Outcome

The RBA is now entering a difficult period where the economic data is strongly indicating that growth momentum has fallen sharply but inflationary pressures remain elevated. As a result the Board’s decision to hike again or hold could go either way.

With December’s retail sales data suggesting that household spending may have peaked (retail volumes likely declined in the December quarter, with spending on services set to broadly offset this), the real estate sector going through a correction, and government spending momentum easing the headwinds to growth are significant. All of these trends could manifest into a hard landing for the economy, and the potential for a correction in the cash rate.

Set against these trends are the broad-based nature of inflation, with many businesses still looking at price resets that are not consistent with inflation falling back to c.2.5% in the near term. Furthermore nominal wages growth, which is currently running at close to 5% on an annualised basis, is also not consistent with the RBA’s target band. This suggests that further action is needed to cool the economy and the labour market, to bring cost and price inflation back down.

Overall, the peak of the current hiking cycle looks to be in sight. Beyond this an extended period of the cash rate being on hold is likely to be appropriate, to unwind current inflationary pressures in an environment where growth momentum remains soft but positive.

Previous periods when unemployment has fallen below 4%, namely 2008 and 1974, have seen inflation accelerate uncontrollably.

To avoid a repeat, the growth in GDP need to fall below 2% and the unemployment rate needs to increase to a sustainable level.

Current projections, assuming mild increases in the cash rate, do not bring inflation and unemployment quickly to their targets. So we need to tighten faster than assumed in those projections.

Updated: 14 May 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Monetary Tightening Needs to Continue to Bring Rising Inflation Under Control

The annual headline inflation rate in Australia climbed to 7.8% in Q4 of 2022, the highest it has been since Q1 of 1990, driven mainly by increased prices for food, automotive fuel, and new dwelling construction. The RBA Trimmed Mean CPI increased 6.9% year-on-year, the highest print since the series began in 2003 and well above the RBA’s target band of 2-3%. While there are signs that past interest rate increases are slowing the economic activity, the Australian economy, in particular the labour market, remains quite strong. The global economy is also proving to be more resilient than expected. The RBA Shadow Board is convinced further monetary tightening is appropriate. In particular, it is 78% confident that the overnight rate should be raised to above the current setting of 3.10%, with a mode recommendation of a 25 bps increase, to 3.35%, whilst attaching a 20% probability that keeping the overnight rate on hold this round is the appropriate policy.

The official Australian seasonally adjusted unemployment rate for December 2022, according to the Australian Bureau of Statistics, remained steady at 3.5%, due to a small decrease in employment of 14,640 and a drop of the labour participation rate from 66.8% to 66.6%. Youth unemployment stood at 7.67%, a smidgen lower than in November, while the underemployment rate remained steady at 6.0%. Total monthly hours worked in all jobs decreased by 1.9 million between November and December. Job vacancies and job advertisements fell slightly but are still historically very high. The Australian labour market remains tight, even though there are early signs it may be cooling a little. The RBA will closely watch the release of the wages growth figure for Q4 of 2022 (to be released later this month), to glean just how much the labour market tightness is translating into wage pressure and, ultimately, prices. Given a headline inflation rate of above 7%, real wages have contracted significantly and, with a wages growth forecast of below 4%, are expected to continue to do so.

The Australian dollar extended its prolonged rally after putting in a low of 63 US¢ in mid-October. It has comfortably remained above 70 US¢ for the past couple of weeks. Yields on Australian 10-year government bonds edged up to above 3.4%. At longer maturities, the yield curve retains its normal convexity; however, at short-term maturities, the yield curve has retained its inversion, which is often interpreted as portending an economic slowdown, or even a recession. At medium-term maturities, the yield curve remains flat. The spread between 10-year versus 2-year bonds, compressed further since the last round, to 31 bps. Australian shares have participated in the new year rally, most recently approaching the major highs made in April 2022: the S&P/ASX 200 stock index started the month below 6,900 and is now, at time of writing, trading above 7,500.

