Aggregate

Strong Dollar, Low Inflation Allow Rates to Stay on Hold

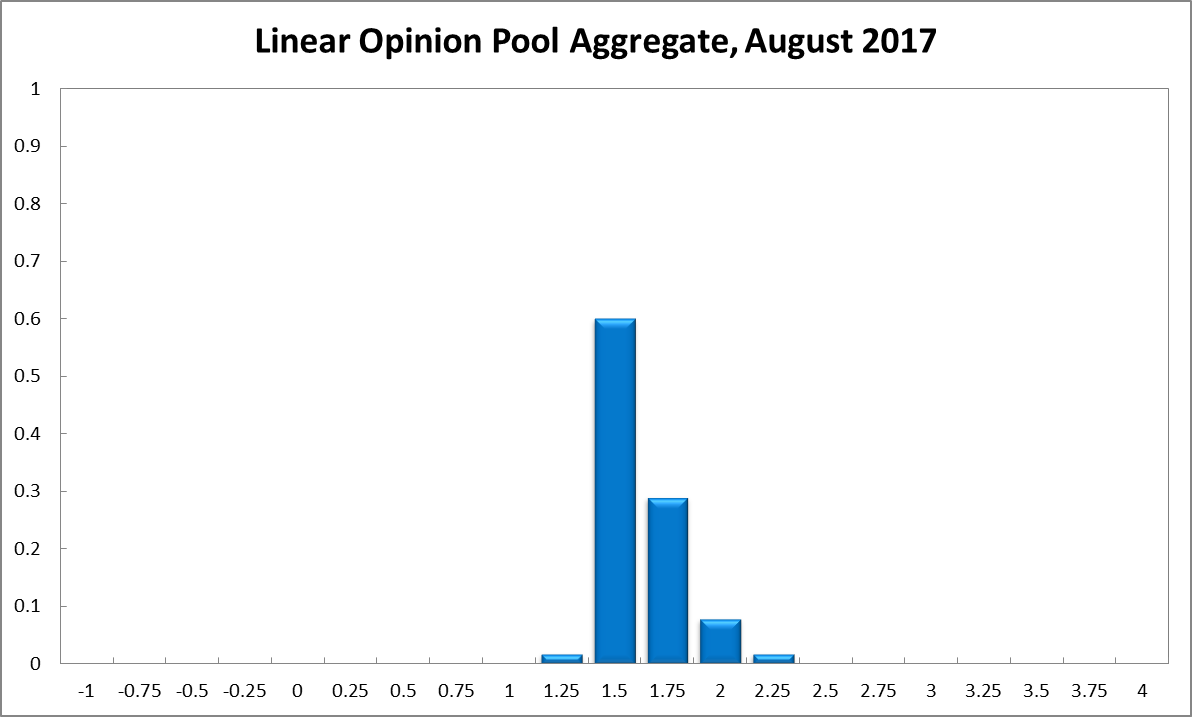

The unemployment rate is unchanged at 5.6%, while headline inflation fell slightly in the June quarter, from 2.1% to 1.9%, just below the Reserve Bank of Australia’s official target range of 2-3%. Consequently, the RBA Shadow Board continues to advocate a hold-and-wait policy. It attaches a 60% probability that this is the appropriate setting. The confidence attached to a required rate cut equals 2%, while the confidence in a required rate hike equals 38%.

By international standards, Australia’s seasonally adjusted unemployment rate, at 5.6%, according to the Australian Bureau of Statistics, remains relatively low. In June the economy added 62,000 full-time jobs. The labour force participation rate edged up further, to 65%, pointing to an overall improvement in economic health. However, the youth unemployment rate rose to above 13%, which is a worrying sign. And weak nominal wage growth of under 2% appears to be the new normal.

The Aussie dollar, relative to the US dollar, after falling the previous month, has continued its surprise appreciation, trading above 80 US¢ late this month. This helps keep a lid on inflation by lowering import prices and slowing aggregate demand. Yields on Australian 10-year government bonds edged up further and now equal approximately 2.68%. Domestic share prices continue to trade within a narrow range; the S&P/ASX 200 stock index’s last reading was 5703.

The international economy is not showing any new surprises. China is looking to de-lever slowly. The US economy is expanding, pointing to further tightening of US monetary policy. European growth is also looking solid though there are little signs that the European Central Bank is considering monetary tightening in the near future. Australia continues to post a trade surplus with the rest of the world but the current account remains in deficit.

Consumer and business confidence remain modest, the biggest improvement being recorded in the services PMI, which jumped from 51.5 to 54.8 index points in June. Capacity utilization dropped to under 82%. Retail sales picked up to more than 3%, year-on-year. The AIG/Housing Industry Association Performance of Construction Index remains near its ten-year high, at 56.

The Shadow Board’s policy preferences remain stable. It is 60% confident that keeping interest rates on hold is the appropriate policy, one percentage point up from July. It continues to attach a probability of 2% that a rate cut is appropriate and a 38% probability (39% in July) that a rate rise, to 1.75% or higher, is appropriate.

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 1.50% equals 25%, two percentage points higher than in July. The estimated need for an interest rate decrease is 7% (6% in July), while the probability attached to a required increase equals 68% (71% in July). A year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 16% (14% in July), while the confidence in a required cash rate decrease rose two percentage points from 7% to 9%, and in a required cash rate increase fell from 79% to 76%.

Updated: 20 April 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin