Outcome

Early this May, the U.S. Federal Reserve increased the target policy rate by half a percentage point. This is the largest increase in over 22 years. In a recent interview, Fed Governor Chris Waller supported a further and continuous tightening of monetary policy “by another 50 basis points for several meetings” until inflation comes down to the 2 percent target.

The Australian economy is doing well both in terms of GDP as well as unemployment (3.9 per cent). In Australia, the CPI inflation is lower than in the U.S.A. but still above the 2-3 per cent target. Year-ended C.P.I. trimmed inflation is at 3.7 per cent. Given this, I believe it would be appropriate to further increase the policy cash rate in the June meeting.

The economic data continue to confirm that demand in the economy is running hot relative to supply. Furthermore, developments globally over the last month have confirmed that this year’s shocks to commodity markets and supply chains have become at least semi-permanent (and in some cases have worsened) – further policy tightening is needed to realign supply side capacity with demand.

Against a more inflationary global backdrop, there is further evidence of broadening inflation pressures domestically, with the domestic final demand price deflator rising 1.4% q/q in March quarter. It is also looking increasingly likely that this year’s award wage setting process and collective bargaining agreements will result in significant pay rises for those covered by these agreements, while momentum in private sector wage setting looks likely to deliver wage increases of c.3.5% on average.

To ensure that inflation expectations remain anchored and mitigate the need for a much sharper slowdown in growth momentum in the future, the RBA Board should raise the cash rate again at its June meeting, and follow this with further rate rises through 2022 and H1 2023.

Now that the RBA is in a raising cycle, I don’t think they should immediately reverse themselves by moving back to the ZLB unless there is a quick deterioration in economic conditions globally (possible) or domestically (unlikely in the near term). However, given that wage growth came in weaker than anticipated by the RBA in making their decision to start raising the cash rate last month, they could pause the raising cycle or just raise 15bps to bring the cash rate to 50bps, a more conventional level than, say, 35bps or 60bps. Raising to 75bps is possibly justified by the very high year-ended GDP deflator inflation for 2022Q1. But if inflationary pressures do ease, the RBA risks raising too quickly and needing to correct with long and variable lags. Generally, it is more important for fiscal policy than monetary policy to return quickly to neutral at this point, at least as long as long-term inflation expectations measures such as the 10-year breakeven rate remain anchored within the 2-3% target range.

Updated: 14 May 2024/Responsible Officer: Crawford Engagement/Page Contact: CAMA admin

Shadow Board Advocates Another Rate Rise

The annual (headline) CPI inflation rate in Australia of 5.1% (Q1 of 2022) remains a significant concern for the RBA, as it lies well outside the official target band of 2-3%. The unemployment and spending data support the view that the Australian economy is re-equilibrating after the pandemic, but growing challenges for the global economy and more cautious projections about the future by consumers and businesses, may slow the recovery considerably. The RBA Shadow Board’s verdict is now, on balance, in favour of a further rate rise. It is 65% confident that the rate should be raised to above the current setting of 0.35%, and it only attaches a 10% probability that keeping the overnight rate on hold this round is the appropriate policy.

The official ABS (seasonally adjusted) unemployment rate fell below 4% in April, as predicted, to 3.9%; youth unemployment edged up, from 8.3% in March to 8.8% in April. Total employment increased by a mere 4,000 but nearly 90,000 part-time jobs were replaced by full-time positions. The labour force participation rate, which tends to move very little in the short term, ticked down to 66.3%. The underemployment rate dropped for another month, from 6.3% to 6.1%, while monthly hours worked increased by a respectable 1.3%. The most recent release on wages data revealed that Australia’s seasonally adjusted wage price index (WPI) rose by 2.4% year-on-year in Q1 of 2022, just shy of the market forecast. While this is the highest reading in more than three years, it falls well short of the current inflation rate, implying that real wages are falling. This should reduce overall inflationary pressures. At the same time, a low unemployment rate is expected to add further pressure for wage increases in the second half of the year.

The Aussie dollar again dipped below 70 US¢ earlier in May but has since rebounded to around 72 US¢. In light of strengthening expectations of further rate increases, yields on Australian 10-year government bonds continued their climb, from a recent low of approximately 1.65% five months ago to 3.5% on 3 June. Yield curves retain their normal convexity. At longer-term maturities, interest rate spreads (10-year versus 2-year) have narrowed, indicative of a flattening of the yield curve. Australian stock prices fell a bit. After a downward excursion to below 7,000, the S&P/ASX 200 stock index is now trading above 7,200.

