumer spending despite persistent economic uncertainties. Meanwhile, housing credit expanded by 0.5% month-on-month in October, matching September’s pace but still well below its historical average of 0.91%, suggesting demand for housing is not going to subside, despite the recent monetary tightening.

Australia’s business sentiment took a sharp turn in November 2024, with the NAB Business Confidence Index falling to -3 from a near two-year high of 5 in October, reflecting widespread weakness across most industries except construction. The Judo Bank Australia Manufacturing PMI climbed to a six-month high of 49.4, inching closer to expansion territory, while the Services PMI edged down to 50.5, still signaling growth but at a slower pace. Capacity utilization slipped to 82.5% from 83.1% in September, pointing to some slack in the economy. Meanwhile, corporate bankruptcies surged to a record 1,364 in October, adding a cautionary note to the business outlook. On a more positive note, forward-looking indicators offered glimmers of hope: the Westpac-Melbourne Institute Leading Economic Index rose by 0.2% month-on-month in October after stagnating for six months, while its six-month annualized growth rate turned positive at 0.26%. The Composite Leading Indicator also ticked up to 100.41 points in November, moving above its long-run average. Total new capital expenditure rebounded by 1.1% quarter-on-quarter in Q3 2024, beating expectations of 0.9% and reversing the previous quarter’s 2.2% contraction. Altogether, the outlook remains mixed: while headwinds persist, signs of resilience in investment and forward-looking indicators suggest the economy still has room to maneuver.

The global economic landscape presents a complex tapestry of resilience and risk as 2024 concludes. The OECD projects global GDP growth to hold steady at 3.2% in 2024, inching up to 3.3% in 2025 and 2026. This stability is underpinned by easing inflation, which has bolstered real incomes. However, consumer confidence has yet to rebound to pre-pandemic levels in many regions. Geopolitical tensions, notably in the Middle East, have escalated, contributing to market volatility and record-high gold prices. Furthermore, the OECD cautions that rising protectionism could disrupt trade recovery, potentially hampering growth. Regionally, the U.S. economy demonstrates robust performance, with growth forecasts of 2.8% for 2024, supported by strong consumption and wage increases. In contrast, China’s growth is expected to decelerate to 4.6% in 2024, reflecting challenges in the property sector and subdued domestic demand. The eurozone faces modest growth prospects, with projections of 0.8% for 2024, as it grapples with energy price volatility and political uncertainties. Encouragingly, inflation is receding globally, creating space for central banks to consider easing monetary policies. The IMF notes that headline inflation is approaching central bank targets in many economies, paving the way for potential rate cuts. Nonetheless, the OECD advises caution, highlighting persistent inflation in services and advocating for a measured approach to monetary easing to maintain economic stability.

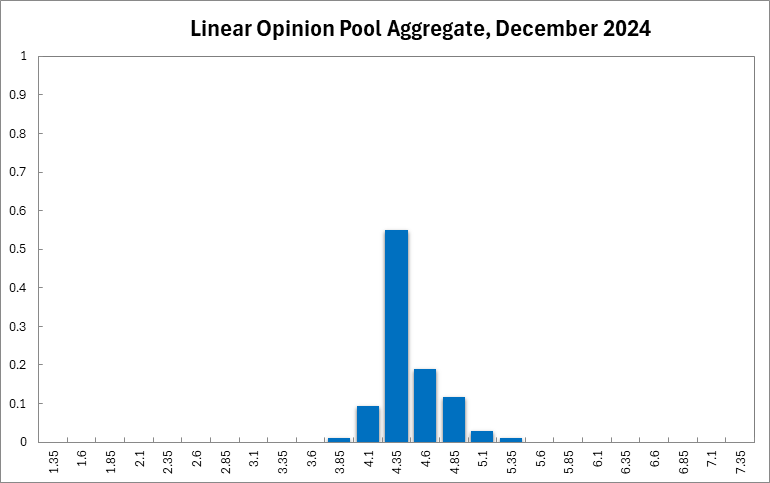

The Shadow Board’s conviction of keeping the overnight rate, currently equal to 4.35%, on hold strengthened marginally. The Board attaches a 55% probability that this is the appropriate setting (51% in previous round), a 34% probability (37%) that the overnight right should increase, to 4.6% or higher, and a 11% probability (12%) that the overnight right should decrease to 4.1% or lower.

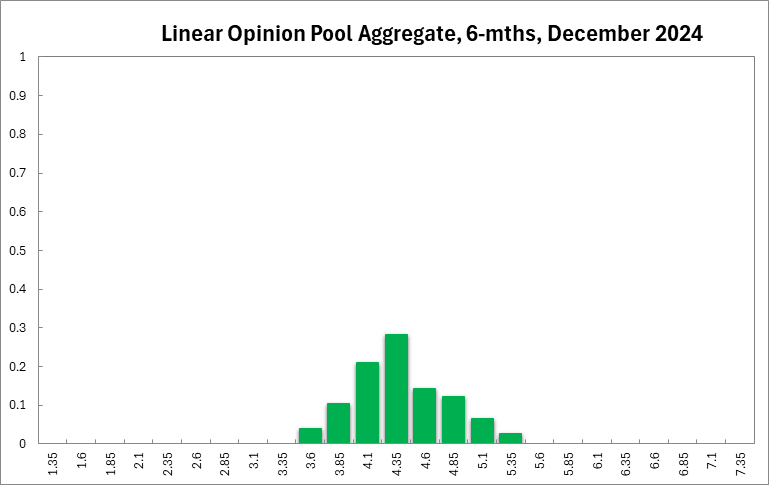

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at the current setting of 4.35% equals 28% (previously 27%); the probability attached to the appropriateness of an interest rate decrease equals 36% (38%), while the probability attached to a required increase equals an unchanged 36%.

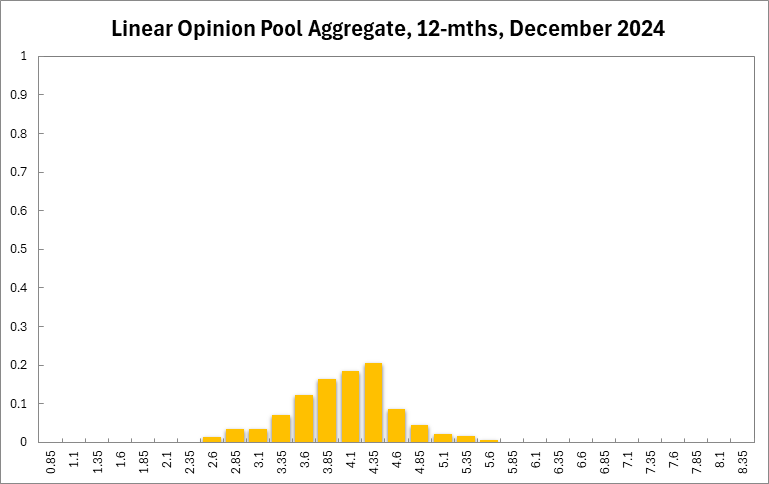

One year out, the Board’s recommendation continues to lean towards monetary easing but slightly less so than in previous rounds: members’ confidence that the appropriate cash rate should remain at the current level of 4.35%, equals 21% (17%), while the confidence in a required cash rate decrease, to below 4.35%, equals 62% (68%), and its confidence in a required cash rate increase, to above 4.35%, is 18% (15%). Three years out, the Shadow Board attaches an 14% probability that 4.35% is the appropriate setting for the overnight rate (previously 11%), an 78% probability that a lower overnight rate is optimal (80%) and an unchanged 8% probability that a rate higher than 4.35% is optimal (9%).

The ranges of the probability distributions have barely changed and are as follows: they extend from 3.85% to 5.35% for the current recommendation, from 3.60% to 5.35% for the 6-month horizon, from 2.60% to 5.60% for the 12-month horizon, and from 0.85%-5.35% for the 3-year horizon.

Updated: 23 December 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin