Aggregate

No Need for Melbourne Cup Rate Change: CAMA RBA Shadow Board

This month has been quiet again, with little economic news to help guide CAMA’s RBA Shadow Board. Employment numbers have again proved volatile, and business confidence rebounded somewhat, while consumer price inflation, at 1.0% year-on-year, remains well below the RBA’s 2-3% target band. The CAMA RBA Shadow Board clearly believes that the cash rate should remain at its current level. The Shadow Board attaches a 64% probability to a rate hold being the appropriate policy setting. The confidence attached to a required rate cut equals 4%, while the confidence in a required rate hike equals 32%.

Australia’s unemployment rate remains unchanged at 5.6%, according to the Australian Bureau of Statistics. The participation rate, again, fell slightly, from 64.7% to 64.5%. And, once again, a large increase in part time employment (43,186) was accompanied by a slightly larger decrease in full time employment (53,000). Data on nominal wage growth will be released in mid-November but the forecast is for a paltry 2%, year-on-year.

The Aussie dollar, relative to the US dollar, continues to be range bound between 75 US¢ and 77 US¢. After a long secular decline, yields on Australian 10-year government bonds have firmly rebounded, to 2.34%. Domestic share prices showed no clear direction in the month of October.

Global markets appear to be in a holding loop, waiting for the outcome for the US Presidential election, held on 8 November. The Federal Reserve Bank in the US, too, is putting off its decision to raise interest rates, in spite of recent favourable economic data. Crude oil prices, after last month’s surprise announcement by the Organization of the Petroleum Exporting Countries (OPEC) to modestly cut oil output, have stabilized around US$ 50. There has been no significant economic news from other regions.

Consumer confidence, as measured by the Westpac-Melbourne Institute Consumer Sentiment Index, is virtually unchanged from the previous month. The manufacturing and services PMI, which measure the performances of the manufacturing and services sectors, have rebounded slightly, from 46.9 to 49.8 and from 45 to 48.9, respectively. The AIG Performance of Construction Index (PCI) reversed its recent decline and rose from 46.6 in August to 51.4 in September, above the long-run average for the past 10 years. New numbers on building permits will be released on 2 November and, after the recent volatility in (the number of permits grew 12% in July and fell 1.8% in August), should provide a clearer picture of the state of the housing market.

The Shadow Board attaches a virtually unchanged probability of 64% (65% last month) that “no change” is the appropriate policy, a 4% probability (6% last month) that a rate cut is appropriate and a 32% probability (29% in the previous month) that a rate rise, to 1.75% or higher, is appropriate.