Farther afield, the major challenges for the global economy remain in place: commodity shortages, especially in grains and other food items, high fuel prices, inflation, disrupted global supply chains, the Ukraine war. According to the UN’s latest World Economic Situation and Prospects (WESP) report, the global economy is expected to grow by only 3.1% in 2022, instead of 4.0% projected in January. Global inflation is predicted to reach 6.7%, twice the average of 2.9% in the past decade. The more pessimistic projections, echoed by other international institutions, further cite the Covid-19 related slowdown in China and the increasingly contractionary monetary policy stance adopted by the world’s main central banks. US Federal Reserve Chairman Jerome Powell unambiguously stated that the Fed would continue to raise interest rates until there was “clear and convincing” evidence inflation was on track to return to the official 2 percent target. There is growing concern, especially in the financial markets, that this may not be achieved through a soft landing but through a policy-induced recession. The European Central Bank, too, is having to navigate the difficulties of higher inflation, largely attributable to an increase in higher energy prices following Russia’s invasion of Ukraine, and flagging growth in the Eurozone.

Consumer confidence in Australia took another hit, for the sixth consecutive month, as evidenced by the Melbourne Institute and Westpac Bank Consumer Sentiment Index dropping from 95.8 in April to 90.4 in May, the largest percentage decline since June 2015. Private sector credit growth on the other hand rebounded strongly, with a reading of 0.8% month-on-month, or 8.6% year-on-year, considerably higher than the forecast of around 5%. The personal savings rate has fallen a couple of percentage points, to below 12%. Business confidence also took a hit; NAB’s index of business confidence deteriorated from 16 to 10 in April, while the manufacturing PMI likewise dropped from 58.5 to 52.4 in May. The capacity utilization rate improved slightly to just under 84%. The Westpac-Melbourne Institute Leading Economic Index entered negative territory again, declining by 0.2% year-on-year, based on its most recent reading in April. Its six-month annualized growth rate halved from 1.69% to 0.88% in April. The S&P Global Australia Composite PMI also retreated in May, from 55.9 to 52.9. All these number suggest that while private sector spending currently looks solid, there is growing uncertainty about the future and this may keep aggregate demand in check.

After the official cash rate target stood at the historically low level of 0.1% for one-and-a-half years, the Reserve Bank of Australia increased the target rate by 25 basis points, to 0.35%, in May. For the current (June) round, the Shadow Board is 65% confident that the overnight interest rate should be raised further, to above 35%. It attaches a 10% probability that keeping the overnight rate on hold is the appropriate policy and a 25% probability that a decrease is appropriate.

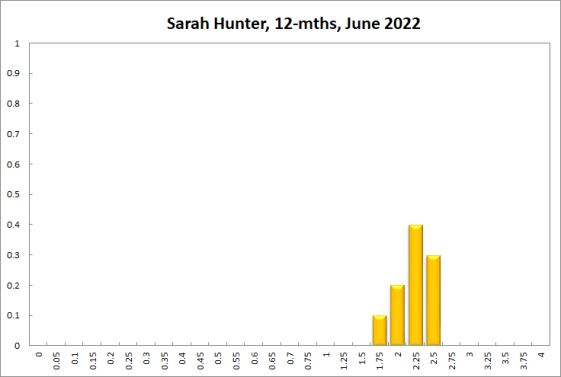

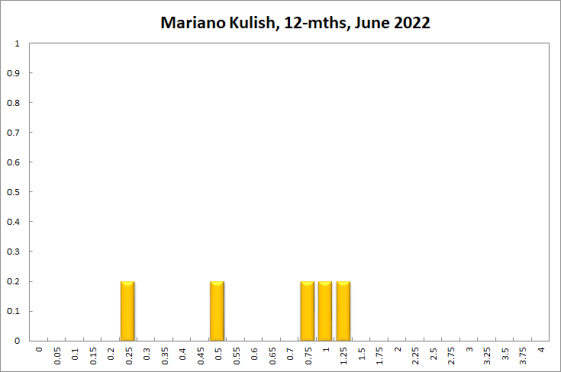

The probabilities at longer horizons are as follows: 6 months out, the confidence that the cash rate should remain at the current setting of 0.35% equals 3%; the probability attached to the appropriateness of an interest rate decrease equals 19%, while the probability attached to a required increase equals 76%. One year out, the conviction that a rate increase is required strengthens. The Shadow Board members’ confidence that the cash rate should be held steady is a mere 1%. The confidence in a required cash rate decrease, to below 0.35%, is 8% and in a required cash rate increase, to above 35%, equals 91%. Three years out, the Shadow Board attaches a 0% probability that the overnight rate should equal 0.35%, a 6% probability that a lower overnight rate is optimal and a 94% probability that a rate higher than 0.35% is optimal.

The range of the probability distributions for the current and 6-month recommendations, widened, reflecting a reassessment by at least some members of the tail risks: for the current setting, it extends from 0.1% to 1.5% and for the 6-month horizon it extends from 0.1% to 2% (compared to a range of 0.1 to 1.75% in the previous round). The range for the 12-month horizon has narrowed slightly to 0.35% to 2.5% and for the 3-year horizon it remains unchanged at 0.1% to 4.25%.