Consumer confidence rebounded a little, as reflected in the increase of the Melbourne Institute and Westpac Bank Consumer Sentiment Index, from 80.3 in December to 84.3 in January. Month-on-month retail sales disappointed, declining by 3.9%, much more than the market forecast of 0.3%. The household saving rate declined further, to 6.9% in Q3 of 2022, the lowest in over three years. Business confidence, as measured by the NAB’s index of business confidence, took a hit in November, but recovered a little in December, from -4 to -1. The manufacturing and services PMIs also dropped slightly, whereas the Judo Bank Australia Services PMI ticked up in January (from 47.3 in December to 48.6). The capacity utilisation rate continued its decline, to 83.7%, suggesting that bottlenecks in production are easing. The Westpac-Melbourne Institute Leading Economic Index, a leading indicator of economic activity, fell for the seventh consecutive month, albeit only marginally, by 0.1%. While there is great uncertainty around this number, the sustained fall of the index does point to an impending slowdown of economic activity.

In light of China’s reopening and signs of surprising resilience in many parts of the globe, the International Monetary Fund (IMF) revised its forecasts for global growth upward. It is now expecting that global growth will slow from 3.4% in 2022 to 2.9% in 2023 and then rebound to 3.1% in 2024. The slowdown will be more pronounced for advanced economies but many are nevertheless expected to narrowly avoid recession, including the US. The outlook for developing economies is rosier, especially for India and China, which together are expected to account for half of economic growth in 2023. Headline inflation appears to have peaked in most countries, as supply chains are improving and energy prices are cooling, but the IMF did revise upwards its prediction for global core CPI inflation. It therefore concludes that central banks need to maintain their resolve to bring inflation down to their respective target levels. The Washington based organization includes stubborn inflation among possible downside risks for global growth, along with a stalling of the Chinese economy, an escalation of the war in Ukraine and disruptions in financial markets. On the upside they point to relatively strong household balance sheets and labour markets. Overall, compared to the IMF’s October forecast, the outlook is distinctly brighter.

For the current (February) round, the Shadow Board is convinced that the tightening cycle needs to continue. It is attaching a 78% probability that another rate rise, above the current level of 3.1%, is the appropriate policy stance, with a mode recommendation of a 25 bps increase. The Board attaches a 21% probability that keeping the overnight rate on hold is the appropriate policy and a mere 2% probability that a decrease is appropriate.

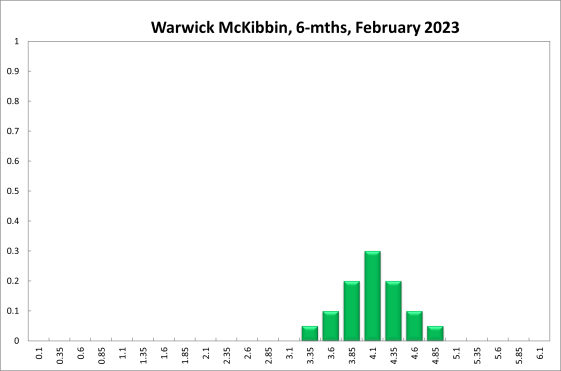

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at the current setting of 3.1% equals 10%; the probability attached to the appropriateness of an interest rate decrease equals 7%, while the probability attached to a required increase equals 83%. The mode recommendation at this horizon is 3.85%, 75 bps above the current level.

One year out, the Shadow Board members’ confidence that the appropriate cash rate is 3.1% equals 11%. The confidence in a required cash rate decrease, to below 3.1%, is 11% and in a required cash rate increase, to above 3.1%, equals 78%. Three years out, the Shadow Board attaches a 9% probability that the overnight rate should equal 3.1%, a 33% probability that a lower overnight rate is optimal and a 57% probability that a rate higher than 3.1% is optimal.

The range of the probability distributions shifted up and widened slightly. For the current recommendation the distribution extends from 2.85% to 4.10% (compared to a range of 2.50% to 3.60% in the previous round). For the 6-month horizon it extends from 2.60% to 5.60% (compared to a range of 1.75% to 5.25% in the previous round). The range for the 12-month horizon changed from 1.50%-6.00% to 0.10%-5.35%. The range for the 3-year horizon, which was identical to the 12-month horizon in the last round, changed to 0.1%-5.85%.