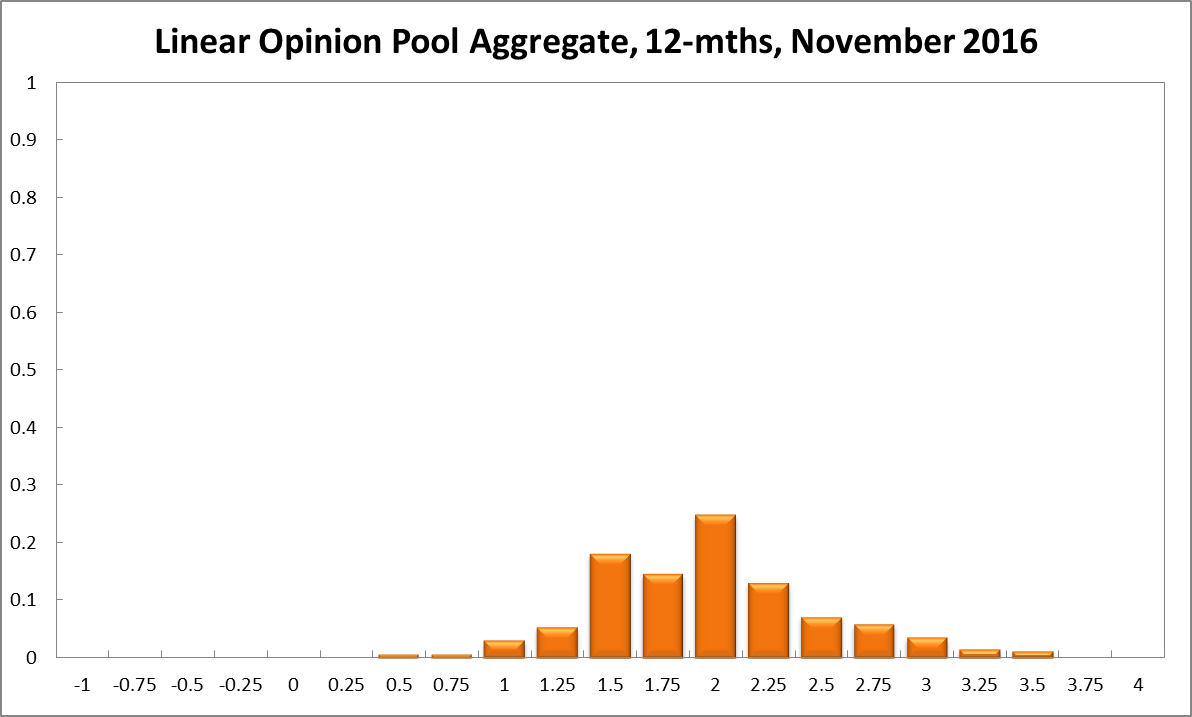

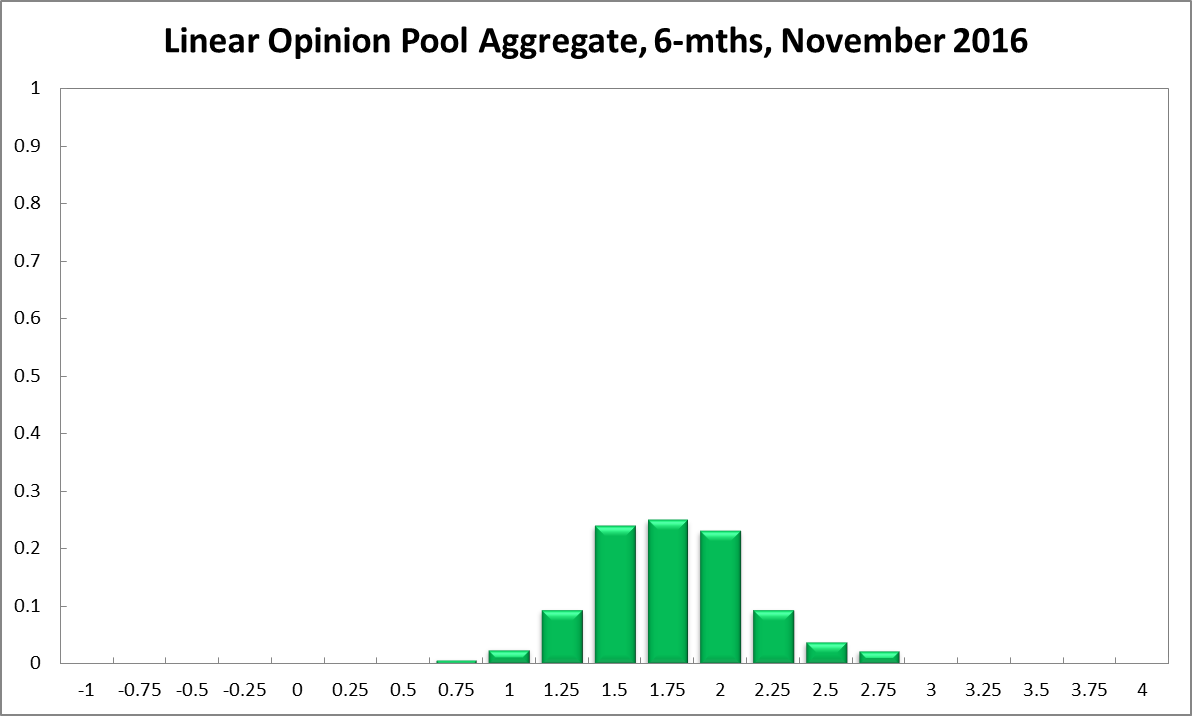

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 1.50% equals 24%, three percentage points down from the previous month. The estimated need for an interest rate decrease is unchanged at 13%, while the need for a rate increase equals 63% (61% in October). A year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 18% (16% in October), while the confidence in a required cash rate decrease is unchanged at 10% and the confidence in a required cash rate increase equals 72% (73% in October).

Updated: 14 May 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin